Retirement Planning is the most complex chapter in this book, incorporating all of the prior topics, several very complex additional topics, and linking closely to estate planning.

Let’s explore income generation from investing first. A gradual change in portfolio composition—your risk-return profile—along with a specific component that matches guaranteed-to-pay-out expenses to guaranteed income (pension, Social Security, and annuities) is crucial. Let’s start with how non-guaranteed income sources can fail.

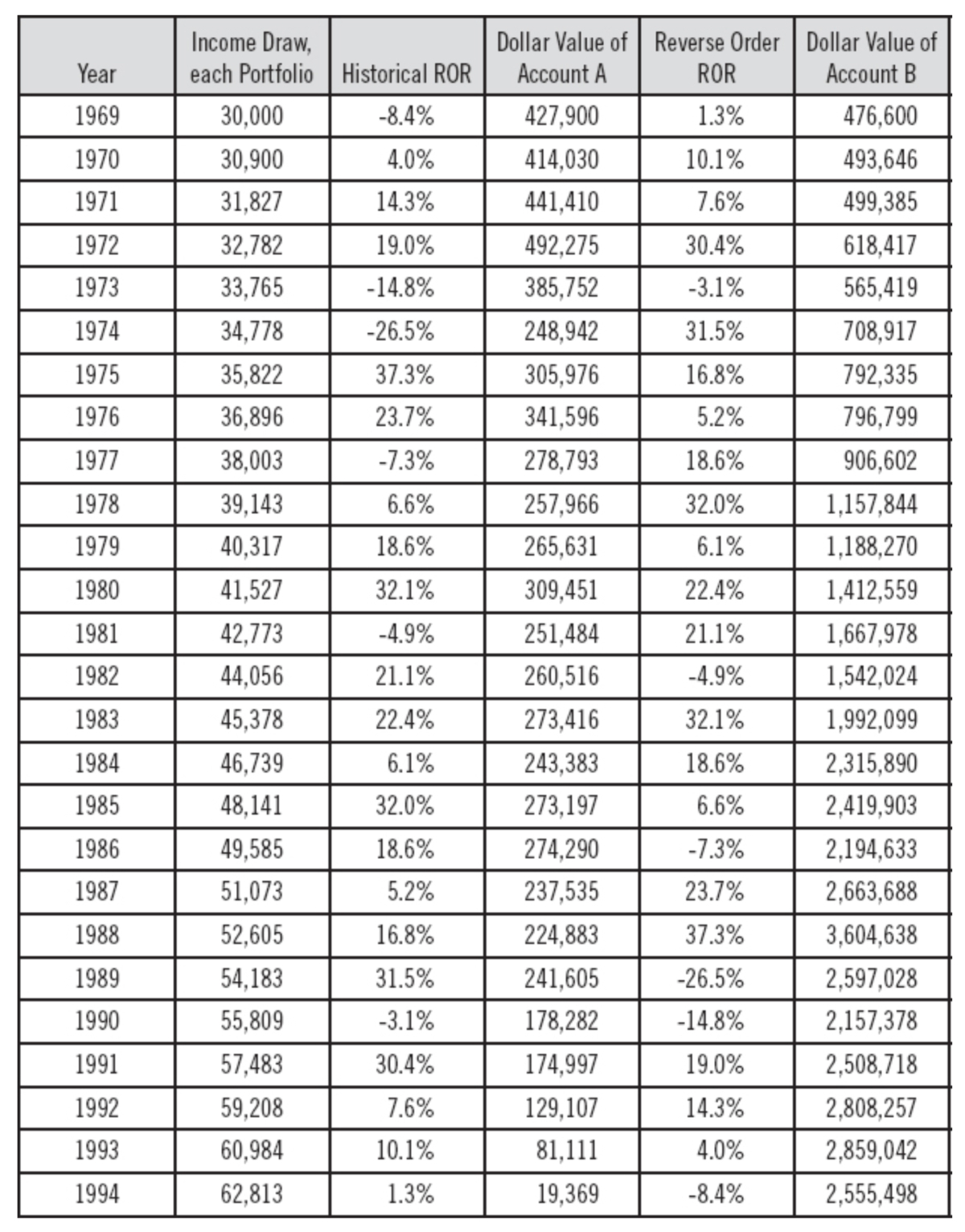

The Order of Returns and Losses

Most people assume that some conservatively estimated rate of return for a portfolio, coupled with a conservatively set withdrawal rate, will result in success in the same way a long- term stock portfolio (e.g., the S&P 500 index) is successful. They assume the portfolio cannot be exhausted with a low withdrawal rate and a high average rate of return. But this is far from true. The chronological order of losses and gains (returns) makes a dramatic difference in success. The following table shows two hypothetical $500,000 portfolios. Each has an identical average rate of return at 11.3% and runs twenty-six years. The income draw is identical, starting at 6% of portfolio value and inflating 3% annually. The only difference between the two is that B has the sequence of returns reversed. While this illustration can work with any time frame and set of returns (hypothetical or real), I picked the starting year of 1969 in order to show a modest loss in the first year and to avoid the anomalous gains and losses of the last quarter century.

By 1994, Portfolio A cannot support the income draw and Portfolio B has almost 132 times the remaining balance, even though the average rate of return is 11.3% for each and the draw is the same! Now, consider that a big withdrawal early in retirement can have the same effect as an early market loss insofar as value is lost (shares are sold off, etc.) when a big withdrawal for that dream vacation (or whatever imprudent treat) is made. So, the lesson is this: In your planning, avoid professionals whose models are not based upon modern portfolio theory (i.e., no Monte Carlo simulations, the recommended portfolios are not on the efficient frontier, and quarterly rebalancing is not done to keep them there).

This leads to an investment maxim credited to Warren Buffett: “Rule No. 1: never lose money; rule No. 2: don’t forget rule No. 1.”

Accumulation And Rollover Strategies

What about changing that portfolio over time to reduce exposure to market losses as you draw income, and as your dependence upon the portfolio grows (i.e., diminished ability to work if you need an income supplement)? There are three approaches to this, and one is popular, yet really bad for you:

- Target-date funds automatically adjust the asset allocation of a portfolio as you approach retirement. These sound nice, but are really designed to protect employers from what might otherwise run afoul of Department of Labor diversification guidelines for retirement plan fiduciaries.

Allow me to categorically dismiss target- date funds as folly: The gradual change from aggressive to conservative composition bears almost no resemblance to the allocation you personally need to target your required rate of return (determined by budget and Monte Carlo analysis, linked to efficient portfolio software routines.) While the target-date fund might be an “efficient” portfolio, it cannot be the efficient portfolio that targets the return you must get in order to maximize the likelihood that your particular eventual withdrawal rate (your budget) can be supported. Avoid target-date funds, including those that purport to adjust throughout retirement. - Investing while looking through a rear-view mirror: The second method of portfolio allocation decision-making is any form of DIY. Here, the temptation is to assume that the available fund with the best return is the one to emphasize, and any diversifying is minimal or essentially random. This applies to any portfolio management, tax-deferred or not, but is especially dangerous in retirement. Remember: well in excess of 90% of returns over decades have been proven to be the result of the asset classes picked. Since you cannot predict the future, the only thing you can control is the risk level for a given target return. Adjusting the asset allocation quarterly or so, using a model that tracks data on the statistical behavior of at least thirty asset classes, is necessary to keep reallocating to an efficient portfolio. Here, though, the DIY person or incompetent advisor can cause harm: without careful examination of the underlying stocks, bonds, derivatives, realty, etc. to correctly identify the asset class for a given fund, a recommended change to the existing portfolio may be incorrect. This may result in an inefficient portfolio that has excessive risk for the actual likely return. If you do not accurately measure the likely return, you could withdraw too much over time, or incur losses that might have been less or avoided. Get a professional to advise you on allocations in your 401(k) as well as other portfolios.

- Proper portfolio management: The third method of managing portfolios is the only prudent one; it was just noted above. If your advisor will not advise you on your 401(k) or other qualified plan assets, get a different advisor for that function. If you are determined to do this yourself, then invest in the programs mentioned in chapter 1 and be sure to pay for the database updates.

Tax-exposed portfolio changes with tax efficiency

By now, you know I will advise that you never let the tax tail wag the investment dog. But efficiency guidelines are essential, otherwise you can easily lose big dollars you need to live on. Two factors will propel your decision to sell off assets to reinvest in something else:

- There is a needed hybrid insurance-investment product

- You must arrange a more efficient portfolio than you currently have

Guideline 1

Have your professional model the tax consequences of the needed liquidation as if it had already been done. What is the likely tax result? If it is not extremely significant compared to the size of your portfolio and other benefits of taking action now, then do it now. But be sure to have him or her also model liquidations over two, three, or four years. If the tax savings of staging the liquidation over several years is significantly better, then take the plunge in stages.

Guideline 2

Some hybrid investments require underwriting that you might fail if you delay, or attractive features might be withdrawn, or rates might increase over time. These are special types of opportunity cost that you must subjectively weight, but never dismiss. Don’t assume your health won’t cause an unexpected bad underwriting decision. Don’t assume that a carrier’s lowered rates will always come back to some rate you saw recently. Over the last three decades, market-risk transfer riders on insurance and annuity products have steadily decreased from “Wow!” to merely “Good” deals. Here are just some examples: Between 2009 and 2012, several variable annuity carriers limited investor asset allocations and also forced policy owners to sell back riders that locked in highest anniversary account value (Investment Advisor magazine, August 2013). This does not occur for equity-indexed annuities (EIAs), but these carriers have begun to protect themselves in event of market corrections.

Twenty years ago, most EIAs guaranteed the higher of two tracked values: cash value, which increases via interest that follows increases in an equity index, and the Income Account Value (IAV), which increases via a guaranteed rate. But today, only a handful of EIAs do this. Most now divorce the two accounts, and income is based upon the IAV only. If the higher of the two is guaranteed, the owner only gets the higher of the two for a set number of years. Hybrid products, like life-long-term care or annuity-LTC products, provide several times your premium deposit as LTC. However, the trend here is also to limit these multiples and rates of interest credited. Since many of these do not allow subsequent premium deposits, or will not advantage later premiums as much as first-year premiums, ask yourself whether the tax savings of spreading capital gains over two or three years is worth the risk of missing out on underwriting or product features.

Guideline 3

A related issue to the capital gain timing decision is the decision to incur a loss (or reduction in gain due to stock or bond market loss) currently. Also, firmly believing that the market is about to “take off” can inhibit the liquidation decision. But consider this: If you are moving from a portfolio that has generally similar relationships of economic conditions to the likely return behavior, then at least you need not fear the issue of selling out at a market low point, or selling out and then missing a recovery from a market low.

Examples: Joe has conservative equities and bonds that have substantial gain, but a market correction has just diminished the gain 20%. Joe wants an EIA to fund his minimum expenses and would have to liquidate half of this portfolio to fund the EIA adequately to provide this segment of his income. He balks until a thought hits him: Realizing a 20% market loss, relative to recent valuation, represents the same amount of (essentially) discount he captures in the equity index of the EIA, so any recovery in stocks he would sell off to buy the EIA will be mirrored in the EIA. Any continuation of loss is not his problem once money reaches the EIA.

Of course, investing in an EIA is not equities investing, and the return is muted because there is a guarantee against any market loss. But he gains that protection, satisfies the “income need” part of his financial plan, and selling his stocks into the down market results in lower capital gains tax (losses offset by tax savings).

Another benefit: Joe can now invest more aggressively with the non-insurance part of his portfolio, because he has the EIA guarantee. FYI, the best models now have databases that properly categorize types of annuities and—provided you would treat some part of life insurance as an investment for eventual income—life insurance. Those modern databases enable correct recommendation of an efficient portfolio, considering such an asset. Those that don’t can still be used by entering guaranteed values as if they were CDs (and separate variable annuity accounts entered subaccount-by-subaccount for accurate treatment).

Once proper planning reveals that your asset allocation should be different—whether you need some lump-purchase insurance product or not—getting what you need is as important as filling a doctor’s prescription. The drug prescription may make you sleepy or prone to infections, but if it extends and improves your life, get it. If the prescription cannot provide this benefit, thank the doctor and find a new one or just live with the malady.

Uncle Sam effectively had a lien on your investment from the day you first had gain (that did not reverse). Weigh a liquidation or switch decision philosophically, subjectively (personal desires, angst over potentially going without guarantees or needed insurance, etc.), and also objectively (expertly estimated dollar values of costs and benefits).

This excerpt is taken from “The Secrets of Successful Financial Planning: Inside Tips From an Expert,” by Dan Gallagher. To read other articles of this book, click here. To buy this book, click here.

The Epoch Times Copyright © 2023 The views and opinions expressed are those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.