A Shameful Secret

Some carriers make software available to calculate the correct estimated equivalency of the policy face value to the SBP. But most actually forbid their reps (even in written policy) from so much as suggesting this, especially for government and military pre-retirees. Why would they, if it creates an opportunity to sell policies? Follow me with this linkage along two routes.

First, the secret is that pensions (especially military and government pensions) actually take pains to discourage you from even learning about SBP replacement. That’s because they fear “adverse selection,” meaning it is in their financial best interest to keep “selling” SBP because if people in good health opt out of the SBP, then the plans have to raise more money. They are left with a poor-health population whose SBP is expensive for the plan, yet paid for by the retiree’s pension reduction being over a brief period of years because of that poor health.If SBP replacement occurred often, the pension plan would lose the pension reductions that healthy retirees sacrifice, and it would have to pay SBP sooner for unhealthy retirees whose SBP would be paid over many years, and that plan would lose out on the pension reductions from healthy retirees whose SBP would, if those healthy ones kept the SBP, be paid only briefly to their widows.

In the early 1990s, using instances of financial planners inappropriately promoting investment and insurance sales as “government specialists” on military bases and other government facilities, Congress forbade this marketing positioning.

Second, at the same time, both private and public pension plans backed lawsuits and regulatory complaints against insurers and brokerages for faulty or incomplete SBP replacement advice. The result is that most carriers became so intimidated that instead of carefully training advisors and providing proper software, they simply forbade reps from discussing SBP replacement.

If you assume typical mortality tables (for which the healthy are only a part, by the way) and ignore the two subjective issues of the potential widow dying first and also ignore the fact that that insurance can leave a legacy whereas an SBP never does, and you assume average mortality charges in a policy (remember, use only policies recommended above), then “smart” financial planners will decry using SBP replacement. But individuals must make smart decisions for their household and not be deterred from decisions that are expensive for the Pension Plan. So I submit that for many people, SBP replacement is an excellent and advantageous option, and further that dismissing it broadly or concealing it from pre-retirees is a moral turpitude.

Required Minimum Distributions (RMD)

Qualified plan money and IRAs are subject to IRS regulation at the distribution level as well. One cannot defer taxation and pass the account to a child without exposing the money to income taxation.

If, by December 31 of the year in which you reach 70.5, you do not take income at the prescribed withdrawal rate, any income you should have taken but did not is penalized. Specifically, your government confiscates half of that amount. (See? You got me started again! Okay, breathe ... breathe. Fine, let’s start again.) There are worksheets for this at IRS.gov, but I recommend the online calculator at https://72t.net/MinimumDistribution/Calculators.

There, you will notice three calculation methods, each using the prior December 31 valuation of—note this—all IRA and qualified plans totaled. You can take the money from any combination of your plans, but you must take the minimum. Annuity payouts are higher than this minimum; some annuities allow for splitting the contract between immediate lifelong income (i.e., annuitization or guaranteed withdrawals) and deferring some of the original balance. Start by the last day of the year in which you reach age 70.5, but you can delay this a bit if you remain employed full time at that age.

Stretching Your Tax-Deferring to Your Personal Max

Use up currently taxable accounts first, your IRA (that must be accessed at age 70.5 anyway) next, and other tax-deferred accounts last.

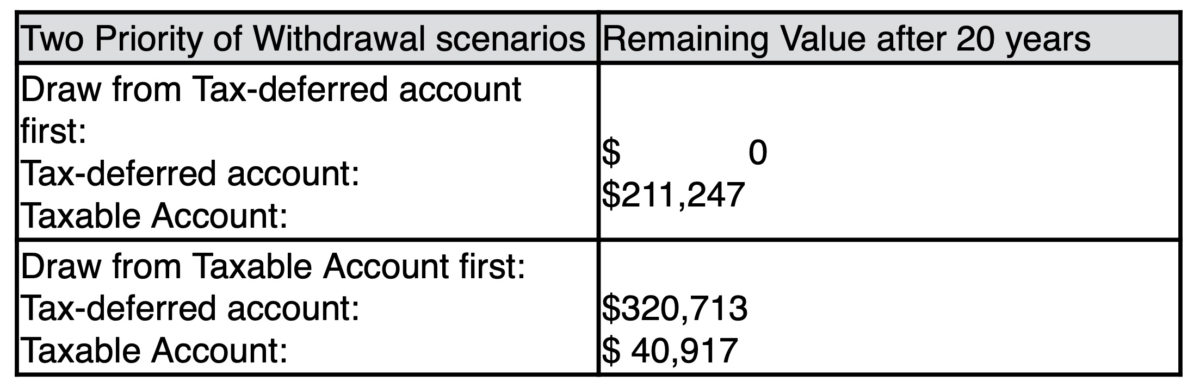

If you are in a high tax bracket and able to delay taking income, here is your best strategy: Keep tax deferral going as long as possible; you’ll end up with a greater asset base. This is because money that would have gone to pay tax could be earning you more tax-deferred, and you will get to keep most of the extra earnings. This table shows money remaining if you spend taxable money first. It assumes you start retirement with $200,000, half in a taxable account and half tax-deferred, you are in a total tax bracket of 33%, you earn 6% per year in each account, and you withdraw $6,000/year:

Using up taxable accounts first for income leaves $361,630 after twenty years; the reverse strategy leaves $211,247. So stretch out the IRA or QRP withdrawals to continue at least partial tax deferral after death. This is addressed in the estate planning chapter.

Reverse Mortgages

Reverse mortgages (RVs) can be conceptualized as the lender slowly buying the owner out of their home over the entire lifespans of those retirees. This only stops upon both relocating from that residence.

The main form of an RV makes payments to the owner(s) lifelong and the house is collateral for that loan. These payments build up slowly; because of this, the interest expense on these payments is slight—the opposite of paying down an old-fashioned lump mortgage loan (for a lump loan, most of the payment you make is interest expense and so the principal owed reduces excruciatingly slowly). Unfortunately, the transactions cost up front is significant and this amount can be paid in cash or else set to be principal on the loan from the start. But even that underwriting and transaction cost is small compared to the large huge amount of interest that accrues from an initially large-amount mortgage. Eventually, you will leave the house (horizontally, assisted, or walking; to a retirement home or any other residence).

Upon that trigger, the house is sold (just a bit ahead of time by the owner or else just after exit by the lender). Lenders must act as fiduciaries to get a good price if they control the sale, but there is a lot of leeway there, so get a good Realtor to get the likely highest price. When sold, the loan is repaid. If the loan repayment cannot be covered (the house lost value or appreciation failed to keep pace with lifelong payments to the owners), then the lender has taken that risk of loss. This is so even if the deficit sale occurs well prior to owners’ deaths. That’s right: There can be no “deficiency judgment” as there might be for a regular mortgage. That’s a huge safety net! If there is cash left over at closing, then the owners (or heirs) receive the excess. The fees are high, but at least the heirs are not forced to sell the house themselves.

This excerpt is taken from “The Secrets of Successful Financial Planning: Inside Tips From an Expert,” by Dan Gallagher. To read other articles of this book, click here. To buy this book, click here.

The Epoch Times Copyright © 2023 The views and opinions expressed are those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.