Strategy of Claim Lower Now, Higher Benefit Later

The higher-benefit spouse defers but takes a spousal benefit from the account of the lower-benefit spouse while that lower-benefit spouse starts reduced payment from his or her own account at age 62. This is two draws from one account. (How long will Congress make this available?) The higher benefit spouse, upon reaching age 70 (maximized benefit), switches from the spousal benefit to his or her own enlarged account.

Effective in 2016, one popular strategy—not to be confused with the foregoing—no longer works. Previously, for a couple, the retiree with the highest payout could use the “File and Suspend” application option.

In that strategy, a worker filed on time, then immediately suspended receipt of payments. The spouse with the lower payout filed as what was called “restricted.” This enabled the “spousal benefit” (a special benefit intended to be for spouses who did not ordinarily qualify).

While taking the small spousal benefit that continued to grow at 8% annually, the other two primary Social Security payments were deferred, inflating at about 8% annually because neither was taken at all yet. The benefit taken was the smaller spousal benefit, while both primary benefits increased due to age step-ups. This was essentially a small but meaningful pre-benefit that was never intended to be for someone who had his or her own normal qualification for full benefits. But now, the spousal benefit suspends when the worker’s does, and there is no growth in spousal benefit. There is an exception for widows, and this can be used for widows who plan to remarry. One can fill out the forms for this strategy, but now that would result in no inflation at all for deferring and one would discover this after it was too late to change the original selection!

Another, simpler strategy is to take both benefits as early as they can be taken (even at the discounted rate for taking them slightly early) on the rationale that one might die unexpectedly, so you might as well get both as long as you can (remember, surviving spouses only get the larger of the two benefits, not both).

There are so many rules and resulting permutations of options and results that, like income tax planning and filing, sophisticated software is now absolutely necessary for maximizing benefit strategy. Further, these rules change so much—they constitute a political football—that you should avoid making any decision about your options based upon this or any book or seminar. Such references and annotations get dangerously out of date.

Here’s the secret: Do not figure this out yourself and then pick a strategy for filing. Filing strategies require software for maximization; even then you will be betting on the timing and order of your and your spouse’s mortality. These programs are best run by financial planners or Social Security specialists.

The good news is that if you use a professional for this analysis and counsel, you transfer the risk of making an uniformed decision to the professional (i.e., if there was negligence or an omission, that professional’s Errors & Omissions policy will enable recovery for a valid claim). Some insurers provide this without charge if you are willing to consider their investments or annuities. “Free” does not relieve the professional from the duty of competent analysis and counsel.

Case Study

Indexed universal life insurance acting like a Roth account. Both provide tax-free income, but the policy also serves as a backup LTC policy.

Can’t put enough into a Roth? Need life insurance with LTC dual-purpose coverage and want the policy to also act like a Roth? As long as you recall that such a three-in-one policy can’t use a given dollar you take out for more than one purpose at a time, then consider this illustration of an actually issued policy and its details.

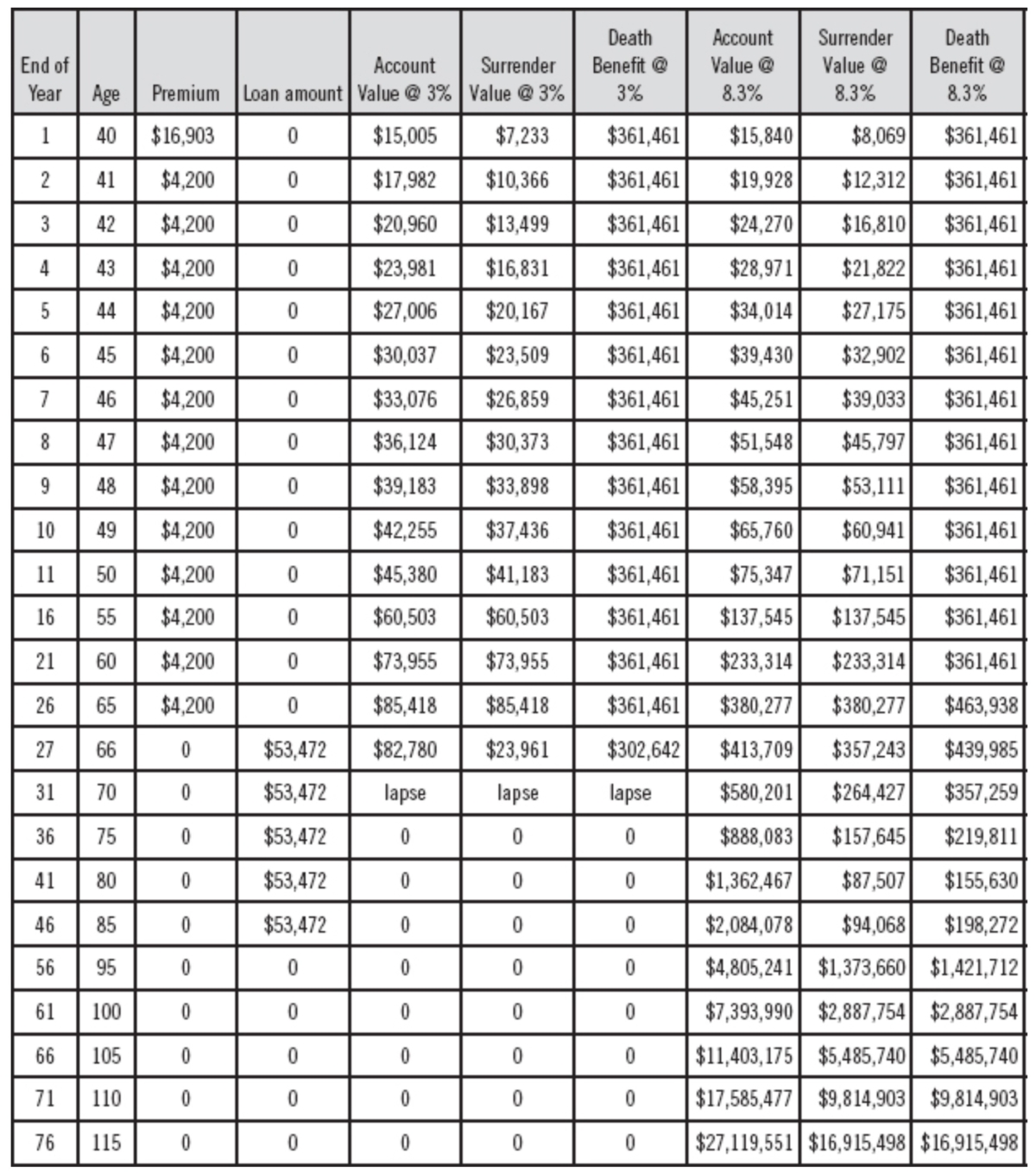

Summary of Indexed Universal Life policy from illustration ledger

Assumptions Tax-Free Income From Policy Loans

This $361,461 policy for a 39-year-old male shows $12,703 transferred from an old policy into this new one, and an annual premium pattern of $4,200 up to age 65, when the last premium is paid. At age 66 through age 85, loans are taken in the annual amount of $53,472. Neither principal nor interest is paid back. A “wash loan” practice (low or no interest because a minimum interest is credited to the loaned-out amount) is typical for carriers but is not shown even though it would reduce the interest expense.

This is because that 3% crediting against the loan interest is not guaranteed and the carrier did not choose to design its software to show this benefit. Interest expense therefore reduces the return on the policy. If the policy lapses, though, the total gain received becomes income taxable.

The policy is issued by an A+ carrier in operation for over a century. This is a very competitive policy but there are many superior to it, especially some available in no- or low-load versions.

The 3% column assumes that only this guaranteed minimum interest rate for money actually in the fixed account (the index options are not used) is credited but is also an unrealistically dismal assumption: These three columns assume that the maximum allowable mortality charge increases each year from year one and continues to increase geometrically. No life carrier has ever charged more than its “current” mortality charges, let alone the maximum allowable in the contract. So these three columns must be taken with a huge grain of salt. The last three columns assume that the current projection of mortality charge increases annually but only per the advertised pace of increase. If there is any over-optimistic assumption at all for the last three columns, it is with the rate of return assumed: 8.3% for the S&P 500 index. The software for this column does not adjust (nor does any carrier’s software) for the fact that the index rate assumed is “x-dividends” or the index, not counting dividends of the stocks.

There are growth stocks in this index, however, and the dividend rate is not huge. Let’s dive deeper into the rate of return assumptions to judge what is realistic for the policy and hence for using it as a tax-free income generator to supplement one’s Roth accounts.

Rate of Return Assumptions

There are no fees for the numerous indexed interest crediting options (Russell 2000, S&P 500, Dow 30, etc.). However, dividends are not included in the index performance, and there are monthly or annual caps imposed upon the highest index rise that can be considered in a month for purposes of calculating the annual interest rate credited.

Typically, this results in interest credits of around two-thirds of the published index performance but this can be higher in a slow-growth, less-volatile environment. For the 8.3% illustrated interest crediting to occur, the S&P 500 index would have to perform at 12.45% annually (this has occurred for extended periods, especially the last three decades).

The owner should react to loss years, when interest credited would be 0%. But there would be no loss, and refrain from loans or take less than shown in such stressed years; the same if the interest crediting trailed 8.3% as illustrated. This compares well, however, with non-guaranteed equities investing. Actual equities lack any guarantee against loss and, for losses occurring coincidentally with income draws, cause reverse dollar cost averaging (i.e., selling off low to harvest income and therefore having fewer shares to participate in upswings). The above illustrated policy was issued in May 2011 and performed considerably better (so far) than this illustration shows.

Premium Assumptions

This policy had a 1035 Exchange Amount of $12,703 from a previous policy. It has a level death benefit (Option A), so the death benefit can grow only slowly and only if the cash value begins to push it toward the IRS guideline definition of life insurance. The policy is guaranteed against market losses, though expenses continue. No fees for money management, only mortality expense. An incentive interest credit of 0.75% is credited to all interest options in all subsequent years after the ninth year, provided that the policy is held at least ten years. It passed the MEC test: the IRS Guideline Single Premium maximum was $63,634.78; the Guideline Annual Premium is $5,177.17.

Loans as Income and Assumptions for This Policy

The variable interest policy loan rate assumed is the higher of 4% or the Moody’s corporate bond yield average, up to a maximum of 10%. At the time of this illustration, that rate was 5.60%. This illustration does not show the 3% crediting of interest which is currently given and reduces the loan interest rate (it is given to remain competitive in the insurance market). The software does not show loans after age 85 for regulatory reasons, but the cash buildup for subsequent years shows that substantial loans may be possible lifelong; the owner will have to decide as the years progress whether to continue borrowing from cash value, what amount, and whether to remit all or part of the interest. This illustration shows no interest payment; it accumulates with the loan amount and is never repaid.

The underwriting class assumed was “Super Preferred Non-Tobacco”; the insured was a 39-year-old male with extensive driving in his work but no dangerous avocations (sky diving, motorcycle riding, etc.). If the insured is alive at age 120, this policy pays the death benefit as if he had died. Congress and the IRS have not passed on whether this policy would be considered a taxable endowment at ages after 100, but most tax experts agree that it would be considered a non-taxable death benefit if paid to the beneficiary and not the insured.

Special Provisions and Lapse Protection

The death benefit is available for long-term care needs, regardless of venue. This is a significant consumer value even though LTC claims would reduce the death benefit and the cash value proportionately so that the claim amount reduces the death benefit dollar for dollar. If the policy exhausts the death benefit, no premium is accepted after age 100, and no mortality charges are debited from the cash value (it is paid up but could lapse if loans stress the cash value). This policy has a no-lapse guarantee provided the minimum premium was paid for fifteen years and loans and withdrawals have not exceeded the “over-loan” protection thresholds (owner took no more than 89% of cash value via withdrawals and loans between ages 65 and 74; 93% afterward).

This excerpt is taken from “The Secrets of Successful Financial Planning: Inside Tips From an Expert,” by Dan Gallagher. To read other articles of this book, click here. To buy this book, click here.

The Epoch Times Copyright © 2023 The views and opinions expressed are those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.