For the sake of liquidity (tax-favored accounts tend to be subject to tax penalties), you will want at least one tax-exposed account. Examples include money for a major business (buy out the boss), or personal outlay (second home), or a Tier 3 cash reserve. But let’s say that you need an equities component to enhance the likelihood of a high return. Phantom income will bite you, and so would using an annuity.

Life insurance has an up-front load that renders the use of these policies inappropriate for medium-term investing (even the low-surrender charge versions have this load). And equities fund managers are constantly turning over the portfolio, passing tax liability through to you. You are building this fund, so it’s not big enough for money manager minimums. Index funds, contrary to popular belief, have fairly high turnover and are not typically tax-efficient. What to do? Discuss a blue-chip dividend-focused fund with your broker; most have low turnover and dividends can be taxed below ordinary income tax rates. Consider individual stocks, too, picked for long-term growth potential, and recommended by analysts as long-term hold candidates. There are tax-controlled ETFs with very minimal turnover and low management fees; also consider Unit Investment Trusts (UITs) that have no management fees and no turnover. Many of these funds have names with “long-term equity” or “tax saver” in them, but your brokerage should be able to find the best candidates and then modify the risk profile, as you approach your intended liquidation date, by buying bonds with new money additions instead of selling off these equity funds as a way to lower volatility as time goes onward.

Roth conversion

This is exposing IRA or QRP money to taxation in return for growth never being subject to income tax. Let’s insert a caution I have found that few professionals discuss. It’s one thing to build up a Roth account from scratch if you believe that your income tax rate in retirement will be high (above 15% or so). It’s an entirely different matter to pay tax now to make a conversion. The early withdrawal penalty waiver if you’re younger than 59.5 is scant compensation. Everyone wants tax-free income, but the risk incurred to get it can be folly.

Let’s examine the crucial factors that must be modeled and provided to you. Suppose you are smart and convert in phases, so as to prevent the distribution from being pushed into high tax brackets. Great. But now you have sustained a definite loss from income taxation. What if you get scant gain in the coming years before retirement or before most years of retirement pass? What if it’s worse than that and you take a loss? Sure, you’d presumably have had the same strategy with the IRA or QRP, and so the same investment results, but you would have far more that could earn you more eventually! So before you convert, ponder whether you have many years to recover from some investment loss or just disappointing gains; the tax loss could have been avoided. In fact, you must have three things going for you for a conversion to make sense: you really do have reason to expect a substantial tax bracket during retirement, you really do get a significant gain (higher than EIAs or conservative investments can get you) to harvest those big numbers tax-free, and you have reason to believe you will be alive to make the probabilities of a good return work for you (many years to recover from possible losses). If any of these three factors are not in place for you, then do not convert.

When to convert?

Conversion works best when two conditions happen simultaneously: You have a low-tax-bracket year and you had a loss in the market (and have good reason to believe the market is near the bottom and soon to rebound). That means you need a crystal ball, but one must estimate the odds given the available indicators existing at the time. It also would be optimal if you paid the tax due from your cash reserve (rebuilding it ASAP, if you’re prudent); cash reserves would not have lost much in a downturn.

Good timing would be after a layoff that put you in a low bracket, for example, or when you started a business that had great potential once you worked past the early losses.

But conversion can help greatly if at least reasonably well timed and if a decent return is captured for many years.

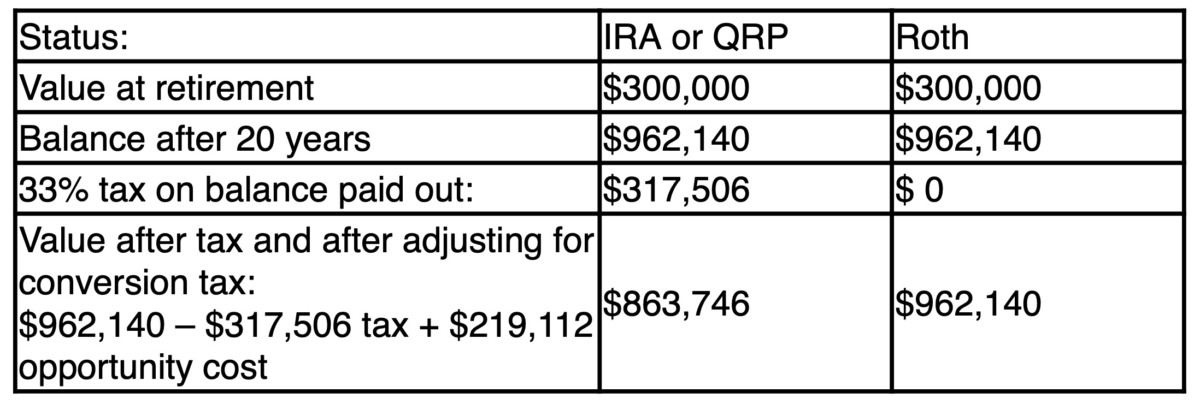

The following table shows the tempting results, though the calculations are necessarily complex. The table below compares having a Roth account to keeping one’s IRA unconverted.

But it makes two less-than-obvious adjustments required in order to focus your attention on a single measure of the tax burden and also on the two account values after a “fairness adjustment” that increases the IRA balance strictly for fair comparison purposes. That is, keeping the IRA would look unrealistically advantageous if I did not make an adjustment for the tax on Roth conversion, and how that tax cost would compound had it not been sent to the IRS.

One normally pays for a Roth conversion with out-of-pocket funds, and this is assumed, mainly to show two identical starting values growing and then accessed for income in one lump amount. I apologize for these two somewhat complex assumptions, but they are necessary for a fair comparison. Therefore, this table does not show income drawn until after twenty years of tax deferral. This method lets you see the growth, and then the tax upon full exposure to income taxation. The owner is assumed to be 65 years old, about to retire with a $300,000 balance that can be converted or kept as an IRA. He or she is assumed to take Required Minimum Distributions (RMDs) from some other IRA.

This assumption allows me to isolate the growth in the account and then show tax upon liquidation for comparison’s sake. So, neither the Roth nor the IRA distribute income at age 70.5; rather, they defer twenty years and then both pay out their balances. A 6% return for twenty years is assumed; also a high 33% tax bracket. Since the optimal way to pay conversion taxes is out of pocket, preserving the principal intact and allowing both accounts to grow from the same account value, I had to equilibrate the IRA to the Roth in some way. The fairest way to equilibrate is artificial. But my method is the fairest way to create a value comparison at the twenty-year mark and thereby fairly compare each: I added $219,112 to the remaining IRA balance (i.e., the $100,000 conversion tax at 6% interest, less the tax on that interest, meaning 4% net interest, compounded for twenty years). This adjustment may be viewed as the total “opportunity cost” over twenty years of paying the conversion tax. This add-in is at the twenty-year mark:

The conclusion is that the decision to convert the Roth “created” $98,394 in extra value on an “opportunity cost”-adjusted basis ($962,140–$863,746). But note that this was all contingent on a high tax bracket and a consistent 6% return as well as twenty years to make this difference come to fruition. That’s not a really reliable set of assumptions, just to obtain a ten-percentage-point advantage. Don’t compare this $97,549 amount to the $100,000 tax paid up front and conclude that it’s a wash, because the adjustment already takes this into account; the advantage is real. My caution—even though I acknowledge the advantage of conversion under these assumptions—is that you exchange a certain loss for an uncertain gain and then proceed to risk your savings in the usual manner in pursuit of some needed return.

There are models every broker uses to analyze the tax liability of re-designating IRA or qualified plan assets to Roth (taxed money in), as well as the strategy of doing this over years in order to avoid pushing you into a higher tax bracket. The 10% penalty is waived if you make this conversion, but you still need to let it grow until you are past the early withdrawal penalty. Alternatively, you can use IRC Section 72(t), discussed later. Here is my “strategic” heartburn with conversions as compared to funding a Roth IRA with new savings: The tax bite is a very large “loss” up front, and as we will see dramatically in the retirement planning chapter, early losses have a far greater effect than later ones (the sequence of returns and losses, in other words). You have a 100% chance of this tax loss, yet you do not have a 100% chance of fully capturing the benefit you seek (big tax savings in retirement because the withdrawals escape income tax). Possible failure to meet this objective comes from three types of risk:

• Tax rates may become low in the future.

• Your projected income tax bracket could be wrong (e.g., you might be less successful as you expect, or a disability could prevent you from building a large nest egg and large income from it).

• You could experience investment losses that limit the size of the Roth account later (that might have happened in the IRA or qualified plan, but you only have two years to change your mind and convert back to the original tax designation).

Roth conversion spreadsheets do not model these possibilities that could thwart what you seek to accomplish with conversion to a Roth. If you want to pursue tax-free income with great growth potential, I strongly advise building the Roth or the similar life insurance strategy from newly saved money (other assets can also go into a life policy, such as liquidating assets that have low capital gains, or offsetting gains with other losses). The maximum Roth contribution will inflate, but currently the limit on any IRA contribution, Roth or IRA, is $5,500 (with an extra $1,000 if you’re 50 and older).

This excerpt is taken from “The Secrets of Successful Financial Planning: Inside Tips From an Expert,” by Dan Gallagher. To read other articles of this book, click here. To buy this book, click here.