Currency devaluation is inflation. How the drop in the currency’s value comes about is another question, though ultimately for consumers and businesses the answer to it might not matter. When that price declines, it simply means the relative value of goods and services available to be exchanged for it has gone up. Once money is cheapened, real things become more valuable by comparison.

In an interconnected world, this also includes the relative exchange rates of one currency to the next. When any plagued denomination goes down to devaluation, others rise up against it. Should the U.S. dollar be made much cheaper, for example, everyone knows this would lead to its downfall, a rapidly falling exchange value.

This is, after all, exactly what we’ve been told has happened over the past couple of years. As with most mistaken impressions, it begins with some truth. The government had, indeed, gone extra crazy with its finances. Some like to include the Federal Reserve’s ultra-QE (quantitative easing) in the mix, and for argument’s sake, I won’t battle the point here (there’s no need).

Combined, American authorities are alleged to have killed the dollar, therefore this explains the painful inflation currently ripping through the U.S. economy.

There was no money printed nor devaluation of any sort. And we know this, without doubt, because the monetary system itself tells us as much. We don’t have to depend on the financial media or the government to interpret the situation for us and therefore lie about what they say they are doing about it (Fed rate hikes).

They, not the currency, did.

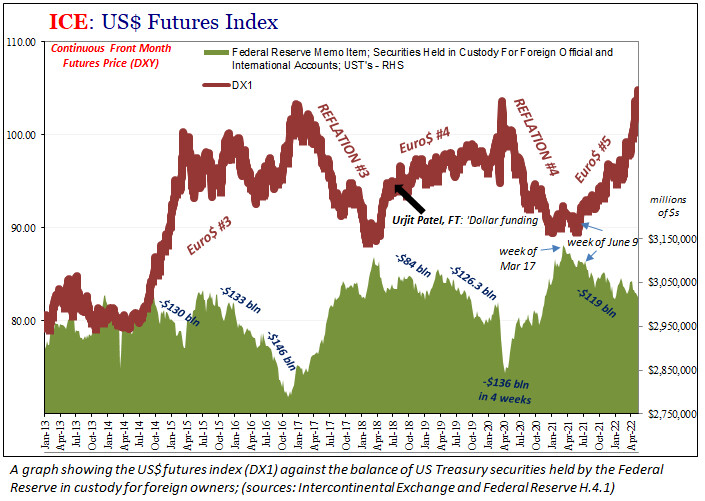

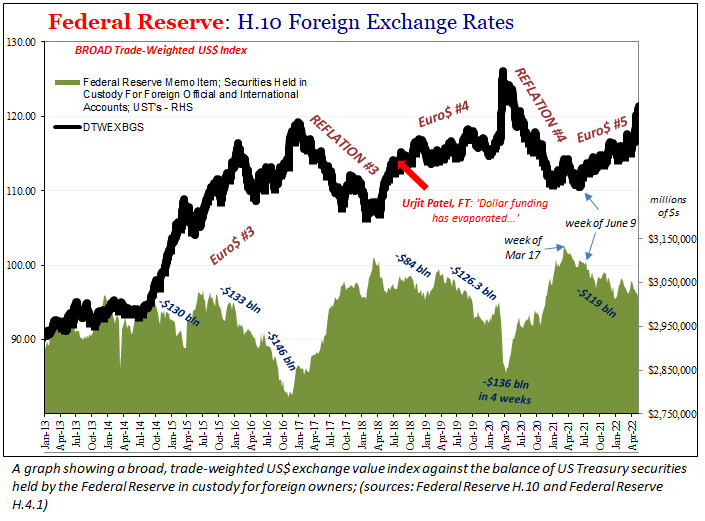

At the same time DXY and others are surging (above), we find the Federal Reserve’s New York branch (FRBNY) custody of U.S. Treasury assets owned by foreign mostly official holders “disappear.” In truth, the Treasuries don’t actually disappear, they are removed from custody with FRBNY to be used somewhere in that official’s jurisdiction as an attempt to deal with a local dollar shortfall.

If fewer dollars (or usable dollar-denominated collateral) are available in places around the world such that overseas central banks and governments have to do something about it (including lending their USTs previously held in custody in New York to commercial banks in their area who might be having trouble sourcing good collateral), therefore those on the wrong end will have to pay up for their trouble; dollar up.

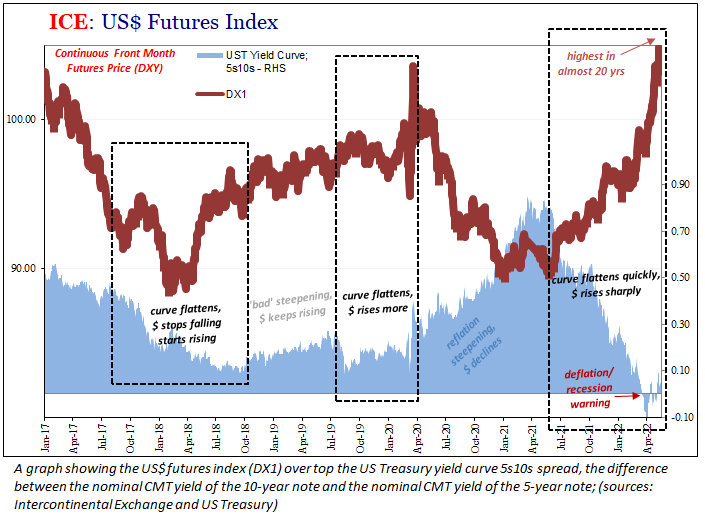

Dealing with tighter monetary conditions, therefore, worsening perceptions of economic growth potential, means flattening curves, particularly (but not limited to) the U.S. Treasury yield curve. As the bond market reduces the additional yield in between short-term and longer-term instruments, that’s another straightforward signal consistent with the rising, rather than falling, dollar.

For example, one such key yield curve spread, the difference between the yield for the 5-year note and the yield for the benchmark 10-year note, this one can tell us quite a lot about how the deepest, most sophisticated market humans have ever conceived is perceiving changes in the balance of risks.

The short end of the yield curve, up to the 5-year note, is a measure of short-term rate expectations (including rate hikes by the Federal Reserve). The long end of the curve, around the 7- or 10-year maturity, builds off those shorter rates into growth/inflation expectations over the long run. Therefore, if the difference between the 5- and 10-year is becoming small, or even negative, that kind of flattening isn’t good nor inflationary.

As you’ve maybe heard or, if not, have already guessed, the 5s10s spread is negative as I type this (and has been on and off since mid-March), having fit all-too-neatly with the dollar’s rise.

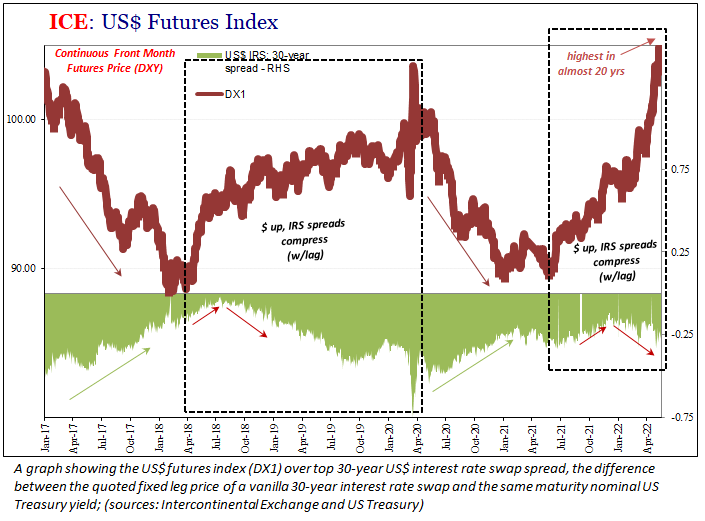

Just to be thorough, I’ll toss in one other financial data point: swap spreads. While the swaps market can be dense and counterintuitive at times, its overview is pretty straightforward. When spreads are decompressing, moving higher, that’s a clear sign of less of a global dollar shortage, when the dollar falls. Conversely, compressing swap spreads, going down, especially now given rate hikes, these are consistent with both the rising dollar as well as what the rising dollar truly represents.

The swap market tends to act with a lag, once factoring one it’s just more evidence for why there hasn’t been a whiff of devaluation anywhere, and in its place real havoc in financial markets along with the real economy.

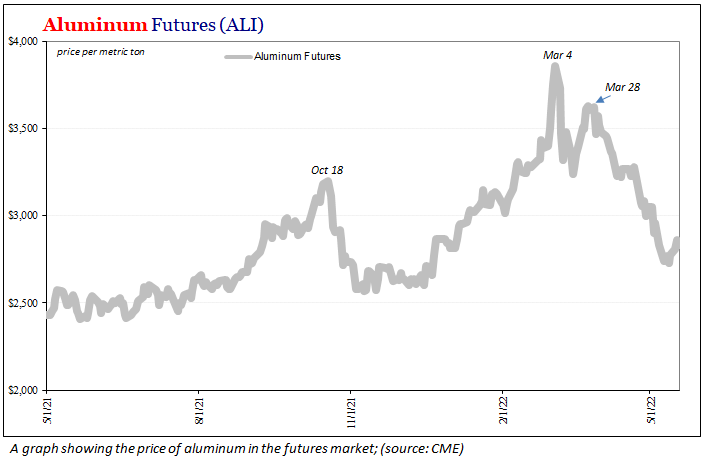

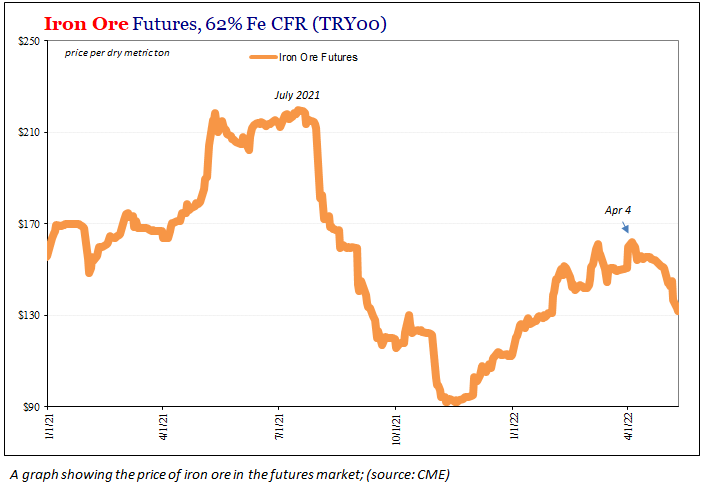

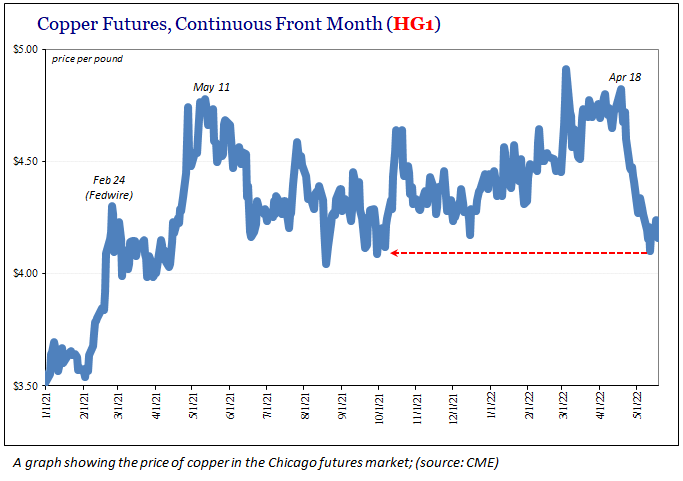

In addition to that financial “volatility,” there has been a late entry into this deflationary mix: industrial commodities. Crude oil has stolen all the attention in the commodity space, not without reason, but others like copper, iron, and even the formerly-invincible aluminum have now reversed.

It was never inflation and that is why the dollar has gone way up rather than way down. Unfortunately, what that ultimately means is the entire global system is increasingly likely to leap out of the frying pan (supply/price shock) and into the fire (recession).