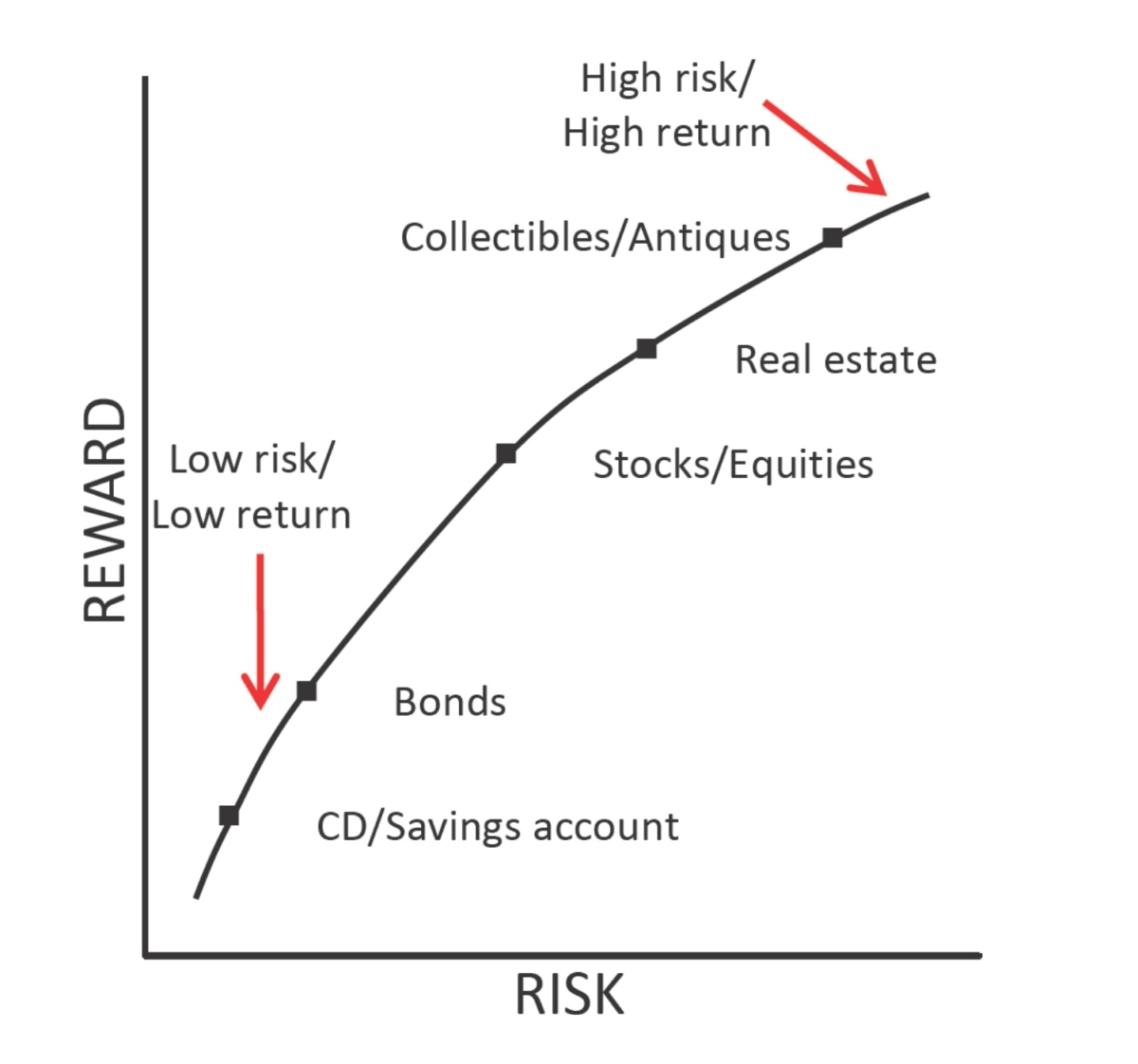

For example, bank savings accounts and certificates of deposits (CDs) offer very, very low returns close to 0.1%, but these savings vehicles are insured by our federal government if they are with one of the many banks you customarily see in your neighborhood. If you’ve seen the FDIC sticker below on the door of your bank, then your money is guaranteed by the United States government up to $250,000—meaning that if your particular bank ever went out of business, the government would give you your money.

Because stocks are riskier investments than savings in a FDIC member bank, if you invest in equities you should expect to earn a higher return. And this is the case—historical equity returns have averaged around 8.5% per year. And because investing in collectibles, such as jewels, antiques, coins, baseball cards, cars, or even wine, is much riskier, the potential returns for those investments must be even higher than stocks—to compensate for the higher risk. But the risk of losing your money in these investments is also much greater.

So, all this leads to the question of which investment is the “right” investment? You must consider all sorts of things when figuring out your risk tolerance. Your risk tolerance determines your willingness to benefit from an incredible investment at the possibility of losing your money. Take too little risk, and you won’t make as much money; take too much risk, and you could lose all your money. Several factors play into this decision:

- Would you risk losing most of your money in the short term, for the possibility of amazing returns in the long term?

- What is your investment horizon—that is, how soon do you need the money?

- Will you need access to your money quickly in the future?

- Can you change your plans? Do you have the ability to alter what you would use the money for if the investment goes poorly?

Asset Classes

You invest by balancing risk and reward depending on your own goals, risk tolerance, and investment horizon. The three main asset classes that are discussed in this book are stocks, bonds and cash. They have different levels of risk and return, so each will behave differently over time.

- Equities (sometimes called stocks) are ownership interests in a company or an asset. These have the potential to make or lose a lot of money, so both the risk and reward are high. Equities are investments you should hold for longer investment horizon. You can buy stock in companies like Nike, McDonald’s, AT&T, and Coca-Cola, plus many other smaller companies you have never heard of.

- Bonds (fixed income or debt instruments) are investments in which you loan money to a company. You are a lender (sometimes called a creditor) rather than an owner. Bonds are generally safer investments than equity which means that the potential returns should be lower. You can buy bonds (in other words, loan money to) in companies like Nike, McDonald’s, AT&T, and Coca-Cola. You can also actually lend money to the United States government (and lots of other countries) and its states and cities.

- Cash is simply the money you have in your checking or savings account (or stashed under your mattress!) that you can access immediately. The bank isn’t paying you much (if any) interest, so there is not much reward in keeping money in the bank, but it is the safest place to put it so you will always know it will be there.

The process of determining which mix of assets works for you today depends on the factors described above. And your risk tolerance today is not the same as it will be later in your life.

TAKEAWAY #6: Invest your money in safe investments if you do not have a lot of time to make your money back or if you need the cash quickly. Take more risk (for higher reward) for longer term savings goals.

Note:Your investment horizon is the amount of time you plan to hold onto your investment. The longer the horizon, the greater your ability to take more risk for higher reward. Long term investments allow you to recover from a bad year or two (or three or more) and benefit from potential higher returns. But if this is called being “liquid” your horizon is very short, stick to safe investments so you don’t risk losing any money before you need it.

This excerpt is taken from “Young Adult’s Guide to Investing: A Practical Guide to Finance for Helping Young Peo Le Plan, Save, and Get Ahead” by Rob Pivnick. To read other articles of this book, click here. To buy this book, click here.

The Epoch Times Copyright © 2023 The views and opinions expressed are those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.