Well, she said it. No legislation, no vote, no court decision, and not even an executive order. It was only one announcement from a lifetime bureaucrat. But it changes everything.

“Our intervention was necessary to protect the broader U.S. banking system. And similar actions could be warranted if smaller institutions suffer deposit runs that pose the risk of contagion.”

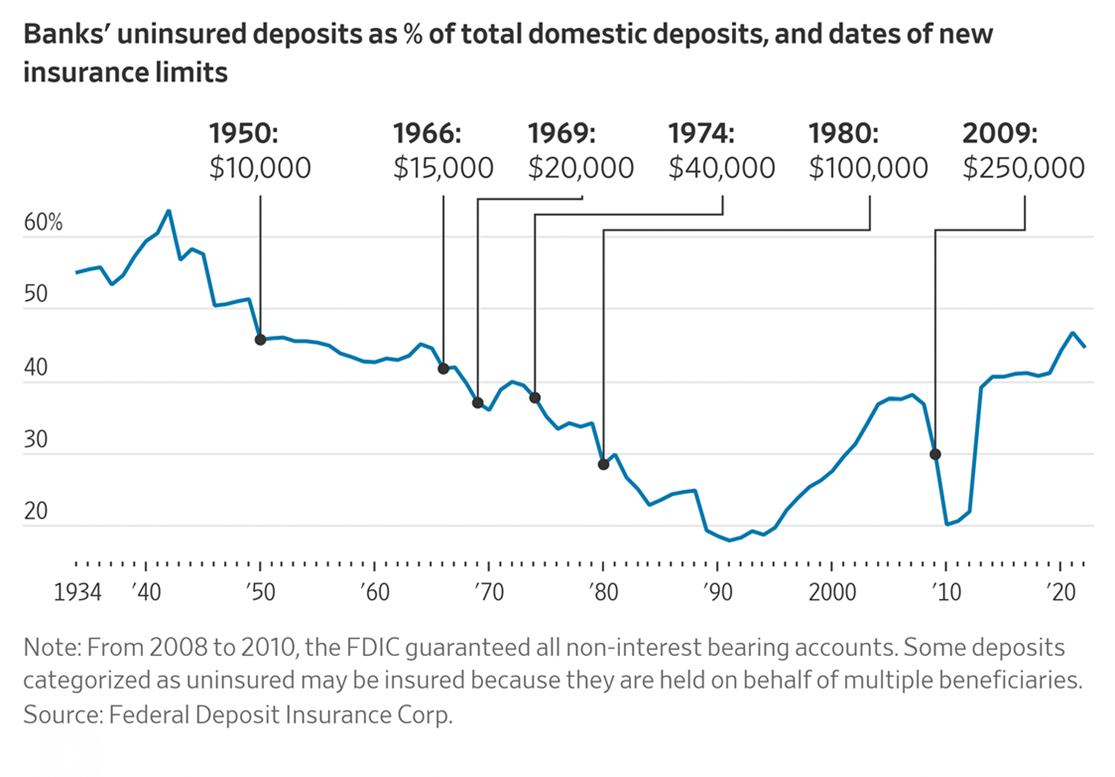

Let’s be clear. There will be more banks. Soon. They will be small, medium, and big. The SVB bailout sets a bad precedent. And now the secretary of the Treasury has flat-out said that it’s a precedent. That means that the current limit of $250,000 in insurance per account is a fiction. It will not be enforced. All deposits are hereby guaranteed to their existing market value.

Every bank that gets in trouble in the coming months and years will be able to scream to the feds that they need a bailout too, or else the country will face grave contagion, and they will get it. The government already arranged for the Federal Reserve to add $300 billion in Treasury purchases to its balance sheet last week. That was just for a few rescues.

If it’s just the beginning, there will be no end to the bailouts. And whatever Fed policy says otherwise concerning tighter money and a more hawkish policy is thereby made moot.

This is truly a turning point in the modern history of American finance and even the world economy. It commits the U.S. government to a liability that could be as high as $20 trillion, probably more, and makes it clear that there will be no more failures resulting from the mistakes of the banking system itself.

Banks and depositors both respond to changes in the level of deposit insurance, obviously. When the limit was raised to $250,000 from $100,000, the amount of uninsured deposits initially went down, before rising higher than before. That’s how moral hazard works: it rewards the very behavior that one is trying to avoid. That decision after 2008 was a true disaster but was decried by only a few. Now we have truly embraced disaster.

To put a fine point on it, this could be the end of private banking and a major step toward the nationalization of credit. It certainly will achieve nothing to bring us back to a world of 2 percent inflation. We might as well get used to 5 to 10 percent, barring some huge change of policy or a change in the regime.

Apocalyptics for a very long time have feared that the current fiat money system will go the way of the Weimar regime, and these developments certainly don’t put an end to such speculation. It could happen. No hyperinflation in history set out to be that way. It comes about because of dangerous and deeply reckless promises by governments that cannot be kept unless there is massive money printing going on.

We might have thought that in the 21st century, central bankers and governments were too smart for such policies, that perhaps they have learned from history that fundamentally undermining the soundness of currency is a sure path to dramatic decivilization and the advent of barbarism. One would have hoped so, but we live in strange times in which the wisdom of the ages counts for nearly nothing. If the regime can go for two years denying such fundamental truths as natural immunity, they can certainly conduct a monetary and banking policy that disregards the lessons of all of history too.

Many observers have also speculated that the impending chaos will pave the way for a central bank digital currency and a social credit system of political compliance. I would love to report that this is a crazed conspiracy theory. Sadly, there is a vast amount of evidence to support this idea, including a Biden administration executive order that insists on driving the United States toward just such a system.

Gov. Ron DeSantis has shepherded some legislation in Florida that changes the commercial codes in the state to make that state a no-go zone for the new digital currency. While this is commendable and great, whether it will achieve the goal is another matter. What we really need are some dramatic moves to make other forms of currencies legal that can protect the citizens against the depredations of central bankers.

Fortunately for this generation, we have just such a technology in the form of bitcoin and its various decentralized offshoots. There is a reason that bitcoin has taken off in terms of its pricing over the past three months. It was conceived of in 2008 during the most recent major financial crisis as a means to provide protection against the last one. It is now up 70 percent for the year.

It’s notable that during the whole of government lockdowns and pandemic-era chaos, bitcoin never flinched. It kept right on doing what it has been doing for the past 14 years, which is enabling peer-to-peer transactions without a financial intermediary, with no double spending, no inflation beyond what its protocol allows, and without any fundamental compromise of the existing code. And it is not only bitcoin but also other tokens that are similarly decentralized in their ownership and control.

Note, too, that all the chaos of the past year in the crypto market generally hasn’t affected bitcoin, and that’s for one reason: it’s not an exchange. It’s not a company or an owned product. It’s a ledger that lives on a public blockchain, which is to say that it doesn’t require trust and does not live off institutions such as deposit insurance and central-bank liquidity guarantees.

There is no sense in making promises about the price of bitcoin next month or next year or in ten years. We simply cannot know. But we do know the protocol and we have strong evidence of its performance over nearly a decade and a half. It’s a system that does not require trust, which means that trust cannot be lost in it either.

But isn’t government in a position to shut it down? It can certainly regulate, control, and even shut down the on-ramps and off-ramps from crypto to dollars (or any national currency) and back again. But within the bitcoin ecosystem, government so far has shown that it cannot really exercise systematic control.

F.A. Hayek spent a lifetime thinking about issues of money and banking, concluding in the end that governments can’t be trusted with the management of money. No rule, no legislation, no regulation can finally prevent them from using and abusing the system for their own benefit. After he received the Nobel Prize, he decided to let loose with his private opinions. He came to believe that the only real solution to a government monopoly of money was to take it completely away from governments.

At the time, the only technologies available to achieve that were gold and other commodities, and he speculated that they could be used to fashion a newly privatized currency. That did not happen in his lifetime. But finally bitcoin did come along to give us a look at what a truly private currency for the digital age could look like.

Governments for years called this technology a scam. Now that it is obviously not, we see government attempting to nationalize the technology for themselves and take it over. The result for society would be the certain doom of privacy and even freedom itself. Might people such as Yellen be working in a destructive way for the ruination of the current systems so as to implement their nightmarish vision of a totalitarian future? Anything is possible.

Certainly, Yellen’s incredible promise of endless bailouts regardless of existing law doesn’t bode well for the future.