We will all come to that point in our lives when we stop working for a living, and need to rely on whatever sources of income remain. Those sources could be savings, interest, Social Security, even rents from properties purchased earlier.

As the cost of living increases, so will the amount we will need to continue our accustomed standard of living when retirement rolls around. We can start early and build savings, but it is the compounding effect of interest that will expand our total savings far above the amount we set aside.

Setting Your Retirement Goal

Experts recommend that your annual retirement income goal should be about 80 percent of your final pre-retirement annual income. In other words, if you make $100,000 a year before retirement, after retirement, you will need $80,000 a year to live the lifestyle you are accustomed to.While investment returns vary considerably over time, the underlying assumption here is that you will make a 5 percent average annual return on your investments.

Tracking Your Retirement Progress

Experts recommend that you save at least 20 percent of your income each year, but 25 percent is preferable, giving you a larger safety margin. Another way to see if you’re getting where you need to go, is to look at your current savings based on your age:- Age 35—two times annual salary

- Age 40—three times annual salary

- Age 45—four times annual salary

- Age 50—five times annual salary

- Age 55—six times annual salary

- Age 60—seven times annual salary

- Age 65—eight times annual salary

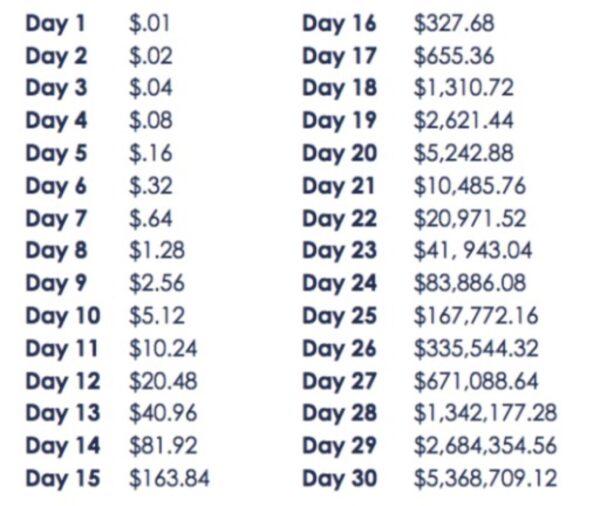

From a Penny to $5 Million

The amazing math of compounding can be demonstrated by an example. If you start with a penny, double it the next day, double the higher amount the following day, and continue this pattern for 30 days, you will end up with well over $5 million!

The Rule of 72

The rule of 72 is a handy formula to calculate how long it will take to double your savings, given a fixed annual rate of return. Divide 72 by your investment’s interest rate: in our example of 5 percent per year investment return, it will take 72 divided by 5–or 14.4 years–to double the initial amount. Taking an extreme case of only 1 percent– more than most savings accounts pay in interest today–it would take 72 years to double your initial savings.

Raiding Your 401(k)

In addition to the Social Security that will help support your annual expenses, it’s wise to take full advantage of your employer’s 401(k) match, by electing to deduct the maximum amount your company will match.Summary

Most Americans don’t begin to provide for retirement at the start of their working life. There are many reasons for this, including student loans and low paying initial jobs. It is a challenge to save at a young age, especially to save 20 to 25 percent of income. In addition, the long-time horizon until retirement lulls us into a false sense of security. We think we will have plenty of time to figure out our retirement later in life.However, the sooner you start saving, the less you will need to set aside over the rest of your life. The miracle of compounding takes over. Your nest egg begins to grow. You will be able to look forward to a comfortable retirement, rather than going into your autumn years with financial fear, topping everything else that comes with growing older.

The $2 million hypothetical retirement target won’t result from your earnings alone. It may also come from investment returns, compounding, and employer 401(k) match amounts over your working lifetime. There will be other sources, from Social Security to sales of assets you have accumulated throughout your life. Though $2 million seems like a daunting number, following the plan outlined here can lead to a pleasant surprise. It’s easy to attain your dream if you plan—and get started—NOW!