Like 401(k) plans, IRAs can come in a range of different flavors. Savers have different ways to prepare for their futures based on the levels of their income and their tax liability.

- Traditional IRA

- Roth IRA

- SEP IRA

The Traditional IRA

The traditional IRA is the plan you’re likely to be most familiar with. It works like a traditional 401(k) but with lower contribution limits, with deductions that can phase out as your income rises, and with a free choice of retirement funds.The Roth IRA

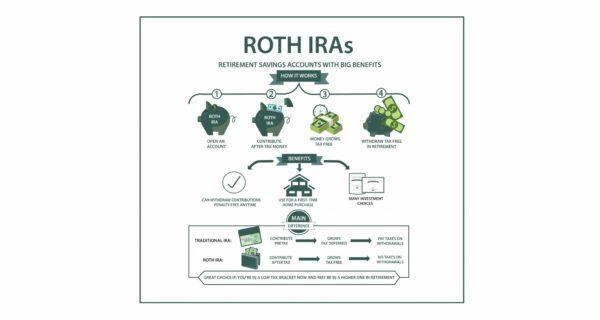

Just as 401(k) plans have Roth 401(k) plans, so IRAs also have their own Roth versions. For IRAs though they come with some special provisions.Like Roth 401(k) plans, savers make their contributions with after-tax dollars. They’ll pay tax on their income, then put money into their Roth IRA. Those funds continue to grow and the distributions are tax-free.

In general, Roth plans are useful for people who expect to have a higher income after they retire than when they make their contributions.

Roth IRAs also keep the IRA contribution limit. Whether you use a Roth IRA or a traditional IRA, you won’t be able to put more than $6,000 a year into your IRA, or $7,000 if you’re aged over 50.

But there are some additional conditions. First, Roth IRAs aren’t available to high earners. If you make more than $140,000 a year, or $208,000 for a couple, you can’t contribute to a Roth IRA.

On the other hand, once you’ve put money into your Roth IRA you can keep it there. While traditional 401(k) plans and IRAs require savers to start taking distributions at the age of 72, so that the tax authorities can get their share, your Roth IRA can remain untapped for as long as you want.

It is important to note though that you can only contribute earned income to a Roth IRA. You can’t use it to hold rental income, capital gains or stock dividends, interest from loans, or the proceeds from another retirement fund. It has to be money that you’ve made through work.

The SEP IRA

The big limitation of a 401(k) is that it can be complex and expensive. Companies don’t have to offer them and while a company that doesn’t provide a 401(k) plan will look less attractive to potential employees, some small companies just can’t afford them.The big limitation of an IRA is its low contribution limits. There’s a good chance that you’ll want to contribute more to your retirement fund than the $6,000 or $7,000 that the fund allows.

A Simplified Employee Pension, or SEP, IRA solves both those problems. It takes some elements of a 401(k) and some elements of an IRA. The result is a retirement fund that’s delivered through employers, gives employees some degree of control over the investments, and has relatively high contribution limits.

The Epoch Times Copyright © 2022 The views and opinions expressed are only those of the authors. They are meant for general informational purposes only and should not be construed or interpreted as a recommendation or solicitation. The Epoch Times does not provide investment, tax, legal, financial planning, estate planning, or any other personal finance advice. The Epoch Times holds no liability for the accuracy or timeliness of the information provided.