How Do I Do This?

Getting started is easy. Just visit the website of one or all of the peer-to-peer lenders and open an account online. It takes just 5–10 minutes. You’ll be asked to link a bank account in order to transfer funds back and forth, but you can opt to simply send a check.

Qualified Investors Only?

Unfortunately, some states do not allow peer-to-peer lending. You can invest if you are you a resident of: California, Colorado, Connecticut, Delaware, Florida, Georgia, Hawaii, Idaho, Illinois, Kentucky, Louisiana, Maine, Minnesota, Mississippi, Missouri, Montana, Nevada, New Hampshire, New Jersey, New York, North Dakota, Rhode Island, South Dakota, Texas, Utah, Vermont, Virginia, Washington, West Virginia, Wisconsin, and Wyoming. This issue seems to be in flux, so check with the P2P websites to confirm the latest rules on who may invest.

Depending where you live, there may be some net worth and income requirements. For example, in most states, investors must have either (1) gross annual income of $70,000 and have a net worth of $70,000, or (2) a net worth of $250,000 regardless of income. In some states, there are no restrictions.

Grading the Loans

Once you are a member, you can start to peruse the loans available for investment. The first step is to determine your personal risk tolerance. There is no correct answer here. Each grade of loan carries a different interest rate based on the risk level.

Investors have access to all of the borrower’s credit information (other than the borrower’s identity) and simply shop through the loans à la carte. Conservative investors can select higher-quality loans that carry less risk and lower interest in the mid-single digits, while more aggressive investors may be drawn to the higher risk loans that accrue interest at over 25 percent. These more aggressive investors understand that a larger portion of the loans will default, but they expect the high interest rate to more than make up for the default rate. Note that the chart above reflects the interest rates charged for each grade of loan. This is not the actual return that investors have earned after defaults are included.

Factoring In the Expected Default Rate

Of course, all P2P investors will suffer a percentage of defaults. It is unavoidable and will reduce profits. This risk cannot be entirely avoided but can be managed through loan selection.

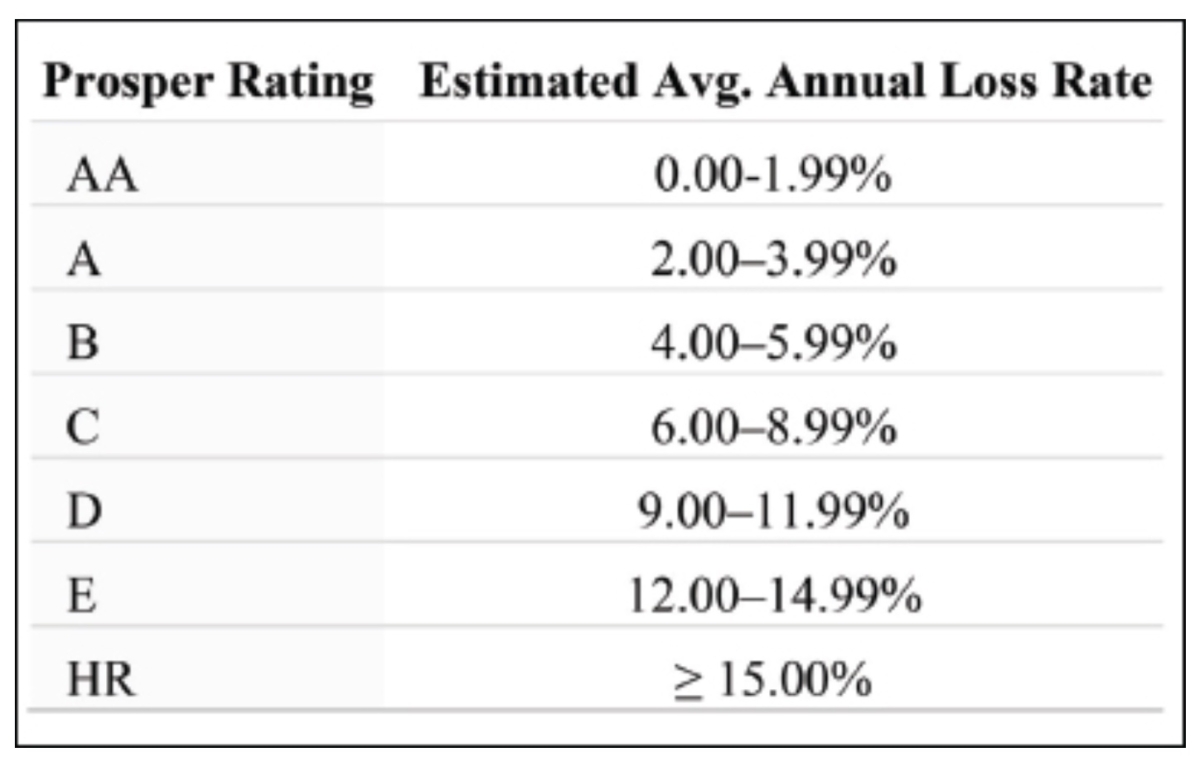

Prosper similarly grades on a scale of AA to E. On its webpage, Prosper provides the historic loss rate for each grade of loan based on the past performance of Prosper loans with similar characteristics. The highest-rated “AA” loans have a historic loss rate of under 2 percent, while the highest-risk loans have a loss rate of over 15 percent.

The estimated loss rates are not a guarantee and actual performance may differ from expected performance, but this sheds light on the risk associated with each grade level. Of course, the lower-grade loans accrue higher interest to make up for the higher default rate.

Some Flaws with Historic Stats

Some statistics and charts on default rates may be less significant than they seem, due to the enormous increase in the number of peer-to-peer loans in recent years. Most loans don’t default immediately—it takes time to see if a given loan will default. Because a large percentage of all P2P loans are relatively fresh (issued in the past six to twelve months), these fresh loans have not ripened to the point of default yet, so they skew the statistics. In other words, a fresh loan that just closed last month should not be included in default stats because it has not aged long enough to carry any weight in a statistical analysis.

Most stats on default rates typically do not take this “aging” into account. The most accurate statistics only evaluate aged loans—leaving out loans that were originated in the past two years. The ideal stats are based only on loans for which the term has been completed. Prosper provides loads of data and charts on their sites, and it is critical for investors to spend some time to gain an understanding of past performance. There are also a few independent websites (listed at the end of this chapter) that provide great analysis.

A lot has been written about default rates and loan purposes. There seems to be a pattern of higher default rates for loans with a stated purpose of business, education, renewable energy, moving expenses, and medical expenses. These statistics are of questionable value for two reasons. First, the loan purpose is not verified. Second, the majority of loans are clustered in the area of debt consolidation and credit cards, so the other purposes may be statistically insignificant.

Perhaps the biggest issue with P2P default statistics is the short history of this sector. P2P lending is no new that we don’t have decades of default statistics to evaluate.

Diversifying Your Portfolio of Loans

Diversity is an advantage for any type of investment because in simplest terms, it spreads the risk. There are a few ways to diversify a loan portfolio. In order to spread the risk of default, investors can spread their funds among many loans. The minimum participation is just $25 per loan, and most investors take advantage of this feature to spread their investment among dozens of loans.

Investors also can also increase diversity by selecting loans among different grade levels—sprinkling in a few lower-grade loans to increase the return, while not wading too deeply into the higher-risk loans. The loan term is another variable that can be mixed in. Longer-term loans generally accrue higher interest. The loans are all relatively short term—twelve, thirty-six, or sixty months—and monthly payments are deposited directly into the investor’s account to be either reinvested into more loans or transferred to the investor’s bank account.

Diversification can also be increased by investing through a variety of P2P platforms.

Selecting Your Loans

There are a few ways to build a portfolio of loans. Investors can select individual loans or use an automated feature that selects loans for you based on criteria that you set. Sifting through the list of available loans is interesting and educational at first, but if you plan to invest a lot and spread your money among many loans, the process can get tedious rather quickly. It is important for beginners to spend time getting familiar with the data available on borrowers, so every new investor should start out analyzing loans one at a time.

After you get the hang of the process by acquiring several loans, you’ll start to develop your own criteria for choosing loans that appeal to you.

The flow of new loans is not steady, so be patient and keep checking back for new loans that fit your own personal criteria. If you find that your filters do not produce any loans over a period of time, then your filters are not set in a realistic model. You will not find high-interest loans with impeccable credit history. Try to reset the filters, or perhaps this investment is not fitting for you. There are plenty of other places in which to invest your funds.

Secured P2P Investing

Some peer-to-peer lenders even offer loans that are secured by a lien on real property or the debtor’s assets. These sites, like Realtyshares.com, Sharestates.com, Realtymogul.com, and many others link up investors with borrowers for mortgage loans to participate in mortgage loans. Uhaulinvestorsclub.com allows investors to participate in loans to the parent company of U-Haul, and the loans are secured by U-Haul’s trucks, trailers, or equipment. There are a lot of options, and more keep springing up.

(In the next section, you will see some expert insight on P2P lending.)

This excerpt is taken from “How to Invest in Debt: a Complete Guide to Alternative Opportunities” by Michael Pellegrino. To read other articles of this book, click here. To buy this book, click here.

The Epoch Times Copyright © 2023 The views and opinions expressed are those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.