Last week the People’s Bank of China (PBoC) cut the overall required reserve ratio (RRR) by 25 basis points (bps). PBoC claimed officially that an amount of 530 billion yuan or equivalently 83 billion USD capital would be released. This sounds a huge amount. Imagine, without any interest rate cut or extra money printed, such RRR cut can generate an amount of exactly 20 percent of the first quarter GDP. But the newly released GDP increased only by 1.3 percent on a quarter-on-quarter basis; even adding inflation to make it nominal it is still way below 20 percent.

Maybe we should not be that serious about the discrepancies. After all, none of the official numbers are reliable. Yet, these unreliable numbers do reflect over time a consistent or probably reliable downtrend. The downtrend of most economic numbers with the ongoing debt crisis together suggests a series of monetary accommodations is needed, but this is tough against the backdrop of global tightening where local easing would bound to drive capital net outflow. Thus, the only way out is postures rather than deeds: pretend to be instead of actual easing.

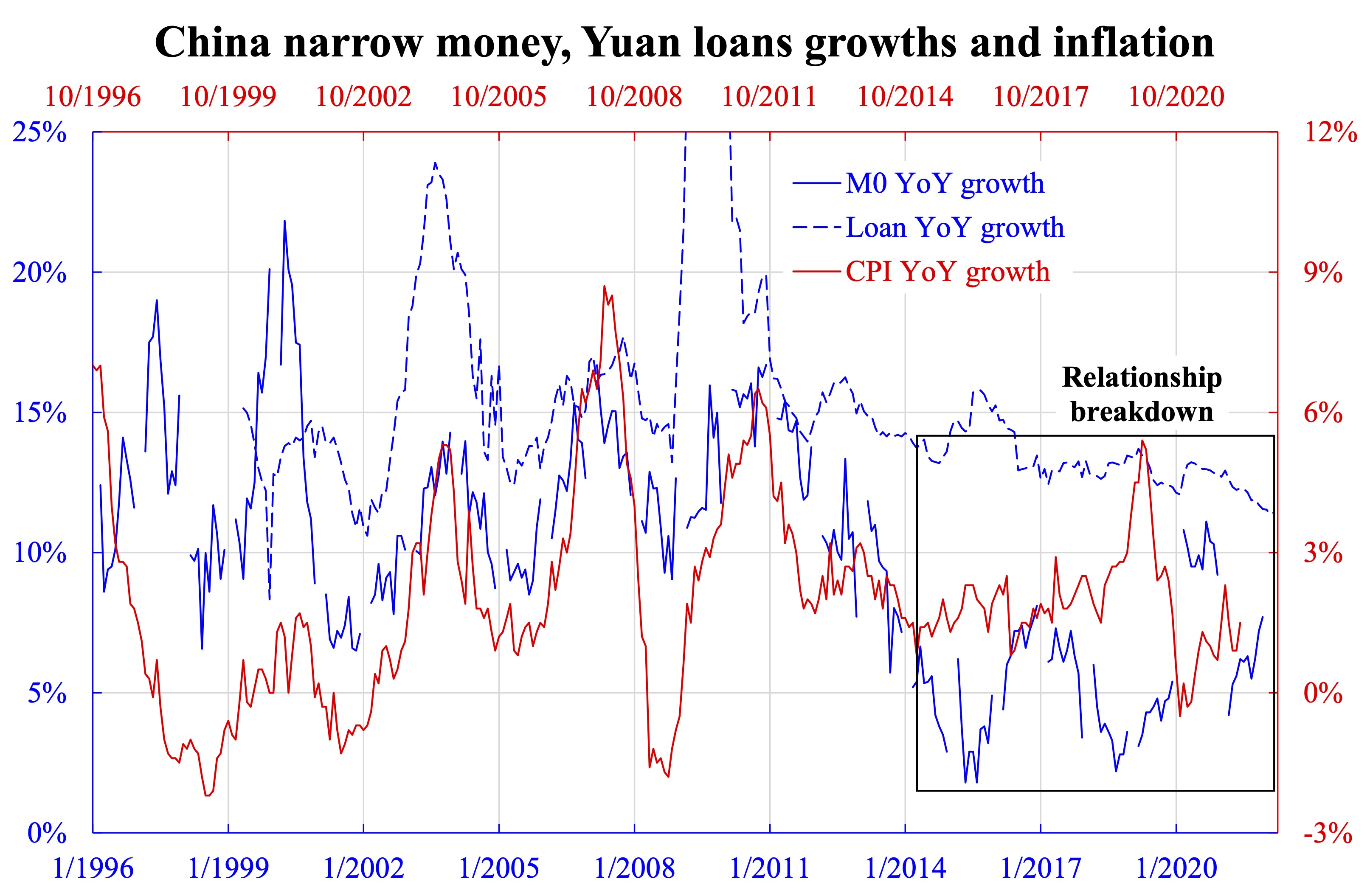

Should the easing be real, there would be one figure not lying—monetary base or narrowest money, which is M0. A glance over the trend of M0 (year-on-year) growth concludes China has not been really easing crazily since 2014. The experience in 2004 and 2010 show that loans surged more than 20 percent and were mostly real estate originated. But the series of developers’ debt defaults over the past few years gave a clear warning to PBoC that easing could not be done as before. Except for 2020 with Covid burst, M0 growth remained low.

More problematically, China has probably fallen into a liquidity trap despite the interest rate is still far from zero. This is easily seen where M0 growth remained flat while loans growth fell from 2014 to now (the boxed part). What’s more, inflation pressure remained generally low. There had been strong correlations between the three before that but broke down afterwards. Printing money steadily with loans growth declining and inflation being subdued, the excess money must have been either outflowed or used to pay back the past, i.e., repaying debts.

If handled by an invisible hand, low inflation provides more room for lower interest rate. Yet this also means capital would outflow under interest rate parity, which is also consistent with the viewpoint from an invisible hand where capital moves from the bad place to good. If on the other hand PBoC hands off, then an invisible hand would drive up interest rate under bad credit background. Such unwillingness to lend would lead to sharper recession but recovery could arrive sooner. The Chinese government is obviously reluctant to take the latter approach.

The only ending remains is a Japanese type: A prolonged debt defaults with low growth of everything. The rich Japan (in terms of GDP per capita) took two to three decades to fix it; for poor China you can imagine.