With inflation near a 40-year high, Social Security could get a historic boost next year to help seniors keep up. The most recent estimate for a 2023 cost of living adjustment (COLA) is 9.6 percent, says Mary Johnson, Social Security and Medicare policy analyst for senior advocacy group the Senior Citizens League (SCL).

July’s Consumer Price Index (CPI) report showed inflation up 8.5 percent over the last 12 months, making it more difficult for people living on fixed incomes, like those from Social Security benefits, to make ends meet.

The 2023 COLA will be based on third-quarter data from the Consumer Price Index for Urban Wage Earners and Clerical Workers, or CPI-W. Johnson says the announcement is expected around Oct. 13, after the release of the September CPI report. If inflation “runs hot” or higher than average, Johnson predicts the COLA could run up to 10.1 percent for 2023. Should it run lower than the recent figures, she says 9.3 percent might be more likely.

An adjustment of 9.6 percent would increase the average monthly Social Security retirement benefit of $1,656 by $158.98, says Johnson.

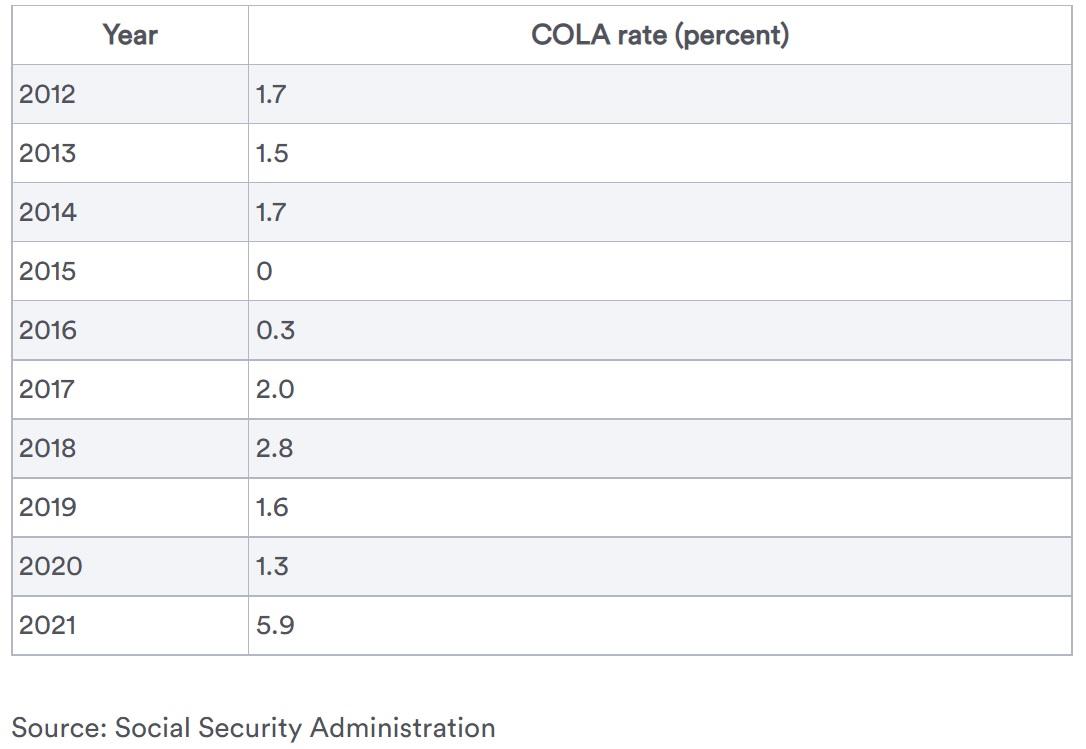

The prior COLA came in at 5.9 percent, and 9.6 percent this year would be enormous in terms of COLA rates in the recent past. The table below shows the past 10 years of rate increases. As you can see, even the jump in 2021 to 5.9 percent was well above the 0-2.8 percent range over the last decade.

COLA May Not Be Enough

The CPI-W is the benchmark upon which monthly Social Security benefits increases are determined, but the Senior Citizens League has long advocated that the index is not representative of the way seniors live.One often-cited gripe with the CPI-W is the weight it gives to things like gasoline—something urban wage and clerical workers might need to commute to work every day more so than retired seniors. The SCL says this figure underestimates the inflation experienced by Social Security recipients, since it does not give enough weight to expenses senior citizens have, such as healthcare or housing.

COLA Is a Double-Edged Sword for Low-Income Workers

Those who receive low-income assistance might be affected by higher COLA increases. Higher benefit amounts next year might hurt the eligibility of low-income assistance recipients to obtain that assistance.According to SCL’s new Seniors Priority Survey, 37 percent of participants reported they received low-income assistance in 2021.

In 2022, roughly 14 percent of survey participants said their low-income assistance was actually reduced as a result of their increased Social Security benefit, and another 6 percent lost access altogether to at least one other program. Low-income assistance programs require recipients to stay under a certain income level to qualify for benefits. Last year’s COLA increase of 5.9 percent was one of the largest in history and pushed many over the edge of eligibility.