Qualified Investors Only

Unfortunately, there are also some net worth and income requirements. In most states, investors must have either a net worth of at least one million US dollars, excluding the value of one’s primary residence, or have income of at least $200,000 each year for the last two years (or $300,000 combined income if married).

Pricing

Pricing is not set in stone and depends on the demand from investors. This is one of the challenges that investors face, because there is no public listing of prices like the stock exchanges. Generally, the price that an investor pays to buy a life settlement is based on these factors:

- Amount of the death benefit that will be paid upon the death of the insured;

- Amount of the annual premiums that the investor will have to pay until the policy is paid in full or until the insured passes away;

- Life expectancy for the insured.

For example, if you could buy a $75,000 life insurance policy for $20,000, and there was an additional $15,000 to be paid in premiums, plus $2,500 in commissions, the investment analysis would be as follows:

$75,000 Insurance Death Benefit payment from Insurance Co. to Investor -$20,000 Initial Investment Paid to Buy the Life Insurance Policy -$15,000 Remaining Annual Premium Payments to be Made by Investor -$ 2,500 Commission $37,500 TOTAL PROJECTED PROFIT

This projected $37,500 profit would be quite attractive on an investment of $20,000, but the issue (like many things in life) is timing. If the policy paid off in just two years, then you’d have doubled your investment in two years for an annualized return of 50 percent. That would clearly be an unusual outcome—a home run. If, however, the insured has a nice long life of another twenty years, your near $38,000 profit would equate to an annualized return of just 5 percent.

What About The Sellers?

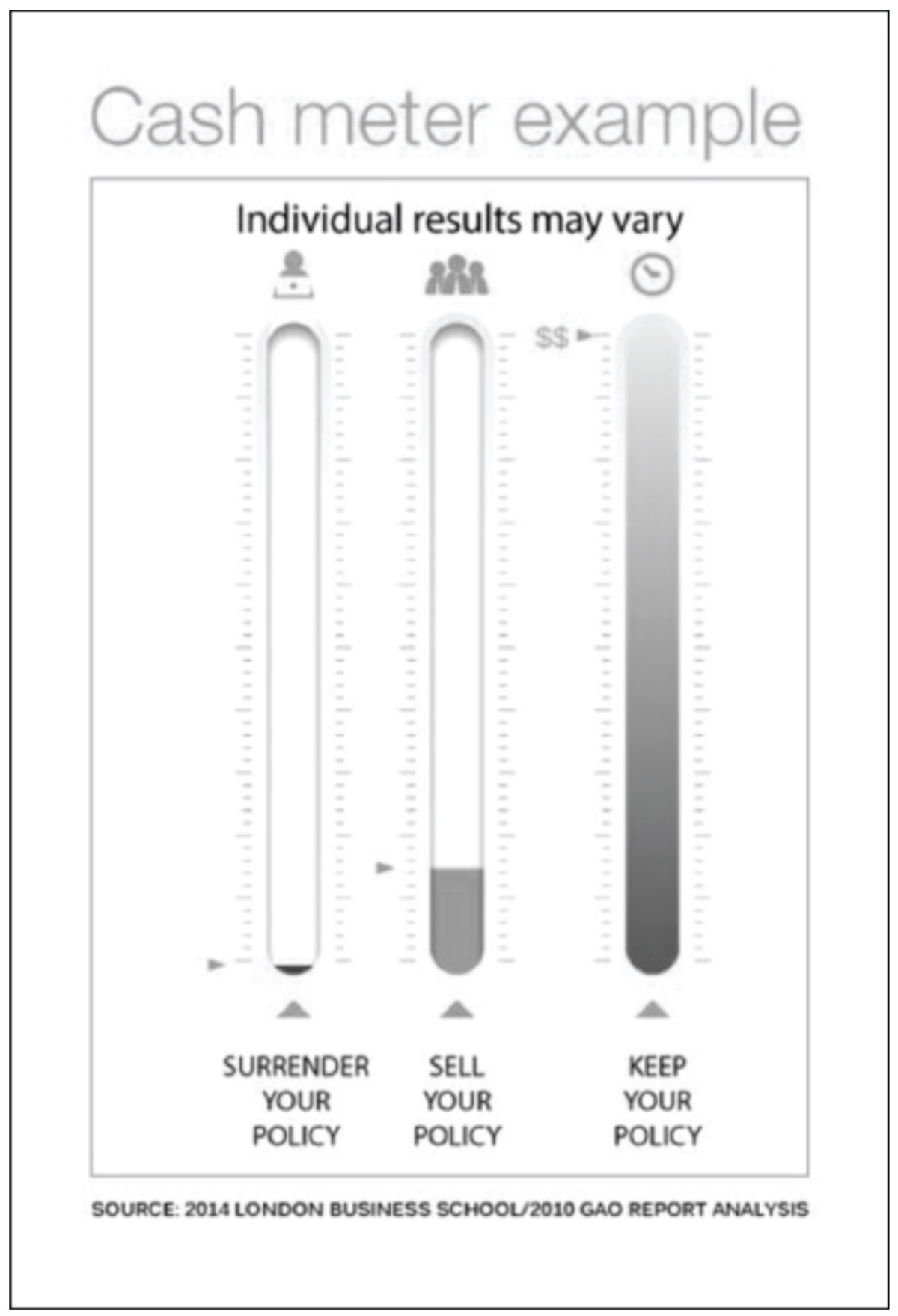

This is an investment book, so of course we are focused on the buyer’s side of the transaction, but it always helps to understand the other side of a transaction. The amount that a seller will receive from selling a policy will always be greater than the cash surrender value and less than the death benefit value. This chart published by the Life Insurance Settlement Association illustrates the comparison between surrendering a life insurance policy for its cash value compared to selling the policy or holding it to maturity:

Of course, holding the policy for the eventual death benefit provides the highest payoff, but people who sell their policy have pressing reasons to cash out. Independent studies of life settlement deals have confirmed that sellers receive at least four times more than the cash value of the policy.

We have already addressed a few of the reasons why an insured may want (or need) to sell a life insurance policy, but here is a basic summary of the issues that sellers must face:

• Pricing There is no organized market with publicly listed pricing, so it is difficult for sellers to determine whether they are getting a fair price for their life insurance policy unless they shop around, offering the policy to several agents. Generally, a seller should expect to get about four to five times the cash value of the policy.

• Fees Fees and commissions are often high. Both buyers and sellers should ask for a list of all fees and commissions.

• Cash Value Whole life policies have a “cash value” that the insurance company would pay to cancel the policy. Sellers should obtain the current cash value and expect to receive a net sale price of about four to five times the cash value.

• Tax & Public Assistance A large payment from the sale of a policy could trigger negative implications if the seller received benefits such as food stamps, Medicaid, or social security. A portion of the sale proceeds maybe taxable.

• Medical Records In order to sell a life insurance policy, the insured must be willing to disclose current medical conditions and medical records to the agent and buyer. The buyer may periodically make future medical health inquiries, so be aware of the process and limitations of these periodic health inquiries.

• Buyer’s Identity The seller must be aware that an investor will have a financial interest in the seller’s death.

• New Insurance? Sellers often intend to use a portion of the sale proceeds to buy a smaller or less costly policy. In this scenario, the seller should confirm the cost of the new policy before selling the old policy.

• Age Sellers must be 65 or older.

Unfortunately, just as very few investors are aware of this opportunity, most people who hold life insurance policies are also unaware that they can sell it. Coventry First, a life settlement company, surveyed 604 seniors citizen in 2016 and reported that 86.1 percent were not aware of the option to sell their life insurance policies. This means that the market could be much larger for investors as the public becomes more aware of this opportunity.

History of Fraud & Abuses

One of the reasons that this investment has not gained more popularity is that it has been the subject of fraudulent schemes in the past. Unscrupulous people have ripped off investors through various “Ponzi” schemes in which investors are led to believe that they have purchased shares in a life settlement but their money had not been invested at all. Others have taken advantage of seniors by tricking them into selling valuable life insurance policies for a fraction of the real value.

As with any investment, we must be diligent and skeptical before writing a check. Only work with legitimate life settlement companies with references and long, proven track records. Only buy policies from “A”-rated life insurances companies licensed inside the United States. Get a copy of the life insurance policy and read it before you invest.

Why It Works

So what is the market theory here? In short: a lack of investor demand creates opportunity for high returns. Most investors are not even aware of this opportunity. Many of those who are familiar with this investment vehicle are scared off by the perception of a morality or “ick” factor. Others will not accept the term risk–unknown payoff date.

Investments like this with some undesirable aspects and narrow market appeal create opportunity for those who can accept and see past the “warts.” Like the other investments featured in this book, this is not for everyone. It is similar to buying the “ugly” house on the block with broken windows, peeling paint, and overgrown shrubs. The average home buyer turns up her nose and runs away. Investors who can see past the flaws and recognize the value can make above-market returns.

As noted above, most investors who do take the time to understand this opportunity get stuck on the risk associated with trusting the trustee. This is a different situation from mortgage-backed securities (“MBS”) to be discussed in Chapter 10. For MBSs like FNMA and GNMA, the trustee is a federal agency, so there is no risk of fraud or a “Ponzi” scheme. Even for private label MBSs, the trustee is typically a well-known bank or large American insurance company. I would not invest in a mortgage-backed security if the mortgages were not held by an extremely trustworthy trustee like a federal agency. This is the main factor that has prevented me from investing in life settlements. I simply can’t trust the trustee who is designated to hold the life insurance policy.

This is a situation that seems to call for government intervention. FNMA and GNMA were formed to facilitate funding of mortgages by pooling them and then reselling shares in bonds that are secured by the pool of mortgages. If a government agency were formed to perform the same function for life insurance policies, it would eliminate risk and facilitate the sale of life insurance policies and the resale of fractionated shares to investors.

What Can Go Wrong

1. Interest Rate Risk: The resale value of a life settlement will fluctuate as market interest rates change. If prevailing interest rates rise then the resale value of your investment will be reduced.

2. Extension Risk: There is no way to accurately predict the term of this investment.

3. Premiums: The investor is responsible to make any annual premium payments. Many whole-life insurance policies are “paid in full” at some point, so no further premiums must be paid, but investors must determine what premiums payments (if any) must be paid. Obviously, any premium payments cut away at profits.

4. Default Risk: Default risk is extremely low. State regulations ensure that life insurance companies maintain adequate reserves. In the unlikely event of insolvency, states maintain a safety net in the form of guaranty funds to cover policies.

5. Term Insurance Policies: Term life insurance expires after a set period of years. The policy is worthless if the insured lives beyond the set term of years. Since there is no way to determine whether the insured will outlive the term of the policy, it is pure speculation to buy a term policy. Experienced, disciplined investors will only consider a term policy if it can be converted into a whole life policy.

6. Incontestable: Investors should only consider policies that are “incontestable.” Generally, insurance companies may “contest” or challenge payment on an insurance policy that is less than two years old or various reasons including false information on the application or suicide. Always determine contestability terms before you invest.

7. Group Policies: Many people obtain life insurance through a group policy arranged by the insured’s employer. These group policies can be purchased, but investor must determine what will happen if the employment is terminated or if the employer simply terminates the policy. Under these circumstances, the investor typically has the right to convert the policy and make the premium payments, but the investor must be aware of all rules and conditions.

8. Tax Issues: Life settlements may be purchased through a retirement account, but check with a tax advisor for details in your particular state.

9. Fraud: As discussed above, there is a history of fraudulent schemes by life settlement companies, and it is very difficult to sniff out a Ponzi scheme.

Summary of The Pros & Cons

Pros

- High potential return: Potential profit is comparably high.

- Diversity: Life settlements provide a hedge against other investment asset classes such as stocks or bonds. Regardless of the economy, investors hold a contractual right to be paid a predetermined sum of money.

- Security: Life insurance policies are considered to be rock-solid due to government regulations and cash reserve requirements.

- Scalability: There are plenty of opportunities, if your financing allows for multiple purchases.

- Stability: No “market swings” like the stock market or mutual funds.

Cons

- Repayment Delays: The “term” or date of repayment is uncertain.

- Morality: Some investors are uncomfortable with profiting on the death of another.

- Illiquid: This is a long-term investment with an uncertain payoff date.

- Capital requirements: The cost of buying life settlements ranges from$10,000 into the millions.

- Fraud Potential: Many investors pass on this opportunity due to the history of fraud.

Hungry for More? Source Books:

Bonded Viaticals & Life Settlements, Gloria Wolk

Understanding Life Settlements, David Isaacson

Billion Dollar Blue Print: What Big Banks Don’t Want You to Know about Life Settlements, Stephen Gardner (2014)

Testing for Adverse Selection of Life Settlements: The Secondary Market of Life Insurance Policies, Life Settlements Study—2013 University of London; Dr Narayan Naik, Professor of Finance; Joint Chair, Finance Faculty

(To be continued...)

This excerpt is taken from “How to Invest in Debt: a Complete Guide to Alternative Opportunities” by Michael Pellegrino. To read other articles of this book, click here. To buy this book, click here.

The Epoch Times Copyright © 2023 The views and opinions expressed are those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.