Let’s look at the types of investments you might consider and how to build your portfolio for the long term.

Does low risk always mean lower returns? And, to increase returns, do you have to take more risk?

There actually is a way you can achieve higher returns without taking on more risk: by diversifying your investments!

The meaning of Diversify is to spread out your money over different types of investments.

Diversification allows an investor to lower risk without lowering the expected return. By combining different types of investments in a smart way, you spread out your investment over a wide variety of sectors and asset classes. The risk that any specific investment will fail is partially canceled by all other investments and overall risk is lowered.

Diversification differs from asset allocation in that when you diversify, you choose different sectors or types of investments within a particular asset class (say, for example, equities), as opposed to asset allocation which is spreading your investment over asset types with different risk (e.g., equities, bonds, and cash).

Having a diversified portfolio invested in a variety of stocks and a variety of sectors lowers the risk of losing much money when one particular investment declines. Too bad diversification cannot protect against risk that the entire market and economy may have a bad year (or more).

Building a Diversified Portfolio

The most basic method of diversification is to buy a mutual fund or index fund instead of the stock of just one company. Mutual funds could own shares in twenty, thirty, forty, or hundreds of companies giving you instant diversification. But, how can we diversify in an even better way to increase returns without increasing risk? Below is just one example of a properly diversified portfolio that you may consider. Before we start, though, let’s learn one more definition: “standard deviation.” It’s sort of confusing, but let’s just say that standard deviation is a measurement of risk that shows how much the returns of an investment stray from the average. The lower the number, the more consistent the returns and less risk; the higher the number the more variance and more risk.

Step One: Basic Portfolio

Start out with just two investments: 60% in equities (S&P 500 Index) and 40% in government bonds (Barclay’s Government Credit Index). The average annual return over the 40+ years shown was 8.8%; the standard deviation (risk) was 11.3%.

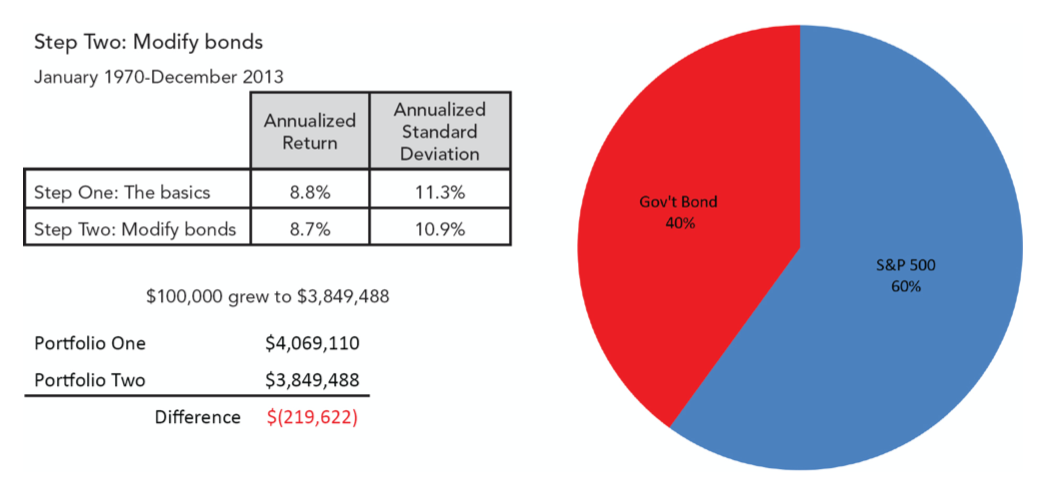

Step Two: Adjust Bonds

On the bond side, the experts who designed this portfolio use government bonds only: 50% intermediate-term, 30% short-term and 20% in inflation protected bonds (TIPS). This is slightly less risky than the basic portfolio above, but the return is almost the same. (I know, I know ... it isn’t terribly exciting yet, but don’t get too worked up, wait for the rest of the changes.)

Step Three: Add Real Estate Index

Real estate investment trusts (REITs) have historically returned around 10% per year. Conventional wisdom holds real estate and stocks go well together because they do not always move in the same direction—they tend to help cancel out the risk of the other asset class.

So ... after adding REITS to 20% of the stock part of this portfolio our returns are back to where we started, but the risk remains much lower. Again, still not earth shattering, but the best is yet to come.

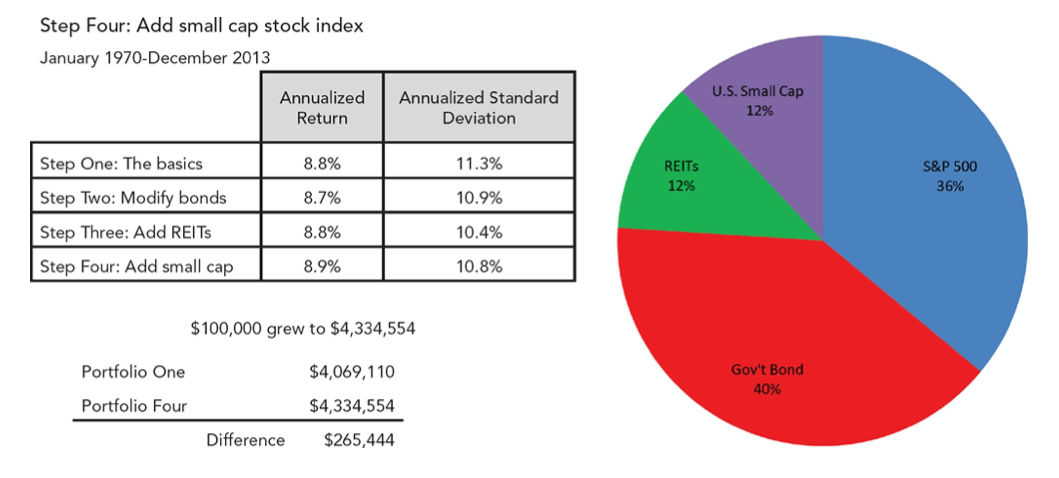

Step Four: Add Small Cap Stock Index

The portfolio shown in steps one and two consists mostly of the stocks of the five hundred largest U.S. companies—familiar names you might see in the news every day like ExxonMobil, General Electric, Johnson & Johnson, and PepsiCo. These companies did not start out huge though—at one point they were considered “small cap” companies. Because small companies can grow much faster than large ones, a basic diversification technique is to invest in stocks of small companies—that’s step four. Notice that the portfolio now has an annualized return of 8.9%, with a standard deviation of 10.8%—so far this strategy has added about $265,000 to the cumulative return with lower risk.

Step Five: Add Value Stock Indexes

Growth stocks are those with rising sales and profits that investors expect to do well because of growth potential—these already make up the bulk of the S&P 500 Index. Value stocks are those that are simply “on sale” because investors believe the company is having one kind of issue or another that it is solving. So, in this example, let’s add large company value and small company value indexes. The risk is still lower than the last step, but returns have gone way up!

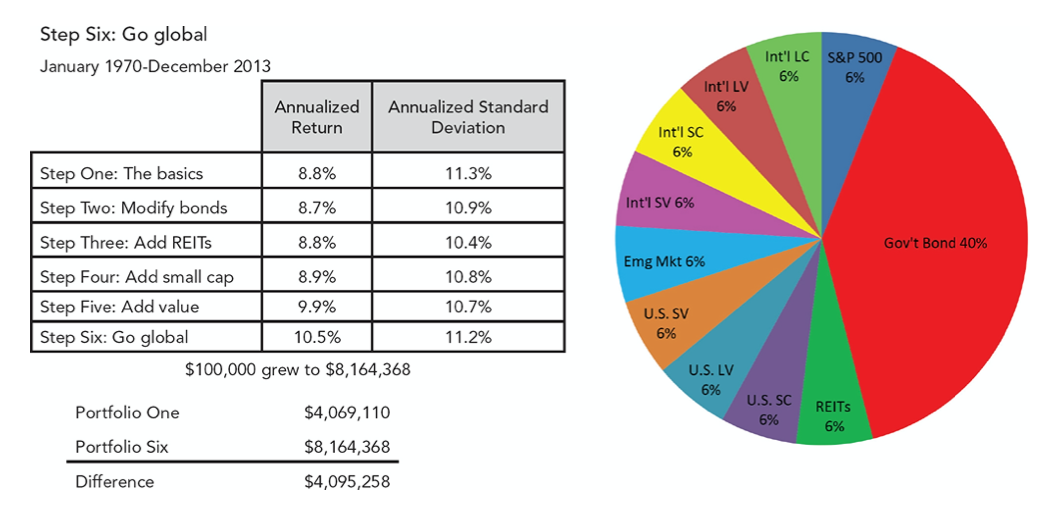

Step Six: Add International Indexes

In this last step, we are going to add additional indexes that include international stocks and emerging market stocks.

Now let’s put it all together ...

Our starting point was a return 8.8%, with a standard deviation of 11.3%. After six well thought out steps to diversify, the portfolio now has returns of 10.5% with a standard deviation of 11.2%.

Over the 44-year period shown, this portfolio would have grown to almost $8.2 million, twice as much as the traditional model shown in Step One—with less risk!

TAKEAWAY #12: Don’t put all your eggs in one basket. Stay diversified and follow a plan.

This excerpt is taken from “Young Adult’s Guide to Investing: A Practical Guide to Finance for Helping Young Peo Le Plan, Save, and Get Ahead” by Rob Pivnick. To read other articles of this book, click here. To buy this book, click here.

The Epoch Times Copyright © 2023 The views and opinions expressed are those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.