While peering through an imaginary crystal ball, real estate industry leaders are forecasting cloudy skies for the residential market of early 2023. At a recent webinar hosted by the Hudson Gateway Association of Realtors in the New York metropolitan area, a National Association of Realtors (NAR) economist, along with panel of expert brokers, weighed in on the state of the market for the next six months.

Nadia Evangelou, NAR senior economist and director of forecasting, said inflation is one of the main triggers of what’s happening in the housing market. “In August, for example, inflation rose much faster than expected, hitting 8.3 percent,” she noted. “Combined with the higher mortgage rates, the accelerating costs of gas, groceries, and other goods are now forcing some people out of the market.”

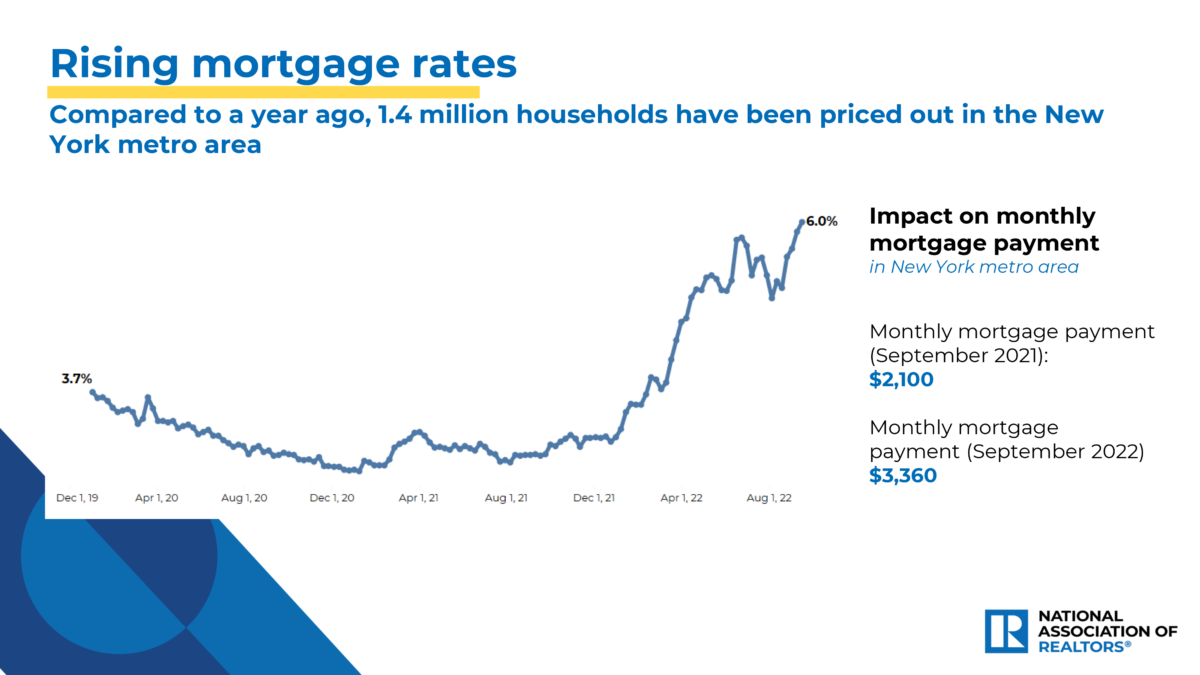

Using the New York metro housing market as an example, Evangelou reported the average monthly mortgage payment in September 2021 was $2,100, compared to the September 2022 average payment of $3,360 per month. “That’s close to an extra $1,300 more each month,” she said. “Mortgage rates are significantly higher than in previous years, and it definitely affects homebuyers, many who are paying up to 60 percent more.” The NAR estimates more than 1.4 million New York metro households were priced out of the market this year.

Currently, rates are over 6 percent, and Evangelou predicts they will stay in that range through the end of 2022. “While there has been a decline in home sales, I think prices will continue to increase, but at a slower rate,” she said, explaining that housing inventory is still falling short nationwide.

In terms of affordability, the forecast is still dim for the short-term future. “Households need to be earning about $200,000 per year in order to be able to afford half the listings in the New York metro area,” she revealed.

While 2021 was the best year in the housing market across the nation, this year home sales have continued to drop for the last seven months. “We’re definitely seeing a slowdown in sales, but not in prices,” Evangelou explained. “Our data show that home prices rose by 7.7 percent nationwide for the second month in a row. Because of the severe housing shortage across the country, the prices will tend to remain stable because there’re not enough supply.”

Joseph Rand, panelist and chief creative officer with Howard Hanna/Rand Realty in Nanuet, New York, agreed. “We did hit a record in 2021, but you can’t really compare this year to 2020 and 2021, when sales were through the roof,” he said. “I think we need to compare current sales to the 2019 or 2018 markets, and in that case, home sales are up in most areas of the Hudson Valley.”

Rand hesitated, however, to use the word “recession.” “I don’t think we’re going to see anything like what we saw in 2008,” he added. Fellow panelist Jonathan Miller, president and CEO of Miller, Samuel Inc., Real Estate Appraisers & Consultants in Manhattan, agreed.

New York Metro Area Lags

Still, throughout the United States, number of households rose by 7 percent over the past year, according to recent NAR data. However, some major metropolitan areas like New York lagged behind, at just 6 percent. In New York City, Queens and Kings counties reported the fastest growth in the last decade, at 8.5 percent, and New York County (Manhattan), at 8.3 percent.Conversely, when compared to the rest of the country, the New York metro area has the fifth largest annual population decline. On a national scale, the NAR found that 47 percent of the relocating population has been inbound, toward urban areas, but 53 percent were migrating to suburban or rural areas. “A lot has to do with the shift to remote working, which is five times larger than it was in 2019,” added Evangelou. “Those moving to suburban areas are also looking for larger homes.” In 2019, the average single-family home measured 1,580 square feet, but in 2022, the national average is 1,900 square feet.

Currently, there are some 3.47 million renters in New York metro region alone, and millions more throughout the nation. While married households may fare better with two incomes, NAR statistics indicate that only one in three renters are married. “With high rents, it becomes a challenge for single people to save money to eventually buy a home,” she noted.

Panelist Gabe Pasquale, vice president of New Development, Christie’s International, NY Metro, believes the answer may lie in the development of single-family rental communities. “We haven’t seen a lot of this in the Northeast, but it seems to be growing in other areas of the country,” he said. “This will give younger people a new opportunity to have a single-family home. A lot of millennials are now looking to change their urban lifestyle without being locked into buying something.”

In White Plains, New York, alone, where the average rents range from $1,800 to $2,200 for a one-bedroom, Pasquale said that the situation is not giving people a lot of incentives. “If they continue to rent at these prices, they’re not going to be able to save,” he added.

Miller admitted that while some rents are stabilizing, he doesn’t expect them to nosedive. “It’s hard to image rents coming down to more affordable levels, especially when the rental market is already very tight,” he acknowledged. “I do think that the single-family rental market and the newer ‘rent-to-own’ offerings will be big growth factors.”

Home Owners Don’t Want to Sell

On the selling side, Rand’s concern is sellers who may not be able to afford to sell. “You’re usually going to spend more money when you’re looking to upgrade your home, but now factoring in the interest costs, many sellers have such good rates they don’t want to give up their current homes,” he said. “I think we have to find more creative ways for today’s sellers to be able to sell.”As for the future, Rand cautions sellers and buys against panicking. “We’re not going to see 2008 again when people who had no business buying a home could get a loan. We don’t have bad loans and a foreclosure boom today, and prices are still up 30 percent from two years ago,” he said.

Miller echoed Rand’s sentiments. “Lenders are not losing their minds, and mortgage underwriting conditions are much more conservative now,” he added. While Pasquale believes the fourth quarter of 2022 may not be a great one, he said the fact that there’s still a housing shortage will keep help to stabilize prices. “The fourth quarter will likely be the softest of 2022,” added Trevidi, “but I also believe inventory will be increasing by the spring of next year.”

“The bottom line is that buyers can’t make an offer that’s 20 percent below asking and expect to get it, but sellers shouldn’t reject a decent offer,” noted Rand.