News Analysis

MSCI Inc. dealt a surprising blow to China last week, by again delaying to add Chinese A-shares in the company’s benchmark index for emerging markets.

The market index provider rejected inclusion of Chinese shares into its MSCI Emerging Markets Index, due to worries surrounding transparency of the Chinese markets and capital controls of regulators.

In the end, it was the correct decision. While China has worked over the last year to improve accessibility and liquidity, MSCI’s decision is a wakeup call. Beijing needs more action, less talk if it wants to be treated like any other capital markets.

Surprised?

MSCI’s decision caught many international banks by surprise, as Goldman Sachs, Citigroup, and HSBC all expected China A-Shares to join the global index this month, with Goldman pegging China’s chances at 70 percent.

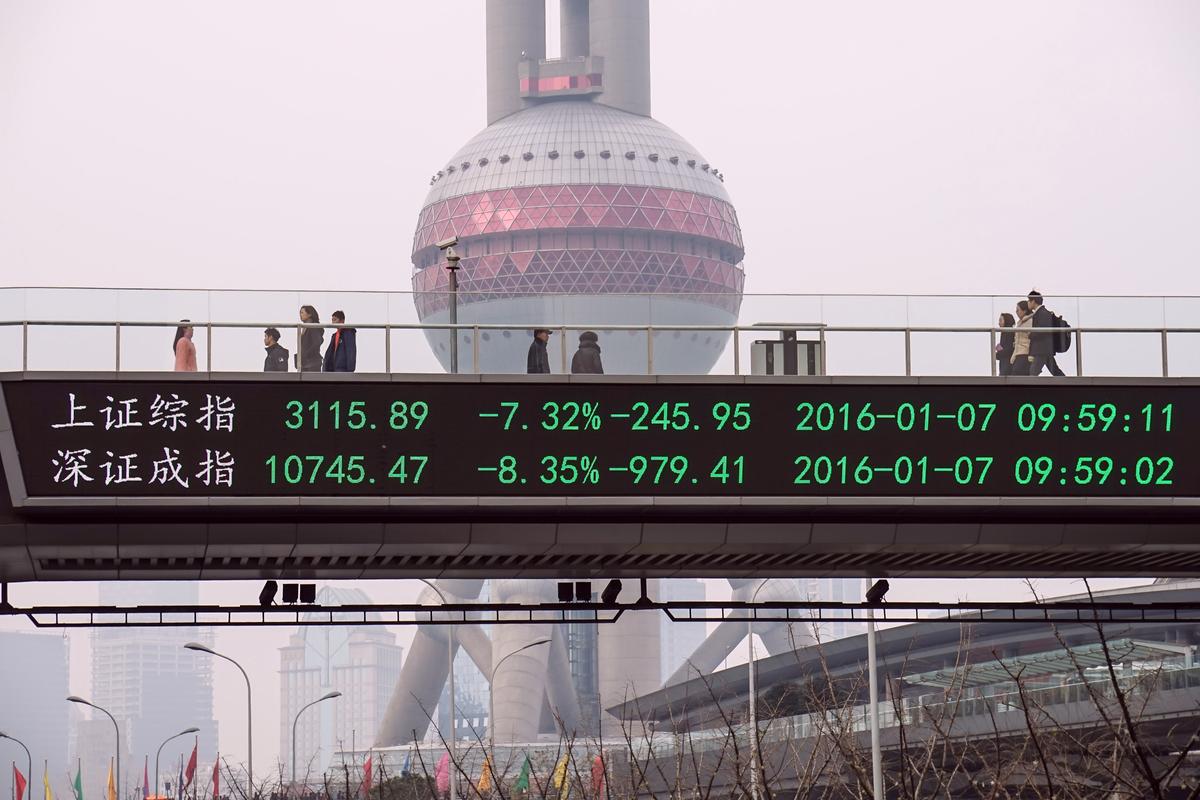

But it really shouldn’t have been a surprise to market participants. Last year’s snub by MSCI was announced in June—in the midst of the Chinese stock market bubble—and the Chinese Communist Party subsequently outlined a number of market liberalization measures to meet MSCI’s requirements.

Then the bubble burst and stock markets crashed. Assurances of a free market with minimal intervention were quickly discarded.

Regulators resorted to wide ranging measures aimed to stem the stock market decline last summer, including halting initial public offerings, banning short selling of shares under threat of arrest, forbidding major shareholders from selling any stock, forcing banks and institutional investors to pledge buying more shares, and running editorials in major state media encouraging investors to purchase more shares.