The “sandwich generation” absorbs special financial pressure from two directions at once: aging parents who may need care and adult children who cannot yet afford to live independently.

A recent report found that over 25 million young adults (under 34) were living with their parents last year. Many American parents are absorbing that cost informally. What may start as temporary help can quietly erode the retirement compounding window that matters most.

Quick Answer: What Tax Benefits Do I Get for Supporting an Adult Child at Home?

Supporting an adult child at home may qualify them as a tax dependent under the IRS Qualifying Relative rules, unlocking benefits including the Credit for Other Dependents and Head of Household filing status. The age-26 health insurance cutoff creates a time-sensitive planning deadline. And the financial cost of open-ended support during your highest-earning decade carries a compounding cost that is difficult to recover. Structure matters on both the tax side and the retirement side.The IRS Qualifying Relative Test

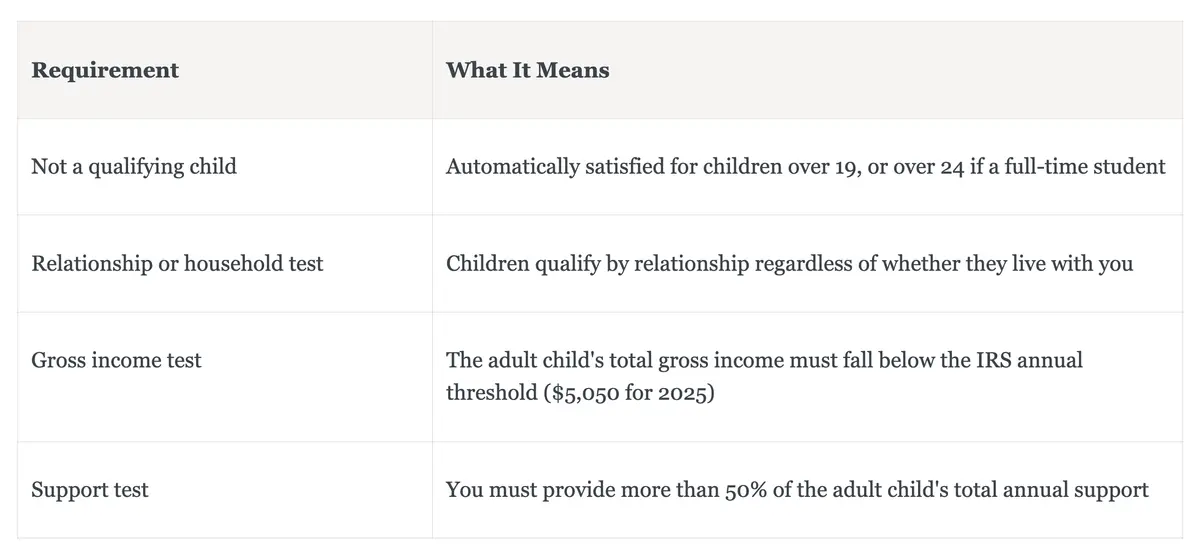

An adult child who moves back home may qualify as your tax dependent under the IRS Qualifying Relative test. To start, all four of these conditions must be met:

The gross income limit is the most common point of failure. If your adult child earns wages, freelance income, or investment returns above the threshold, the dependency claim fails regardless of how much financial support you provide.

What Qualifying Dependent Status Still Gets You

Personal exemption deductions were suspended by the Tax Cuts and Jobs Act, so claiming a dependent no longer reduces your taxable income directly. However, dependency status still provides meaningful benefits:- Credit for Other Dependents: A $500 nonrefundable tax credit for adult dependents who do not qualify for the Child Tax Credit. This phases out above $200,000 AGI for single filers and $400,000 for married filing jointly.

- Head of Household filing status: Single parents supporting a qualifying dependent may file as Head of Household, which provides a larger standard deduction than Single status.

- Medical expense deduction: Medical costs you pay on behalf of a qualifying dependent may be included in your Schedule A deduction, to the extent total qualifying expenses exceed 7.5 percent of adjusted gross income.

The Age-26 Health Insurance Cliff

Under the Affordable Care Act, children may remain on a parent’s health plan until age 26, regardless of whether they live at home, are married, or have access to employer coverage. This applies to both employer-sponsored and marketplace plans.The age-26 cutoff is a hard deadline. After the policy year in which your child turns 26, they must obtain separate coverage. Plan for this transition before it arrives, not the month it happens.

Below-Market Rent and the Household Charter

Two tools that most families skip are worth using together: below-market rent and a household charter.Charging even modest rent keeps your adult child in the habit of allocating income to housing before discretionary spending, and it reduces your net share of their total support for the IRS support test calculation.

When rent is set below fair market value, the IRS generally treats the room or property as used for personal purposes; rental losses are not deductible, but if the amount is reasonable and primarily for family support rather than profit, the arrangement typically does not generate significant reportable rental income.

- Monthly financial contribution, whether rent, utilities, or shared grocery costs

- A savings milestone or target before the arrangement is revisited

- A defined exit date or a scheduled review

- Shared household responsibilities and expectations

The Retirement Math You Cannot Ignore

For most sandwich generation parents, the decade between 50 and 60 is the most productive remaining window for retirement compounding. Diverting money from retirement contributions toward open-ended adult child support during this period carries a cost that compounds—in reverse.Investors who are 50 and older can contribute an additional $7,500 annually in 401(k) catch-up contributions above the standard limit. Redirecting even part of that capacity toward adult child support means foregoing not just the dollars contributed but all future earnings on those dollars across the remaining working years.