You’re comparing two financial advisers. One says he’s a fiduciary. The other says he always acts in your best interest. They sound identical. They are not.

Quick Answer: What Is a Fiduciary and Why Does It Matter?

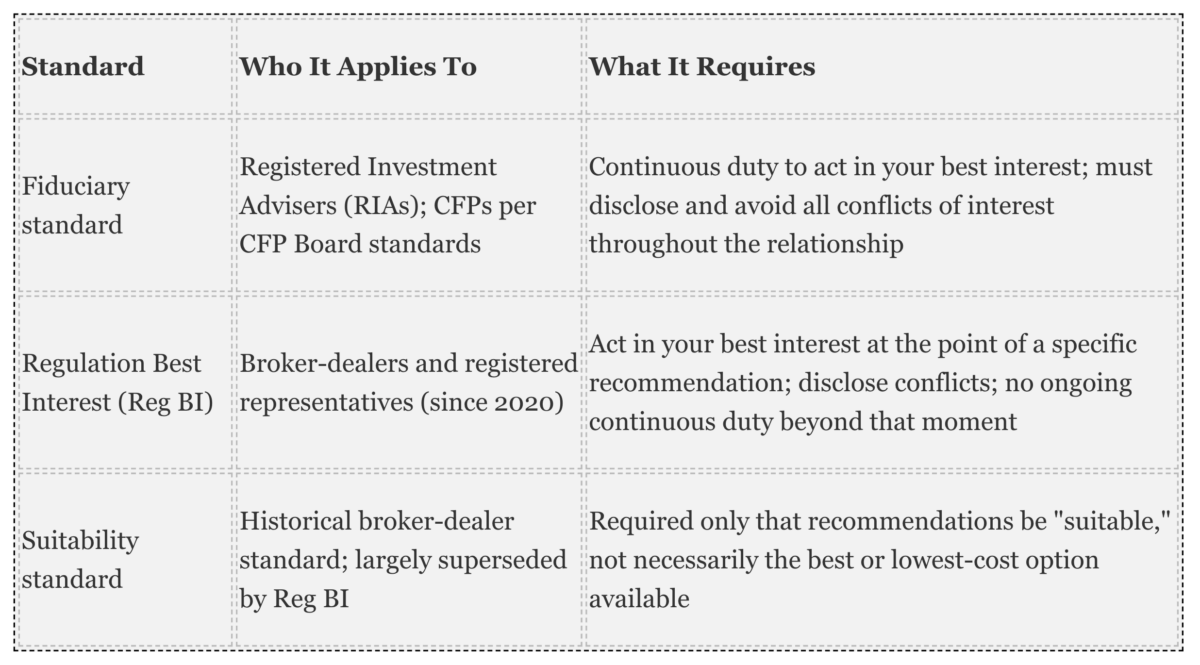

A fiduciary is legally required to act in your best interest on a continuous basis, not only at the moment of a specific recommendation. In financial advising, this means disclosing all conflicts of interest, managing your assets with professional care, and placing your financial well-being ahead of their compensation. Not all advisers are fiduciaries, and the difference can affect what they recommend, what it costs you, and what legal recourse you have if something goes wrong.The 4 Core Fiduciary Duties

A fiduciary carries four legally recognized obligations:- Act solely in your best interest, not their own

- Manage your assets with professional care and diligence

- Keep your assets completely separate from their own

- Maintain accurate and complete records of all decisions and transactions

The 3 Standards of Care

Three distinct standards govern financial advisers in the United States today:

The Difference That Matters Most

The critical distinction between Reg BI and the fiduciary standard is timing.Under Reg BI, a broker-dealer’s obligation applies at the moment of making a specific recommendation and does not extend beyond it. Under the fiduciary standard, the duty is continuous throughout your entire advisory relationship.

Who Is and Isn’t a Fiduciary

Typically fiduciaries:- Registered Investment Advisers (RIAs) registered with the SEC or your state securities regulator

- Certified Financial Planners (CFPs) when providing financial planning advice, per CFP Board standards

- Trustees, estate executors, legal guardians, and conservators

- 401(k) plan administrators

- Broker-dealers and registered representatives, governed by Reg BI

- Commission-based insurance agents

- Dually registered advisers, who may operate under different standards depending on the service

What to Ask Before You Hire

One of the most useful questions you can ask a prospective adviser is a direct: “Are you a fiduciary 100 percent of the time, for every service you provide to me?”

- Vague reassurances like “I always act in your best interest” without legal specificity

- Inability or unwillingness to give a direct yes or no

- Confirmation of dual registration without a clear explanation of when each standard applies

- Reluctance to put their fiduciary commitment in writing

How to Verify Fiduciary Status

Don’t rely on the adviser’s word alone. These official tools let you confirm:- adviserinfo.sec.gov: The SEC’s Investment Adviser Public Disclosure database; search by name for registration status, Form ADV, compensation structure, and disciplinary history

- brokercheck.finra.org: FINRA BrokerCheck; covers broker-dealers and registered representatives

- cfp.net/verify: The CFP Board’s certification and standing verification tool

- napfa.org: Member directory of the National Association of Personal Financial Advisors, the leading professional organization for fee-only fiduciary advisers

The Cost Question

Fiduciary advisers typically charge assets under management (AUM) fees of 0.5 percent to 1.5 percent of your portfolio annually, or flat fees for defined planning work.Commission-based advisers may appear free upfront, but their compensation comes from the products they sell you, often those carrying higher expense ratios, front-end loads, or 12b-1 distribution fees that quietly reduce your returns every year.

A fiduciary who recommends a low-cost index fund over a high-fee actively managed fund is saving you a meaningful percentage of your portfolio value on every dollar invested, compounded over time. In practice, the transparent advisory fee is frequently the less expensive choice, not the more expensive one.