Everything seems to be well in China, maybe except for the rising defaults. The currency is up almost a percent against the dollar for the last month and foreign exchange reserves only decreased by $4.1 billion, to $3.2 trillion. Long gone are the months of triple digit reserve drain during the turn of the year.

But underneath the surface the picture may not be as rosy.

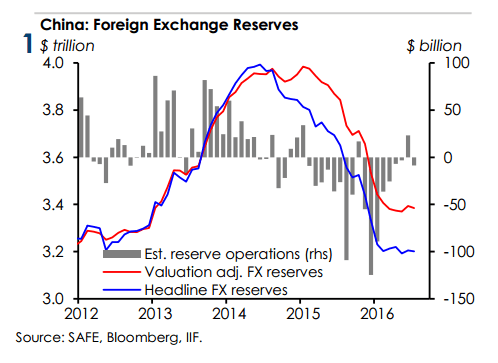

“Our preliminary estimate of People’s Bank of China (PBoC) reserve operations suggests that net capital outflows amounted to some $39 billion in July, marking the largest net outflows in six months,” write the Institute of International Finance (IIF) in a report.

So all the money that China made exporting goods, and then some, just stayed abroad. “We would not want to read much into a one-month pick up in capital outflows but we continue to caution that investor concerns about the policy environment and

pace of economic growth will continue to influence the rhythm of capital flows to China,” the IIF states.

Worth Wray, the chief economist of STA Wealth Management, thinks there is a high risk that outflows could pick up again very soon. His premise is that while Chinese currency reserves are still high in absolute terms, and should be sufficient to finance trade, they will not last long if Chinese citizens lose confidence in the economy and move money abroad wholesale.

“There’s a difference between having enough reserves to meet normal balance-of-payments needs and adequate reserves to defend resident-driven capital flight in a panic. My point is that the buffers continue to fall and Beijing can’t keep following this policy course forever,” he told Bloomberg.

He compares the exchange reserves against deposits available in the banking system, made up of the savings of companies and citizens, also called the M2 money supply.

The ratio is now at its lowest level since 2003, according to Wray’s figures.

“We’ve seen an alarming fall in the ratio over the last few years. It was as high as 27 percent as recently as 2014—when FX reserves totaled more than $4 trillion—but is now closer to 14 percent. That’s well below the [International Monetary Fund]’s advisable 20 percent threshold,” he said.

In other words, while M2 is increasing—deposits in yuan can’t really leave China, it’s the owner who changes hands—because of new loan issuance, foreign exchange reserves are decreasing because citizens exchange the money for U.S. dollars and other foreign companies.

According to investment bank Goldman Sachs, Chinese residents buying foreign assets made up 70 percent of capital outflows during the last 9 months.

This estimate is consistent with survey data from FT Confidential Research. More than 60 percent said they are moving money overseas because of risk diversification and more than half expect the Chinese economy to slow further. A total of 56.8 percent of respondents said they will increase their investment overseas in the next two years.

(Source: FT Confidential Research)

The survey also confirmed the Chinese tendency to overpay for assets, as almost a third of respondents said they are looking for attractive returns overseas. It seems in their case, it is the return of their money, not the return on their money that counts:

Aaron Wu, a 31-year-old financial worker in Beijing, invested more than A$1m ($770,000) last year in a Sydney apartment and another A$240,000 in Australian shares after losing more than Rmb1.5m on the Shanghai stock market. The domestic stock market crash was a watershed moment for Mr Wu’s asset allocation strategy, he said.

China has tried to counteract this trend by making moving money abroad more difficult and 67.6 percent of the respondents say it has become harder to circumvent the $50,000 limit.

According to Assia Nikkei review, the PBOC has told banks in a private meeting last month to clamp down in international transactions but didn’t make new regulations official.

And it’s not just the citizens moving money abroad. Companies, whose deposits are included in the above M2 analysis, are also buying foreign assets to the full extent of the law.

Chinese companies bought a total of 493 foreign firms for $134.3 billion during the first half of the year, according to a report by PriceWaterHouseCoopers (PwC) cited by ChinaDaily. This is an increase of almost 350 percent compared to the same period last year.

Contrary to its citizens, the regime is encouraging companies to take over foreign firms, following the Chinese premier’s Li Keqiang’s “going out” policy.

“The outbound M&A is an irreversible trend in the long term,” Liu Yanlai of PwC states in the report.