Special-Needs Trusts

Medical coverage is often more important to a beneficiary than a monetary inheritance. Lots of people rely upon Medicaid or other need-based programs to pay for their chronic medical expenses. If they should inherit an unrestricted amount of money, they could be disqualified from receiving their benefits until the money has been exhausted. So, they receive no actual benefit from the inheritance, it being required to be used for their medical care. Probate court conservatorships cannot help in this situation.

A trust can include provisions that the share of that person is to be held in a discretionary trust, which gives the beneficiary no right to these assets without the permission of the trustee, and at the death of the beneficiary any remaining assets would go to one or more other named beneficiaries, the so-called remaindermen. The trustee could use some of the money—less than what would disqualify the beneficiary from the program—for the benefit of the beneficiary but would not be required to do so. Paying for a vacation at a theme park, for example, or buying toys, games, and clothing would likely not disqualify the beneficiary. This type of discretionary Medicaid trust takes careful drafting by an experienced trust attorney, since the law changes often in these areas and varies from state to state. It is a personal decision to do it this way, since some would think it a way of taking unfair advantage of the Medicaid program. (I have never had anyone say no to this suggested approach.)

Joint or Single Trusts

Trusts can be joint or individual. Married couples typically opt for joint trusts, although they can have individual ones if they choose. Couples who are in second marriages, where each brought assets into the marriage and might have children from prior relationships, often have a desire to use the assets of the first to die to benefit the survivor, with the residue going to that person’s separate children at both their deaths. The trust of the first to die usually becomes irrevocable at that time. As we know, that means it cannot be changed. The trust has to be carefully written to protect the survivor as well as the children. The surviving spouse is normally not a sole trustee.

Even in relatively modest family estates, an irrevocable survivor’s trust is sometimes used. It often happens that one of the parties already had a house into which the new spouse moved. The house-owning spouse will give the survivor the irrevocable right to live in the house as a primary residence for life, with the house going to the children at both deaths. Be sure, though, that if this type of trust is created it also protects the survivor’s right to the use of the household furnishings and possibly automobile. I had a case where the children of the deceased parent actually removed all the furniture, right down to the kitchen dishes and silverware, even though they could not get possession of the house itself. People can be real jerks when a stepparent dies, and it often comes as a tragic surprise to the survivor. A trust can be written to provide for the individual wants and needs of nearly any family situation.

A grantor does not have to be married to create a joint trust. I have prepared joint trusts for a parent and child and many for unmarried couples.

As you can see, the flexibility of revocable trusts, both joint and single, allows you to accomplish your testamentary goals while avoiding the high cost and time consumption of the probate process. The vast range of trust types and provisions is why, in my opinion, preprinted or online trust forms are not suitable for most people and can lead to unintended outcomes if not carefully drafted.

Discretionary Trusts

Irrevocable trusts are often used in gifting situations. You can set aside money to be held in trust for someone, to be distributed according to your instructions and under the control and management of a trustee other than yourself. This might be a trust for grandchildren, which you can add to from time to time with the parents as trustees. It could be used for educational expenses or distributed in installments as you direct. Or it could be a total discretionary trust where the trustees have total say-so as to when, if, and what amount should be used for the beneficiaries. If the beneficiary dies or disclaims the trust funds, you would direct who would get the remaining funds in the trust. These irrevocable trusts would remove the funds from your probatable and taxable estate. You can also set up trusts to care for pets or for charitable purposes.

Asset Protection Trusts

I mention these because they get a lot of press, though not just for probate avoidance. The asset protection trust pitch is that you can create a trust, usually with a legal home base in another country, put your assets in it, and even open bank accounts with debit cards in the trust name. If you are sued or subject to high tax rates where you actually live, the trusts protect you from having your funds taken by creditors, bankruptcy, lawsuits, and divorce judgments. While most of these are legal plans, they have significant downsides and can be pricey.

The basic idea is to create an irrevocable discretionary trust with someone besides yourself as the trustee. You can only get at your trust funds if the trustee agrees, and only under limited circumstances. If you can’t get them, neither can anyone else. Typically, the plans also include creating a limited liability company (LLC) to manage the assets and to hold title to some of them to hide the actual ownership. You own the LLC, which sets up the trust, and you decide who becomes the trustee. It is a rich person’s way of hiding money and can be used for money laundering.

Problems can arise and often do if you try to create this kind of trust after the trouble you are trying to avoid has already begun. There are criminal laws that apply if it can be shown that you fraudulently divested yourself of assets in order to avoid creditors. These are usually called fraudulent conveyance statutes. Similarly, a divorce or bankruptcy court may be able to set aside any such transfer if it was made too closely in time to the bankruptcy or divorce.

Complex Tax-Saving Trusts

What if your trust was set up years ago, based on tax laws at that time, and was intended to avoid estate taxes? Because of the changes in estate tax laws discussed earlier, it is unlikely that you would ever have to be concerned about taxation. The existing trust, which is likely filled with complicated formulas for splitting the trust at the death of one partner, creating a marital trust and a bypass trust, can now be simplified. This will eliminate accounting and attorney fees at the death of one and again at the death of the other to settle the complex trust. While this type of trust was appropriate and necessary when the tax threshold was low, it is likely not needed any longer.

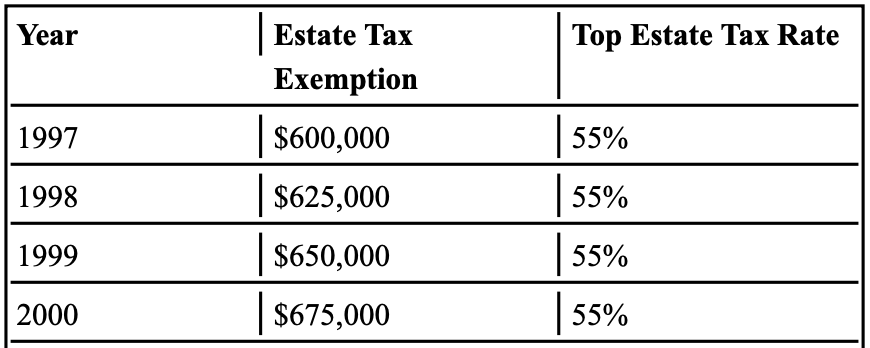

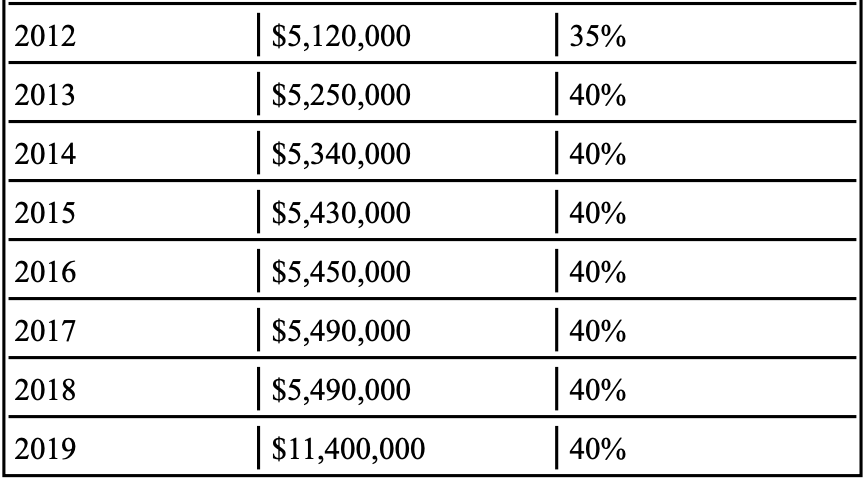

For much of the last thirty years, the estate tax threshold has been increasing so that fewer estates are now taxable. The threshold is the amount your estate can have in it without being taxed by the IRS. The taxable estate is not the same as the probate estate. All assets, including those in trusts and those like life insurance that pass by beneficiary designation, are counted as taxable assets for estate tax purposes. By the time you add up the values of insurance, retirement and investment accounts, real estate, personal property, intangibles, and other assets, many people—not just the rich—were subject to estate taxes. And the tax rates were high—up to 45 percent of the amount over the threshold. Having trusts could easily double the amount of exemption for a married couple, so we made a lot of tax- saving trusts back then.

One of insurance agents’ favorite plans to push used to be irrevocable life insurance trusts, set up to create a fund to pay the massive estate taxes. This cost the client money for both the trust and the life insurance, but presumably saved money in the long run. If you have one of these and are substantially below the exemption amount, you probably don’t need either the trust or the insurance policy any longer. Ask your lawyer. It could be appropriate to defund the existing trust and replace it with a simpler and easier-to- understand version.

A simple trust, such as the example in Appendix E, is pretty easy to understand, but in fact I can make a perfectly legal trust in just two or three pages for simple estate plans. More pages do not make a better trust. I have seen trusts running upwards of a hundred pages for seemingly ordinary family situations. They are mostly boilerplate. To repeat my warnings: whatever you do, be sure to run it past your lawyer before you commit to anything, and always get a second unbiased opinion.

Here’s a chart illustrating the changes in the estate tax exemptions. Keep in mind it is likely to continue to change in the future. It may even decrease. The tax rate applies only to the amount in excess of the estate tax exemption amount.

(To be continued...)

This excerpt is taken from “How to Avoid Probate for Everyone: Protecting Your Estate for Your Loved Ones” by Ronald Farrington Sharp. To read other articles of this book, click here. To buy this book, click here.

The Epoch Times copyright © 2023. The views and opinions expressed are those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.