You should be happy with average! It is better to be the market than to beat the market. It isn’t very often in life that you don’t want to be better than most ... But at the end of this chapter, you should want to be average when it comes to investing!

Adopt a Low-Cost Strategy—Minimize Expenses

The next three chapters may not be the most exciting part of the book, but they might just be the most important, so ... stay with me here.

Historically, market returns have averaged around 8.5% annually. So, as you saw from the compounding example in Chapter 1, this book will use 8.5% as a historical return average. That does not mean that in any given year returns won’t be better or worse, but over the long term, 8.5% is the approximate average.

Active

All investors have a choice of investment style when trying to achieve or beat that return average: active or passive. “Active investing” is a strategy in which an investment fund (or fund manager) attempts to outperform the market; the goal of active management is to beat the market or a particular benchmark. This strategy is for those that think they’re smarter than everyone else.

Passive/Indexes

“Passive management,” or “indexing,” is an investment approach in which the fund’s goal is to match the performance of the market (or match a particular sector, industry, or region within the market as a whole) as closely as possible, rather than try to beat it. Indexing does this by investing in the same securities in the same proportions as a market or sector. There are thousands of index funds available that track particular markets, sectors, industries or regions. Indexes represent benchmarks. Examples of indexes that you see on TV or online are:

- Dow Jones Industrial Average (representing 30 of the largest and most well-known companies in the United States)

- Standard & Poor’s (S&P) 500 (representing the 500 largest companies in the United States)

- Russell 2000 (representing the smallest companies in America)

- Nasdaq Composite (following companies listed on the Nasdaq, which is tilted towards technological companies)

- Wilshire 5000 (this is a total market index of the United States including all companies)

- EAFE (representing international markets “Europe Australasia and the Far East”)

This book aims to convince you that you should follow a passive investment strategy. The professionals advise investors that it is impossible to consistently beat the market without increasing risk. This idea is called the “efficient market hypothesis”—it states that the market itself is efficient and its performance is based on all the information about stocks that is available, so beating the market without taking on more risk is impossible.

Some studies have shown that there are some anomalies (things that are different from what is normal or expected) in the market that might allow for opportunities to beat the market over the short term—but over the long term the markets are efficient.

The word “consistently” above is emphasized because that is the key point. For any given period, or even for a day, someone can pick a stock that will beat the market ... but that person will have to do that day after day after day, year after year after year, to actually come out on top. One trade, one day, or one year even does not make someone a successful investor.

The chart below shows how passive index funds beat actively managed funds over a five-year period (this chart shows the five years ended 2017, but the results would be similar for nearly any five-year period). The percentages show how many actively managed funds beat the benchmark for their category. And, by the way, these results show all funds, even those that closed within the time period. (Their results may have been so bad that they went out of business—too bad for the people who thought they were actually smarter than the market and invested in those funds.)

Percentage of Actively Managed Funds That Beat Their Benchmark 5 Year Period Ended 2017

The exact stats vary depending on the year and type of asset category, but on average, anywhere from 70–90% of funds cannot beat the market. Only 10–30% of professionals beat the market year after year.

Do Not Try to Time the Market

A passive investment approach necessarily means that you should not try to time the market either. Many people might try to convince you that you can get into the market in good times ... and get out before the bad times ... then get back in before the next upswing. They will say that staying invested all the time should not be followed. The first decade of the 2000s had a lot of ups and downs, so it is not a surprise that some people do not favor a buy-and-hold strategy. But the question you have to ask yourself is “Do you think you’re smart enough to time the market’s movements?” The answer is ... no. If you are a long-term investor, you should not try to time the market.

In fact, most investors miss out on the good times precisely because they jump in and out of the market at the wrong times because they think they can time it. In the 20-year period ended in 2017, stock investors earned only 5% a year due to terrible market timing, nearly 4 percentage points less than a buy-and-hold strategy (and the market historical average).

But what if you could avoid the bad days? If you thought you could time the market and miss all the bad days, you’d be in great shape. But if you get out of the market at the wrong times, you also end up missing out on big rallies. If you missed out on just the 10 best days in the same 20-year period, your average annual return would have dropped to 3.5%. Miss the 30 best days and would have lost money.

It is virtually impossible for investors to successfully predict the market in order to capture good performance and avoid bad performance. Remember, the professionals whose job it is to do this and who get paid based on their success cannot do it 70–90% of the time! Why would you think you can do it? To be sure though, if you think you are smarter than the market and all those professionals, at least know what you are up against and make a reasoned decision to be an active investor. And don’t forget ... trading in and out costs commissions that lower your returns even more.

Minimize Costs/Expenses

Hopefully you are convinced that trying to beat the market is a fool’s game. So, let’s take it a step further and boost returns even more. We do this by eliminating or reducing fees that funds charge.

In life, people like to say that “you get what you pay for.” This does NOT apply to investing! Lower-cost funds actually outperform higher-cost funds. Every dollar paid for management fees or trading commissions is simply a dollar wasted.

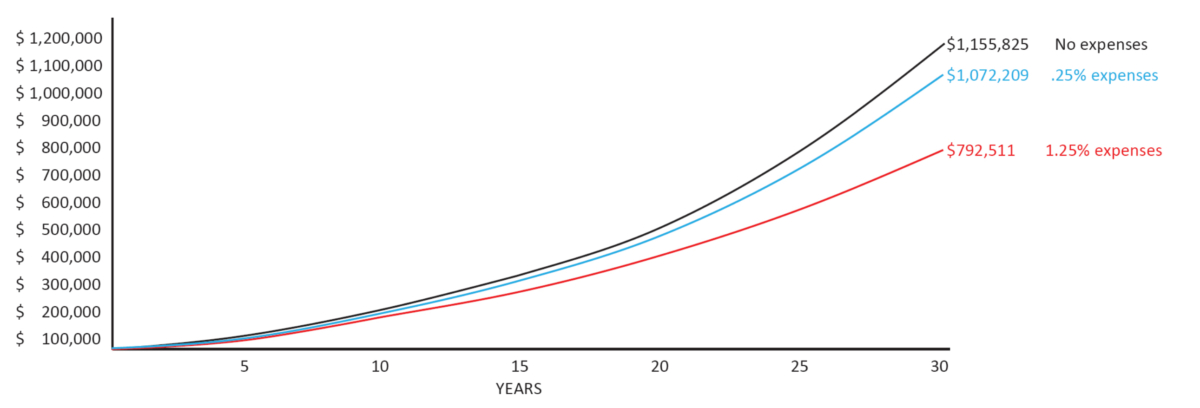

The chart below shows how fees and expenses affect investment returns. The chart shows thirty-years’ growth of $100,000 assuming an 8.5% annual return. The black line shows returns for paying no fees at all; the blue line shows low cost funds that only charge 0.25% expenses (which is about average for passive funds); and the red line shows a higher expense ratio of 1.25% (this is also about average expense costs for actively managed funds). You would have wasted almost $280,000 by investing in funds with higher costs as opposed to the low-cost index funds!! So, you can increase your return by beating the market, if you think you can. Or you can lower your costs. ... You decide which is easier. Do you have the skills to beat the market when far less than half of the professionals cannot do it over the long term (remember the blindfolded monkeys)?

Actively managed funds eventually revert to the mean but charge much higher fees. Index funds charge much lower fees than actively managed funds, and they too provide market average returns. So, if all investments ultimately produce the same returns, why would you pay much more for the actively managed funds? Indexing/passive investing will make you more money because it provides the same returns as active investing at a much, much lower cost.

Higher Fees Do Not Mean Better Performance

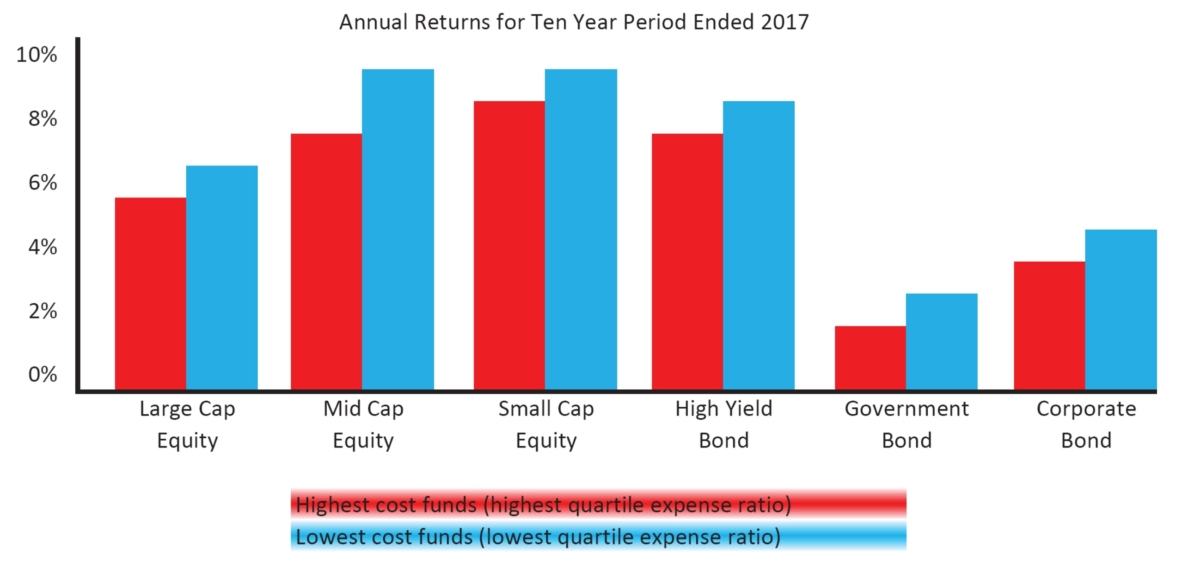

One final chart to hammer home the point that you do not always get what you pay for. The red bars represent the highest cost funds and the blue bars represent the lowest cost funds for various asset classes for the ten-year period ended 2017. In every category, the low-cost fund outperformed the high-cost fund!

TAKEAWAY #7: Invest in indexes; don’t be a fool and try to beat the market!

TAKEAWAY #8: Do not try to time the market—you can’t! Buy and hold is the best long-term strategy.

TAKEAWAY #9: Do not chase returns—Stay the Diversified Course

You should not expect that an investment’s past performance from last year will continue the next year. In fact, most stocks and funds that beat the market in the past generally will not do so in the future.

TAKEAWAY #10: The market always reverts to the mean.

TAKEAWAY #11: Minimize expenses, invest in low-cost index funds.

This excerpt is taken from “Young Adult’s Guide to Investing: A Practical Guide to Finance for Helping Young Peo Le Plan, Save, and Get Ahead” by Rob Pivnick. To read other articles of this book, click here. To buy this book, click here.

The Epoch Times Copyright © 2023 The views and opinions expressed are those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.