Premiums & Discounts

New bonds are issued at “par,” which means price is equal to the face value of the bond. Like any other bond or security, MBS bonds may be resold and traded in the secondary market. If you are buying a bond in the secondary market, it may be priced at par, at a discount or at a premium based on how interest rates have changed since the bond was issued.

Par: If interest rates in the marketplace have not changed since the bond was issued, the bond will likely trade at close to par, which is the face value of the bond.

Discount: When market interest rates increase, it reduces the value of bonds that were previously issued with lower interest rates. Why would an investor buy your older bond yielding 2 percent when similar new bonds are being issued with a 3 percent yield? The only way to attract a buyer would be to discount the price so the effective yield would match the current market rates.

Premium: On the other hand, if interest rates drop in the market, then your higher yielding “old” bonds will increase in market value. This is because the market will adjust the value of your bond to reflect that it accrues interest higher than the market rate. Investors would rather buy your higher-yielding bonds than the new lower-yielding bonds, and they will pay more for it.

Principal Paydown: Of course, the price will also reflect how much of the bond has already been paid off. Principal and interest payments are collected and distributed to bond holders each month, so as the bond ages, the principal due on the bond is paid down and the value of the bond is reduced.

Keep in mind that these price fluctuations only apply if you sell your bond. As long as you hold the bond to the end of its term (to“maturity”), you will be paid all of the principal and interest. You will see a “paper loss” or “paper gain” on your monthly brokerage statements, which list the current market value of each bond, but you will not incur the gain or loss unless you sell the bond before it matures.

Types of MBS Bonds

MBS bonds are created or “issued” by a variety of government and private entities. Characteristics and risks of the MBS vary depending on the issuer, so it is critical for investors to be familiar with each type of MBS. There are four general types of mortgage backed securities:

1. Government National Mortgage (“GNMA” or “Ginnie Mae) is an agency of the federal government created to ensure that mortgage loans are available throughout the country. GNMA bonds are guaranteed by the “full faith and credit” of the United States Treasury, so even if every mortgage in the pool were to default, the investors would still be paid in full. The only down-side is that the bonds are sold in $25,000 minimum increments, as opposed to the other MBS bonds that are offered in $1,000 increments. GNMA bonds can be bought for less than $25,000 on the secondary market as they are paid down and closer to maturity. Individual investors can also buy a GNMA mutual fund or ETF, but they differ significantly from an individual bond.

2. Federal National Mortgage Association (“FNMA” or “Fannie Mae”) is a publicly owned corporation that was formed by the federal government to increase and support the secondary market for home mortgages. It buys mortgages from banks. It is also not a government agency, and the bonds are not explicitly guaranteed by the US Treasury, so they are considered slightly riskier than GNMA.

Although it is not a governmental agency, it was formed by the federal government and its bonds are guaranteed by FNMA as the issuer. It is widely considered that FNMA is “too big to fail,” so investors generally believe that the federal government would not allow it to default on its MBS bonds. Accordingly, the market deems these bonds to be “implicitly” guaranteed by the fed and extremely secure, so these bonds yield just slightly more than fully guaranteed GNMA bonds. FNMA Bonds are issued in $1,000 increments.

3. Federal Home Loan Mortgage Corporation (“FHLMC” or “Freddie Mac”) is also a publicly owned corporation that was formed by the federal government to increase the home mortgage market. Like FNMA, Freddie Mac is widely considered to be “too big to fail,” so the public considers the bonds to be extremely secure. Freddie Mac bonds are also issued in $1,000 increments.

4. Private mortgage-backed securities. Large financial institutions like Goldman Sachs and J.P. Morgan Chase create private mortgage-backed securities, based on pools of mortgages that are held in a trust for bond holders. The government has no involvement, so there is no direct or implied government guarantee, and these bonds accordingly carry a higher yield. These “private label” bonds may be offered with insurance that greatly reduces risk.

Variations on How MBS Bonds Are Structured:

Here is where it gets a bit more complicated. Creative financial companies have devised ways to repackage MBS bonds to better fit investors’ needs.

“Pass-through” MBS: This is the standard straightforward type of MBS. The issuer, GNMA for example, collects payments from a large batch of mortgages and “passes through” the collected principal and interest to the bondholders. Funds are collected from three sources: monthly payments of principal, monthly payments of interest, and prepaid principal (when the homeowner refinances or sells the home.) The bond term extends until the last mortgage is fully paid off, so the date of final payment is uncertain. As explained above, the long and uncertain repayment term is undesirable for some investors who wish to avoid prepayment and extension risk.

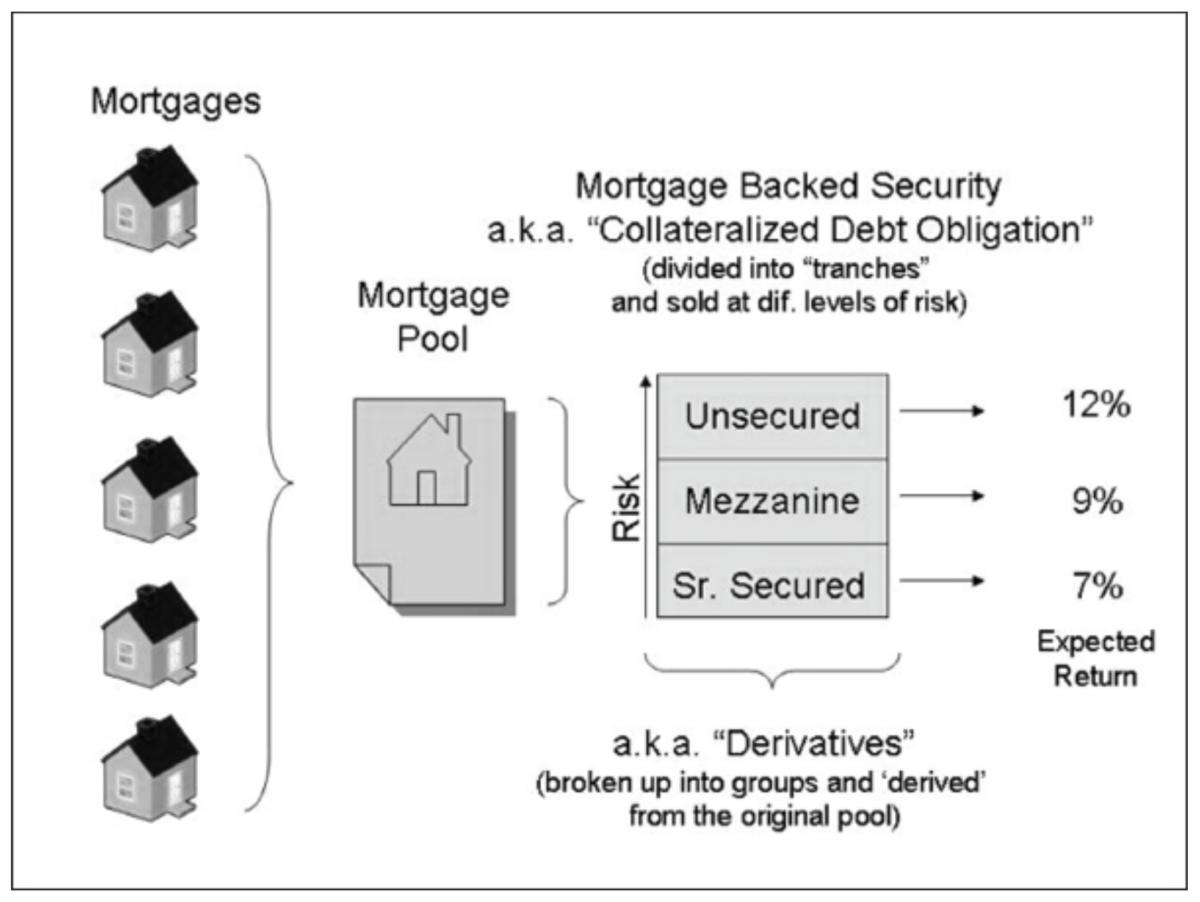

Collateralized Mortgage Obligations (CMOs) are designed to improve pass-through mortgage-backed securities by making repayment more predictable. CMO sponsors bundle together a bunch of mortgage-backed securities and repackage them with a prioritized order of payment. Cash flow is segregated into different bond classes known as “tranches,” which is a French term for slice. Each tranche is assigned an order of priority for repayment. The tranches are designed to provide investors with more predictable repayments.

Some CMOs have a dozen or more tranches, and they can be structured in limitless ways to create tranches to perform in different predictable ways to suit different investors.

Real Estate Mortgage Investment Conduits (“REMICs” or “Conduits”) are similar to CMOs but have more complex tranches. Instead of just slicing tranches up by the order of repayment, REMICs also sort mortgages by risk. Some tranches include only the highest-quality, lowest-risk mortgages, and others include the lowest-quality, highest-risk mortgages. Investors can choose the quality that best suits their need.

Yes, These Are “Derivatives,” But Don’t Be Afraid:

An MBS is considered to be a “derivative” investment because it is “derived” from a different investment. It is a bond that is derived or created from a pool of mortgages. Many investors have a vague conception that derivatives are bad. This reputation was generated through a series of financial scandals that involved complex and misleading derivative investments. Not all derivatives are bad, and government MBS bonds are widely considered to be a safe income investment.

This diagram is an example of how a CMO may be structured:

Commissions & Fees

Buyers generally do not pay a commission or fee to invest in an MBS. Brokers make money by buying large batches of MBS bonds and then reselling them at a higher price.

Structuring a “Ladder” of bonds:

A common technique for managing interest rate risk is to build a portfolio of bonds with different maturity terms, so that a portion of your principal is always invested in higher-yielding long term bonds and a portion of your bonds is always close to maturity, so the funds can be reinvested at the current interest rates. For example:

20% of Bond Portfolio 10-Year Term Bonds

20% of Bond Portfolio 8-Year Term Bonds

20% of Bond Portfolio 6-Year Term Bonds

20% of Bond Portfolio 4-Year Term Bonds

20% of Bond Portfolio 2-Year Term Bonds

No one can consistently predict the fluctuations of interest rates, so this ladder approach allows you to diversify your bond portfolio with both long- and short-term bonds. When the 2-year bonds mature, the funds are reinvested into a new 10-year bond. And when the 4-year bonds mature, once again, the money is reinvested in new 10-year bonds. By following this process, you will build a portfolio of 10-year bonds (earning higher, 10-year yields) maturing every 2 years to be reinvested into high-yielding 10-year bonds.

Why It Works

No one is going to “beat the market” buying MBS bonds. This is designed as a safe portion of a portfolio. Income-seeking investors are attracted to MBS bonds because they yield more than bank CDs and because of the federal government’s explicit (for GNMA) and implicit (FNMA & FHLMC) guarantees. The federal government has determined that the overall economy is at least partially driven by homeownership, so these agencies were created to insure that mortgage loans are readily available throughout the country. The sale of MBS bonds provides funding for the nationwide mortgage market, so there is always a strong supply of bonds for investors, and the federal government will undoubtedly protect this market from default.

What Can Go Wrong:

1. Interest Rates Risk: A bond’s resale value will fluctuate as market interest rates change. A bond’s value has an inverse relationship to market interest rates. If prevailing interest rates rise higher than your bond’s rate, the resale value of your bond will be reduced. On the other hand, your bond’s resale value will increase if market interest rates fall. In any event, an investor who holds a bond for its full term will receive the principal and interest rate paid in full, regardless of prevailing market interest rates.

2. Prepayment Risk: MBS bonds may be paid off early if the underlying mortgages are paid off earlier than expected. This occurs more often as prevailing interest rate are falling. The MBS bond will be paid off earlier, and the investor will have to reinvest, possibly at a lower yield.

3. Extension Risk: This is the opposite of “prepayment risk.” MBS bonds may be paid off more slowly than anticipated if the underlying mortgages are paid off later than expected. This occurs more often as prevailing interest rates are rising and the mortgage debtors are less likely to refinance or pay off the mortgage. The MBS bond will be paid off later, delaying the investor’s ability to reinvest in new higher-yielding bonds.

4. Delayed Reinvestment Risk: As small portions of the investor’s principal are returned each month, they may sit idle for a period of time before being reinvested, and they may have to be reinvested at a lower yield.

5. Default Risk: There is no risk of default for GNMA bonds, which are guaranteed by the full faith and credit of the United States Treasury. Although there is a technical risk for default for bonds issued by FNMA & FHLMC, they are considered to be extremely secure. MBS bonds issued by private banks and financial companies are subject to possible default.

Summary of the Pros & Cons

Pros

Diversity: Mortgage-backed bonds provide diversity from stocks and general economic swings.

Security: There is no risk of default for GNMA bonds, which are guaranteed by the full faith and credit of the United States Treasury, and extremely low risk of default for Fannie Mae and Freddie Mac bonds, which the market considers to have an implied guarantee.

Scalability: Almost unlimited supply of MBS bonds. Stability: No major “market swings” like the stock market or mutual funds.

Cons

Low Yield: Due to the low-risk nature of MBS bonds, the yield is low.

Hungry for More?

Mortgage-Backed Securities, Justin Adams

The Handbook of Mortgage-Backed Securities, Frank Fabozzi

This excerpt is taken from “How to Invest in Debt: a Complete Guide to Alternative Opportunities” by Michael Pellegrino. To read other articles of this book, click here. To buy this book, click here.

The Epoch Times Copyright © 2023.