As previously discussed, when it’s time to buy an annuity, you have the choice between an immediate and deferred annuity.

If you prefer an immediate annuity, you’ll make a lump-sum payment. Within a year of the contract, the insurance company will begin issuing you a monthly income—which can either be for a specified number of years or for the rest of your life. And, the payment amount will be based on factors like your age.

For those who select a deferred annuity, you’re going to invest your money in a lump sum or a series of payments. But, you’re going to sit back watch it grow. Whatever earning you’ll make are tax-deferred.

Here’s where things might get a little more complicated. Regardless of what broad category you choose, both immediate and deferred annuities will be either fixed or variable. The main difference is that you’ll earn a predetermined interest rate on your money with a fixed annuity. The rate you’ll get is clearly spelled out in your annuity contract. It’s predictable and there’s less risk involved.

Variable Annuities Explained

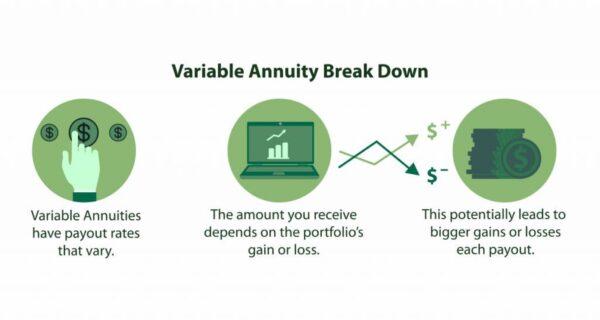

As with most annuities, a variable annuity is a contract between you and an insurance company. Specifically, it serves as an investment account that grows on a tax-deferred basis. The insurance aspect of a variable annuity comes in the forms of guaranteed payments that you’ve purchased with a single payment or a series of multiple payments.Unlike its annuity counterparts, you also personally select a wide range of investment options with a variable annuity. It’s through these sub-accounts that the value of your contract will vary. It could rise or fall depending on the performance of your investment options. Usually, your investment options are in the form of mutual funds that invest in stocks, bonds, and money market instruments. You may also be able to select a combination of these investments.

Since each variable annuity contains features that you can’t find in most other insurance products and investment options, they can truly be one-of-kind. Just note that you’ll most likely have to pay for the uniqueness of variable annuities.

The first defining feature of variable annuities is the insurance elements. An example of this will be if you pass away before you’ve begun to receive payments. If you’re named a beneficiary, then the insurance company will guarantee that they’ll at least receive a specified amount of your annuity. Additional insurance features include the promise that you’ll get you a certain account value and the ability to make withdrawals up to a certain amount annually.

Secondly, variable annuities are tax-deferred. As we’ve repeatedly stated, this means that you don’t have to pay federal taxes on the income and investment gains from your annuity. That is, until you make a withdrawal or receive income payments. This would also apply when a death benefit has been paid.

Sticking with taxes here, you can also transfer money from one investment option to another within a variable annuity. You don’t have to worry about paying federal taxes at the time of the transfer. But, you will once you withdraw your money. Just be aware that you are responsible for taxes on any gains at the ordinary federal income tax rates.

And, thirdly, with variable annuities, you’ll receive periodic income payments. Again, this can be for a specified period or the rest of your life. If married, you can set it up where they will receive payments for the rest of their life if you die before them. The process of converting your investment into a steady and recurring stream of income is known as annuitization. The highlight of this feature is that it protects against the possibility of you outliving your savings, which is a fear that many retirees have.

How Does a Variable Annuity Work?

When you purchase a variable annuity, don’t get discouraged or overwhelmed that you’ll have some investment options to fund your portfolio. Remember, these options or sub-accounts usually consist of stock mutual funds, bond mutual funds, and money market funds. You may even be able to select other investments like stable income value mutual funds.Accumulation Phase

It’s during this phase when your contract will increase in value. For this to take place, you’ll make a deposit or an initial contribution. This will purchase the annuity. From there, you can determine how you want to invest your money; You make an initial deposit or contribution to purchase the annuity. You can specify how you would like to invest your funds. However, be sure to review the disclosure document, aka prospectuses, for what your available options are.You may also have the option of investing in a fixed-interest account. With this variation of a variable annuity, you’ll still play the investment game while also receiving a guaranteed minimum interest rate.

Payout Phase

Also known as the distribution phase, this is when you can begin to receive your funds. You can also collect any gains you’ve made as well. This will either be as one lump-sum or as a recurring stream of variable payments. You can spell out in your contract how long you want the payments to last. Typically, you can settle on a period of years, let’s say for 10-years, or an indefinite period. With the latter, this would be the rest of your life or the lives of your beneficiaries.Variable Annuities: The Good, The Bad, and The Ugly

We would be remiss if we didn’t lay out the pros, cons, and downright terrible aspects of variable annuities.The Good:

- Potential growth that your money could earn. Without question, this is the most appealing feature of a variable annuity. In fact, compared to other annuities, this is the type that offers the best possible return.

- Tax deferral of investment gains. As with a traditional IRA, your account will grow on a tax-deferred basis.

- Ease of changing investments. Since you choose the mutual funds that make up your variable annuity, you have the ability to easily change the course of your investments. Often, this is at little or no cost.

- Income for life. As long as you annuitize your contract, the flow of income begins. When this occurs, the insurance company you’re working with guarantees payments for an agreed-upon period or the rest of your life.

- Asset protection. If you reside in Florida, New York, or Texas, annuities are protected from creditors and lawsuit plaintiffs.

The Bad:

- Little protection against premature death. Let’s say that you, at age 60 you receive a grand month since you have $264,000 into your annuity. Even if you break even and live past the age of 82, the insurance company must continue to make payments to you. But, what if you passed away younger than expected and there’s still a $264,000 balance? The insurance company will retain the balance. If you add beneficiaries, it’s either going to cost you an upfront fee or shrink your own payments.

- Tax penalties. Variable annuities are not exempt from this. You can not touch your money before age 59 ½. If you do, expect a 10 percent IRS tax penalty. Also, when you begin to receive payments, the income that’s considered an investment gain will be taxed at an ordinary-income tax rate instead of the long-term capital gains rate, which is usually lower.

The Ugly:

- Surrender charges. Having to shell out that 10 percent tax penalty is bad enough. But, it’s common practice for insurance companies to charge a surrender fee if you make an early withdrawal. So, let’s say that you have a $200,000 investment and you’re in the second year of the contract. If the surrender fee is seven percent, that will cost you $14,000! Just note that the longer your money is untouched, the lower this surrender fee will be. So, in year three, it might drop to six percent and so forth.

- Hefty sales commissions. Because annuities are commission-based products, expect the insurance agent who sold you the annuity to make a commission on the sale. Ask them how much they’ll be making.

- Fees galore. If you aren’t careful, you could get burned with annual and administrative fees. There could even be mortality and expense charges that will chip away at your earnings. On average, an annuity will charge around 2.3 percent to three percent on these charges every year. Also, the mutual funds in your sub-account charge fees.

Shopping for a Variable Annuity

Before committing, always do your homework when shopping for a variable annuity. And, the first place to start is weighing the advantages and disadvantages listed above.“But watch out for costly options that are ‘sophisticated and richer’ than what you are looking for,” she adds. “The fewer bells and whistles an annuity has, the less it should cost.”

And, most importantly, you want to work with the right annuity company. After all, these are are a complicated mix of insurance and investments. As such, they must be sold by insurance agents and not some random Amazon seller.

Can You Exchange One Credit For Another?

Let’s say that you would like to exchange an existing variable annuity contract for a shiny, new annuity contract. You know, one that has features more to your liking. If you’re still in the surrender period, you may have to pay surrender charges on your old annuity. Also, expect a new surrender period to begin when you exchange one credit for another.Bonus Credits Explained

Some insurance companies offer bonus credit features. This is simply a promise from the insurance company to add extra money to your contract value. The catch is that it’s based on a specified percentage. Generally, this is in the one percent to five percent range of purchase payments.So, if you purchase a $100,000 variable annuity and there’s a three percent bonus credit on each purchase payment, you’ll land an additional $3,000.

What’s a “Free Look” Period?

Most variable annuity contracts come with something called a “free look” period. Basically, it’s just a test run on the annuity to ensure that it’s a right fit with your retirement plan. Typically, this period is 10 days for you to cancel your contract before any fees are incurred. But, it could be more days for you to review your investments.