What do you think of this investment opportunity? You loan your hard-earned cash to a stranger whom you will never meet. The loan is unsecured, so you will not hold a mortgage lien or any type of collateral to secure the repayment of the loan. If the borrower defaults, you cannot file a collection lawsuit. You will have no control over the collection efforts. A third-party servicer (who arranged the loan) will decide whether to make any collection efforts, or write off the loan on your behalf. Sound appealing? Of course not, but don’t turn to the next chapter just yet: you may feel differently if you read the next few pages. After accounting for defaults, investors who diversify among many small loans can make net returns of 5 to 10 percent just sitting at a computer.

Summary Points

- Specialized Knowledge: None

- Minimum Capital Requirement: $2,500

- Scalability: Yes

- Liquidity: Limited; resale of the accounts is not well organized

- Priority over other forms of debt: Not secured by a lien

- Barriers to Entry: Not available in some states, and in some States open only to “Qualified Investors”

What is Peer-to-Peer Lending?

Peer-to-peer lenders such as Prosper provide online marketplaces that originate loans of up to $35,000 and offer investors an opportunity to participate by financing a portion of the loan. Their goal is to “disrupt” or transform the traditional bank lending industry to reduce costs and increase transparency and efficiency. Through their websites, they connect borrowers and investors and provide related services including screening and grading borrowers, and collecting and processing monthly payments for the investors.

The idea is simple and appealing: Use the Internet to cut out the middleman (banks) from typical loans. Under the traditional banking system, investors deposit their extra money in banks and earn a very low interest rate (recently under 1 percent). The bank then loans the funds to borrowers at higher rates of interest based on the borrower’s credit history. The bank sets the interest rate based on various factors such as the borrower’s credit score, income level, employment history, and the length of the loan.

Higher risk loans earn higher interest to offset the higher risk of default. The bank takes on the risk of default, collects the loan payments, and makes a profit based on the difference between the low interest rate that it pays to investors for their deposits and the high interest rate that it charges on the loans.

The peer-to-peer investment model allows the investor to take on the role of the banker and earn an attractive rate of interest. In some ways, it is the Uber of loans.

What about the Risk of Default?

For hundreds of years, banks have used a variety of lending criteria to evaluate credit risk, and these techniques are not secret. P2P lenders such as Prosper evaluate each proposed loan and rank them based on the same criteria that the banks apply. The loans are screened, graded, and assigned an interest rate that reflects the level of risk. Of course, the riskiest loans are weeded out and rejected.

Investors then review the graded loans and select loans in which to participate. Members have access to the borrower’s credit data including income level, FICO score, default history, and debt load. One of the best features is that you do not have to provide funding for the entire loan. Most investors elect to “participate” in many loans by funding small pieces of a lot of loans. Investors may invest as little as $25 in a loan to spread the risk among many loans.

If a loan is fully funded by investors, then the servicer closes the loan and manages the monthly payments. Monthly payments of principal and interest are transferred into the investor’s account. If there aren’t enough investors willing to pitch in to fund a loan, then the loan is rejected.

Why Investors Should Consider This

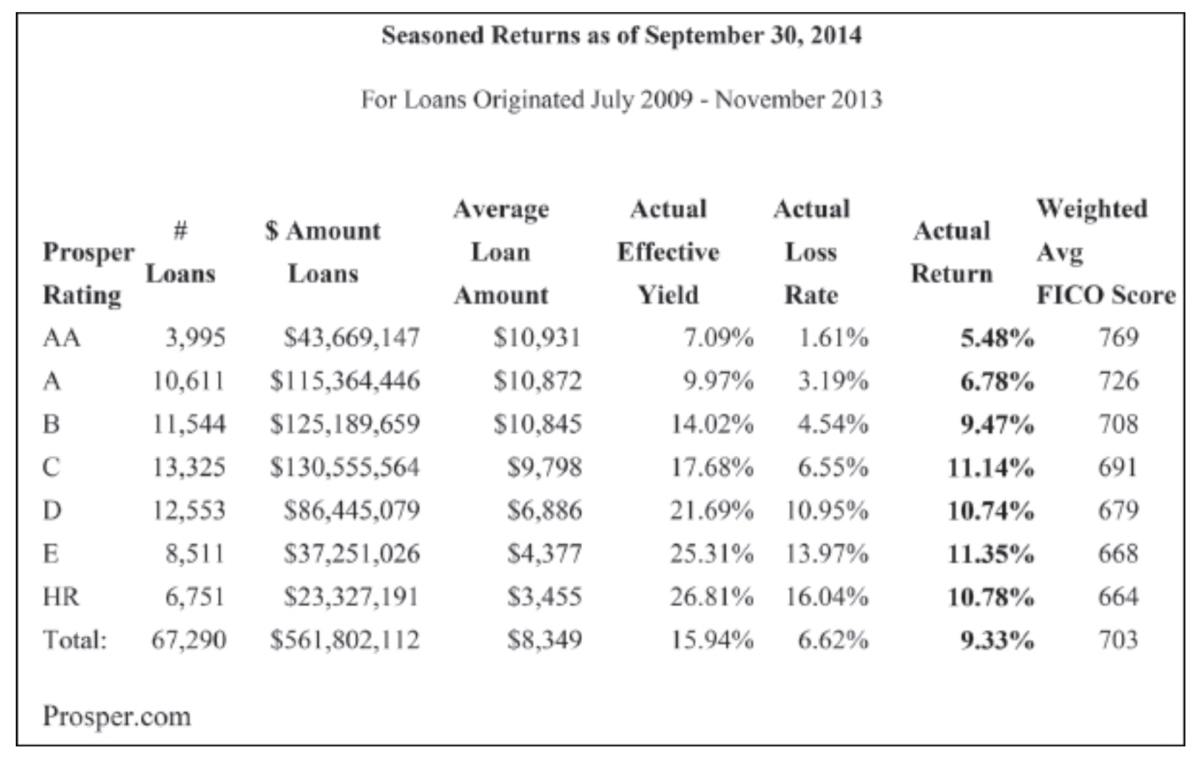

Returns have been attractive. According to figures posted by Prosper (chart below) on its website, its highest graded loans have generated a net return of 5.48 percent. The “AA” graded loans carried a 7.09 percent yield and had a 1.61 percent rate of write-offs, which left a net yield of 5.48 percent. Lower graded loans generated higher profits even though they suffered higher loss rates, because the interest rates on the higher risk loans offset the higher loss rate.

Some deep-pocketed investors have taken notice. In 2013, Google led a round of private investors that bought a $125 million stake in Lending Club, valuing the company at over $1.5 billion. Lending Club then went public in late 2014. Prosper also landed a $20 million investment from Sequoia Capital. Goldman Sachs has launched its own direct lending site, called Marcus. There are many P2P sites in Europe, China, Japan, and India, as well.

Unfortunately, P2P lending is a relatively new asset class and has not been approved for investors in every state. More states are being added, so check the P2P websites for an updated status on your home state. As of the writing of this book, the following states allow residents to participate:

Alaska, Arizona, California, Colorado, Connecticut, Delaware, Florida, Georgia, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, Massachusetts, Minnesota, Mississippi, Montana, Nebraska, Nevada, New Hampshire, New Jersey, New York, Oklahoma, Rhode Island, South Dakota, Texas, Utah, Vermont, Virginia, Washington, West Virginia, Wisconsin, Wyoming.

Why Aren’t Default Rates Higher?

Unsecured loans are very hard to enforce and collect, so investors often wonder why there isn’t a higher rate of default. Why are these borrowers paying off their loans? The answer seems to be that the credit system simply works. Banks have proven that this model works through their credit cards—which are unsecured, low-balance consumer debt, just like P2P loans. There are two strong factors at work to keep defaults down. First, the peer-to-peer sites screen the borrowers (just like the credit card companies) and weed out the borrowers who are most likely to default. Borrowers with the worst credit history do not make it onto the P2P sites. Second, borrowers have strong incentive to pay back the loans in order to preserve their credit scores. Our society has become more and more reliant on credit. Borrowers are well aware of the negative impact that a default will have on their credit score—which will impact their lives for many years.

It is important to understand that all investors will suffer a percentage of defaults. Defaults are part of this investment, but as illustrated in the charts above, the default rate can be overcome by the high interest rates if the loan portfolio is properly diversified and spread out among many quality loans.

Why Borrowers Like P2P Lenders

Following the Great Recession of 2007–2009, it has become much harder for borrowers with imperfect credit ratings to obtain loans. Borrowers seem to be flocking to peer-to-peer lending as a simpler, lower-cost, and faster option. The borrower fills out forms online explaining the purpose of the loan, authorizing a credit history check, and selecting the term of the loan—either 36 or 60 months. Then, if the loan passes the servicer’s initial screening, the loan will be listed on the website for investors to review and select. If the loan is fully funded by investors, then the borrower signs loan documents and the loan proceeds are transferred into the borrower’s account. Monthly payments of principal and interest are automatically transferred from the borrower’s bank account, and the borrower may pay off the loan early without penalty.

The entire process is done online so borrowers avoid embarrassing, time-consuming meetings with bank loan officers. The online application takes twenty to thirty minutes to complete. Minutes later, the borrower receives preapproval (or rejection), and the proposed loan (of up to $35,000) is assigned a grade and an interest rate. If the borrower accepts the terms, then the loan is posted for investors to select. If investors choose to fund it, the loan can be approved and funded into the borrower’s bank account within days. Traditional banks cannot match that convenience, transparency, and efficiency.

The borrower’s identity is never disclosed to the investors, so there is no opportunity for investors to contact the borrower if the loan is defaulted. Collection efforts, if any, are managed by the P2P lender. The typical collection process includes in-house phone calls and/or letters, then referral to a collection agency, and then possibly referral to a collection law firm. These loans are unsecured, so collection efforts may not be cost-efficient. The P2P lender retains full discretion as to what collection efforts (if any) are warranted.

Borrowers apply for these peer-to-peer loans for a wide variety of purposes including consolidation of credit card debt, to start or expand a small business, to make home repairs, for higher education, or even for vacation expenses.

The majority of borrowers indentify “debt consolidation” or “credit card” as the purpose, but the purpose is not validated or confirmed in any way. Investors must assume that many borrowers do not use the loan proceeds for the stated purpose.

The loan application process is very similar to a standard bank loan application, and if the loan is funded, the borrower can get an interest rate that is lower than a bank would charge.

The P2P servicer naturally charges the borrower an origination fee of 1 percent to 5 percent, depending on the grade of the loan. The servicer also charges a 1 percent processing fee for each monthly payment, and Prosper charges investors a 1 percent annual fee on all loan assets. This is how peer-to-peer sites make their money.

(In the next section, you will see advice on how to do Peer-to-Peer Lending.)

This excerpt is taken from “How to Invest in Debt: a Complete Guide to Alternative Opportunities” by Michael Pellegrino. To read other articles of this book, click here. To buy this book, click here.

The Epoch Times Copyright © 2023 The views and opinions expressed are those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.