Business email compromise (BEC) is a targeted fraud scheme in which criminals impersonate vendors, executives, or accountants to steal money from businesses. AI has made these attacks dramatically harder to detect by generating personalized emails that mirror real writing styles and existing business relationships.

What Is Business Email Compromise?

A BEC is not your typical phishing email. There is often no suspicious link, no misspelled bank name, and no “lottery prize.”The Core BEC Scheme

A criminal impersonates a trusted contact, such as a vendor, your accountant, or your own CEO, and requests a wire transfer, an invoice payment, or a change to banking details.Why AI Has Made This Significantly Worse

For years, spotting a BEC email meant looking for bad grammar, awkward phrasing, or a sender name that did not quite match the domain. That approach no longer works.- Scrape LinkedIn profiles, websites, and public business filings to map your vendor relationships and internal structure.

- Analyze writing samples to clone the tone and style of a specific person.

- Generate emails that reference real projects, real invoice numbers, and real business history.

- Produce flawless English with none of the telltale errors that once flagged these attempts.

What a Typical Attack Looks Like

These two scenarios play out regularly against small businesses and freelancers:Scenario 1: The Fake Vendor Invoice

You receive an email from what appears to be a vendor you have worked with for two years.

The address looks right at a glance. The email references your last project together and includes an updated invoice with new banking details. The tone matches the vendor’s usual communication style.

Scenario 2: The Executive Wire Request

You get an email from your company’s owner or a senior partner.A deal is closing today, and a wire transfer needs to go out immediately. The request emphasizes urgency and discretion. The writing style matches. The amount fits your normal range. You send it.

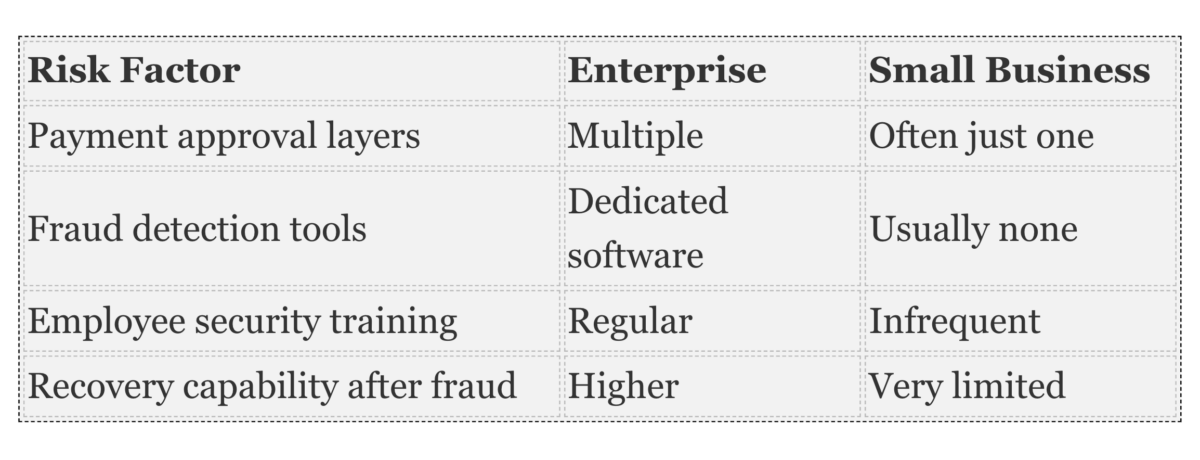

Why Small Businesses Are Targeted More Than Large Companies

Large enterprises typically have layered payment approval systems, dedicated fraud detection software, and internal cybersecurity teams. Small and mid-sized businesses generally do not.A single employee may have full authority to execute a wire transfer without a second sign-off. Criminals know this and exploit it systematically.

Five Verification Steps That Cost Nothing

You do not need specialized software or a cybersecurity team to reduce your BEC exposure. You need consistent habits.- “Call to confirm” protocol. Any request involving a payment, wire transfer, or change to banking details should be verified by phone, using a number already in your records, not one provided in the email in question.

- Create a payment change policy. Set a firm rule: vendor or employee banking information is never updated based on an email alone. Require a written request plus a live phone confirmation.

- Treat urgency as a red flag. Urgency is a deliberate manipulation tactic in BEC attacks. If an email is pressuring you to skip normal approval steps, slow down regardless of how legitimate it looks.

- Check the actual sending domain. The display name may read “Sarah at Metro Supplies” while the actual address is [email protected] rather than [email protected]. Lookalike domains are a standard BEC tool.

- Require dual authorization for wire transfers. Even in a two-person operation, require a second approval on any outgoing wire above a defined threshold.

If Your Business Has Already Been Hit

If your business has already been hit, act immediately. Contact your bank and request a wire recall. File a complaint with the FBI’s Internet Crime Complaint Center at ic3.gov. If the loss is significant, contact your local FBI field office directly.Also, review your insurance coverage. Standard commercial general liability policies typically do not cover funds transfer fraud. A cyber liability policy or crime insurance endorsement may provide protection.