Social Security benefits were designed to supplement our income needs in retirement by providing about 40 percent of what a retiree might need for a comfortable life based upon pre-retirement income.

Beyond Social Security, financial planners suggest we plan to depend upon 80 percent of what we were earning in the years leading up to retirement, on average. This retirement savings piece will be the 60 percent that, along with the 40 percent from Social Security, will get you where you want to be financially when you retire and enjoy perhaps the best part of life.

A stressful retirement awaits those who do not properly prepare, those who receive only or mainly social security benefits, and those who must rely on their children to take care of them.

By the time you retire, if you haven’t adequately planned and prepared, you can’t do much about it, as many folks well into their seventies are finding out, and are having to find work to supplement their retirement expense needs.

So, take heed. Plan. Save. You can arrive at the most joyful part of your life when you no longer work for a living and can enjoy the flexibility of doing the things you want to do, going where you want to go, and not having to worry about financial stability.

Saving in a Tax-Deferred Retirement Account

Let’s look at the different ways you can accumulate an adequate nest egg, that is, a retirement savings account. There are several popular options and others that are lesser known but customized to fit specific circumstances and unique working situations, skills, and ways to generate retirement income. First up we discuss the 401(k).401(k) Retirement Savings Plan

If you work for a company that offers a 401(k)-retirement savings plan, by all means participate. Today you can sock away as much as $20,500 per year, and if you’re over 50 you can save an additional $6,500 more.A rule of thumb is about 20 to 25 percent of your income should be saved throughout your working lifetime. The amount is deducted from your paycheck and not taxed. You pay income taxes only when funds are withdrawn from your retirement account, and by then you are likely only going to need to withdraw an amount for living expenses, and therefore the tax bracket will be lower than the tax bracket during your working career.

Many companies will match your 401(k) deductions up to a certain amount. The average match is 4.6 percent, and it is a good idea to take full advantage of every dollar of match your company offers.

Your company will select a 401(k) provider, for example T Rowe Price. That provider will build a list of fund options for you to choose from, ranging from conservative to aggressive funds. The conservative choices won’t provide high returns, but they will provide greater safety to retain the principle amount you put into the fund.

The aggressive funds will experience volatility, meaning their value can go up or down a lot, but over time they offer the possibility of a much higher overall return on your investment.

When you’re young and just getting started, choosing a heavier weighting of aggressive fund choices makes sense since you have a long runway called “time” to smooth out the ups and downs and enjoy long-term higher returns. As you are nearing retirement, however, you will be inclined to lock down your principle amounts and the gains you have made. This can be done by shifting into the more conservative fund choices offered.

Let’s take a hypothetical example to illustrate. Jill works in Accounts Receivable at Feckless Frisbee company, and earns $52,000 per year. She pays 22 percent in federal income taxes and gets paid on a weekly basis. Jill has elected to contribute 10 percent of her salary to her company 401(k), or $100 each paycheck.

Since the deduction is pre-tax based, Jill sees only a reduction of $78 from her weekly paycheck. If she neglected the 401(k) deduction, Jill would take home $780 after tax withholding. With the 401(k) deduction Jill takes home $702 and $100 goes into her new 401(k) and begins to compound.

Individual Retirement Account

For those who are self-employed, perhaps running your own business, or your employer doesn’t offer a 401(k) plan, you still can contribute to a tax-deferred individual retirement account (IRA). The annual maximum contribution for tax years 2021 and 2022 was $6,000. If you are age 50 or over, you can add an additional $1,000 a year, called a “catch-up contribution.”Roth IRA

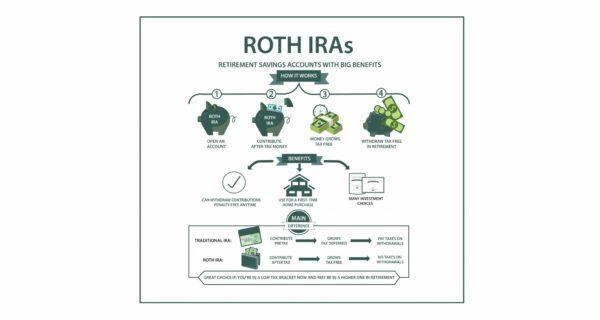

The main difference between a Roth IRA and a Traditional IRA, or a 401(k), is when you pay the taxes. You contribute to a Roth with after-tax dollars. The beauty is that when you make withdrawals from your Roth, you have no tax liability. Zero. With the Traditional IRA and 401(k) you must pay income taxes on your retirement withdrawals.

Bottom Line

It is easy to put the need for a retirement account out of your mind when you’re younger. You think you have plenty of time, your career is just getting started, and your salary barely covers what you need to live on, and you may have some hefty student loan payments.But the simple reality is that the earlier you start, the easier and more affordable your retirement goal becomes. You develop savings habits early on, and almost unconsciously adjust your standard of living for the shortfall in salary. You will find you really can live without a portion of your income if you make just a few minor adjustments to your spending habits and tweak your budget to make saving as a priority.