What they rarely include is a clear fee schedule, an honest explanation of Internal Revenue Service compliance requirements, or a comparison to lower-cost alternatives for investing in gold. Before you roll over retirement savings into physical gold, here is what the structure actually involves.

Quick Answer: What Are the Main Risks of a Self-Directed Gold IRA?

A self-directed gold IRA is a legitimate account structure, but it carries ongoing fee drag, limited liquidity, and strict IRS compliance requirements that standard IRAs do not. Buying ineligible metals, taking personal possession, or violating custodial rules can trigger a fully taxable distribution with penalties attached. Gold exchange-traded funds (ETFs) held in a standard IRA provide comparable price exposure at a fraction of the cost and without the compliance burden.

How the Structure Works

A self-directed IRA permits alternative assets, including:

Physical precious metals

Real estate

Private equity holdings

However—and this is important—you cannot hold the metal yourself.

All gold must be held by an IRS-approved custodian and stored at an IRS-approved depository, such as the Delaware Depository or Brinks Global Services. The custodian administers the account; the depository stores and insures the metal.

Both charge ongoing fees that a standard brokerage IRA does not require.

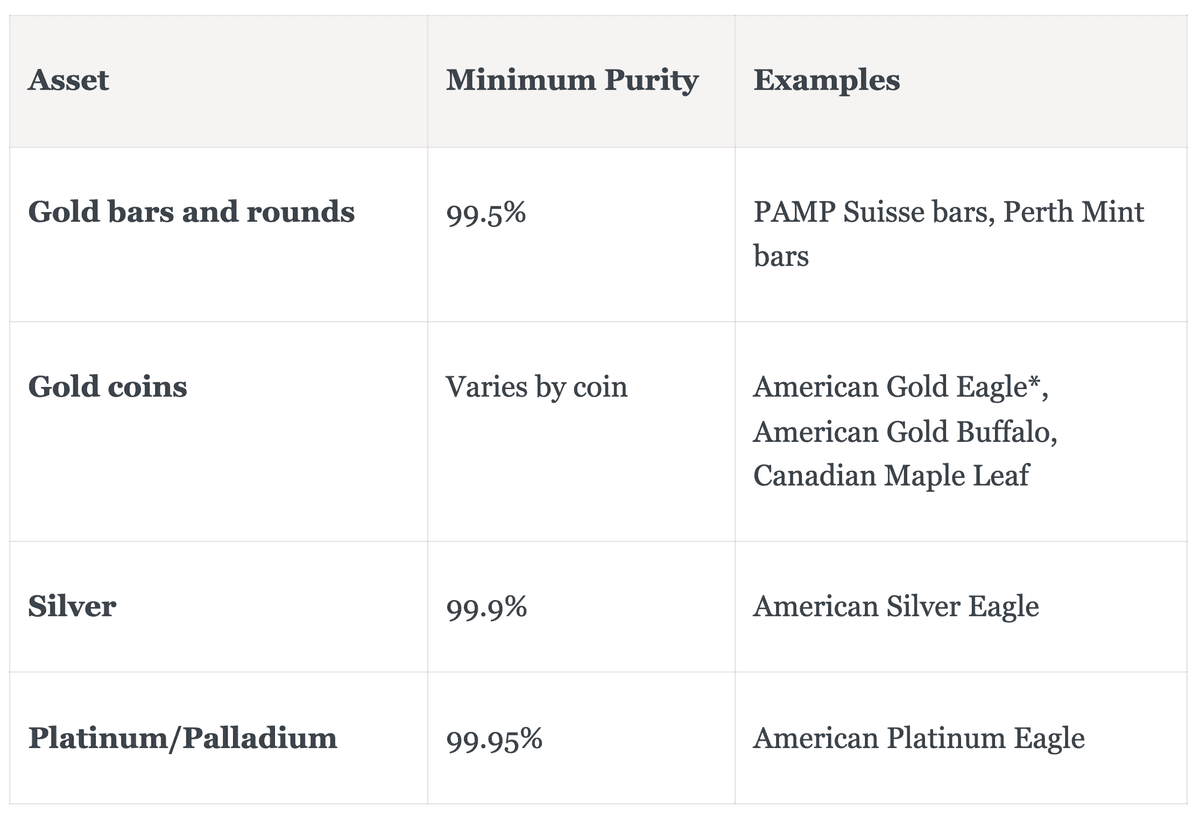

What Gold the IRS Will and Will Not Accept

Under Internal Revenue Code (IRC) Section 408(m), metals held in an IRA must meet minimum purity standards. Purchasing non-qualifying metal inside an IRA triggers immediate distribution treatment at the full purchase price.

Numismatic and collectible coins do not qualify regardless of their gold content. Dealers who fail to distinguish between investment-grade bullion and collector products are among the most common sources of IRA compliance failures.

3 Compliance Violations With Severe Consequences

Personal possession: Taking physical custody of the metal at any time, even temporarily, constitutes constructive receipt. The IRS treats the full fair market value as a taxable distribution in the year it occurs. Investors under 59 1/2 also owe a 10 percent early withdrawal penalty.

Home storage IRAs: Some dealers promote arrangements allowing investors to store IRA gold at their residence. The IRS does not recognize this as compliant custody. Following this advice can trigger full IRA disqualification, making all assets immediately taxable.

Prohibited transactions: Purchasing metal from a family-owned dealer or using IRA gold as personal loan collateral violates IRC Section 4975 and can disqualify the entire account for the year the transaction occurred.

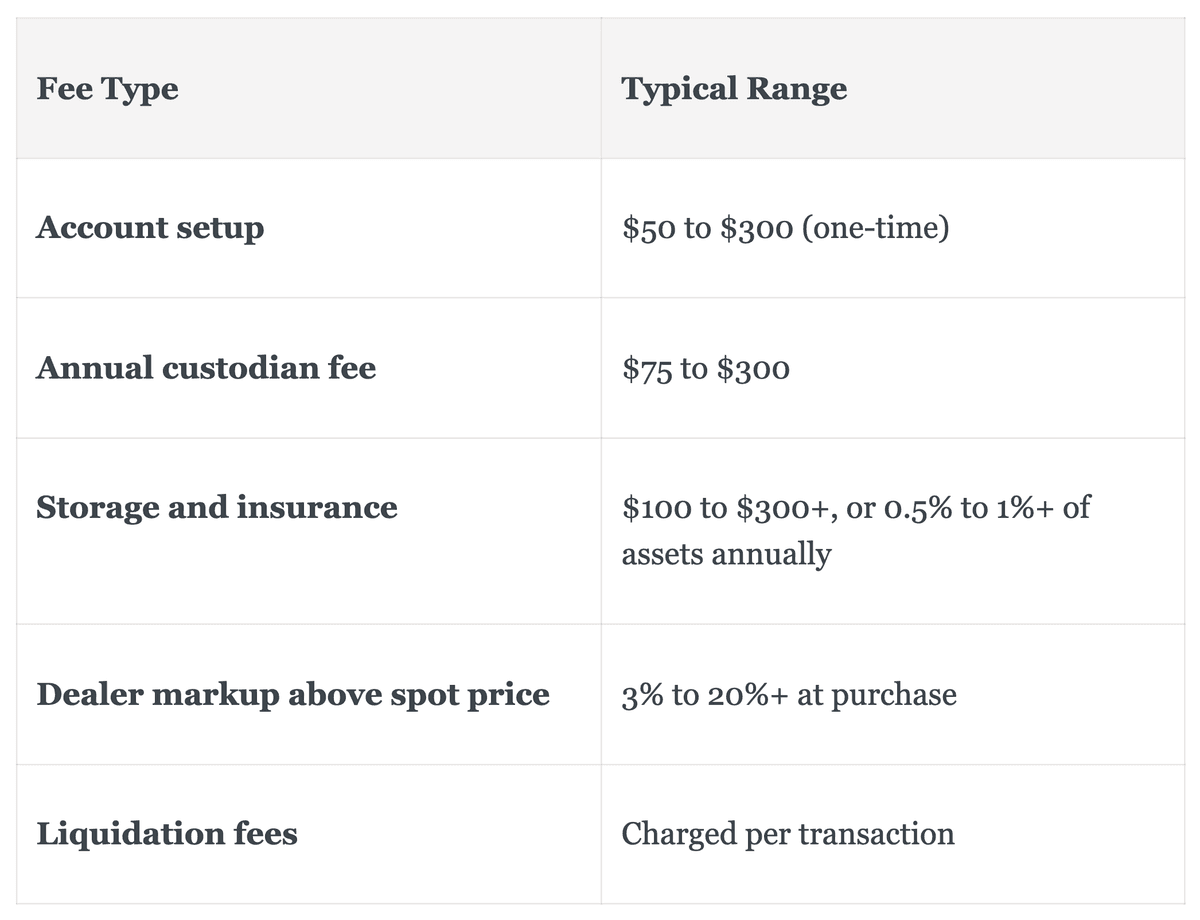

The Real Cost: Fee Drag and a Lower-Cost Alternative

A physical gold IRA layers costs that a standard IRA does not carry:

On a $100,000 account, annual costs can reach $1,000 to $1,500. Gold ETFs such as GLD (0.40 percent expense ratio), IAU (0.25 percent), and GLDM (0.10 percent) provide equivalent gold price exposure with no storage fees, no specialized custodian requirement, and no dealer markup.

Tax treatment inside an IRA is identical in both structures.

Required Minimum Distribution Problem

Traditional IRA holders must begin taking required minimum distributions (RMD) at age 73. In a standard IRA, this is a straightforward cash withdrawal.

In a physical gold IRA, satisfying an RMD requires either selling gold at whatever the market price happens to be on that deadline or taking an in-kind distribution of metal that must be independently appraised and is taxable at its full fair market value.

Pairing an illiquid asset with mandatory annual distribution deadlines creates structural risk that most gold IRA sales presentations never mention.

Audit Checklist for Existing Accounts

If you or an aging parent holds a physical gold IRA, review the account against these criteria:

Annual statement itemizes storage, custodian, and insurance costs as separate line items

Custodian is IRS-approved; the depository is a named, established facility

Metal on account is bullion-grade, not numismatic or collectible

No documentation references home storage or checkbook control arrangements

Dealer markup above spot price was disclosed before purchase

The account has a documented plan for satisfying annual RMD obligations

Any item you cannot confirm is reason to consult a fee-only financial adviser or CPA before adding further contributions.

FAQs About Self-Directed Gold IRAs

What Happens if I Accidentally Buy Non-Qualifying Gold for My IRA?

Purchasing metal that does not meet IRS purity standards, including collectible or numismatic coins, is treated as buying a collectible inside the account. The full purchase price is classified as a taxable distribution in the year of purchase. You owe income tax on that amount, and if you are under 59 1/2, the 10 percent early withdrawal penalty also applies. The metal does not leave the account, but under IRS rules it is taxed as though it did.

Is There Ever a Good Reason to Choose a Physical Gold IRA Over a Gold ETF?

How Can an Adult Child Review a Parent’s Gold IRA Without Full Account Access?

Start with the account statements. Look for custodian names that are not major financial institutions, separate line items for storage and insurance, references to a private depository, and a large portfolio concentration in a single alternative asset. Request a complete fee disclosure document directly from the custodian. If fees are not clearly itemized or the custodian is unresponsive, that itself is a significant red flag. A CPA or fee-only adviser can conduct a formal review with limited documentation in hand.