While this sounds like something from earlier this year, the story here begins in 1948. Actually, it starts back in 1946. The Europeans having suffered directly the devastations of World War II, and with much of American and undamaged global supply still on a wartime footing, postwar prosperity quickly grew into systemic price imbalances.

Demand for non-lethal goods came roaring to life after having previously been shut off for more than a decade and a half. First the Great Depression, then the war, global consumers had been patiently waiting for their day to come around again.

It did early in 1946. Except, industry wasn’t nearly ready for it. While spending soared, supply was slow to respond given rigid government dictates and very real physical limitations. As real economics (small “e”) teaches us, a sharp rise in demand for these serious and persistent supply restraints can only balance through rapidly rising prices.

Within the blink of an eye, the U.S. consumer price index (CPI) went from a gentle 1.69 percent increase (year-over-year) in February 1946 to more than double digits, 11.6 percent, in a matter of six months (August). Just four months further on, December 1946, the CPI was rising at an 18 percent clip.

Eighteen!

At first, those at the Federal Reserve were more worried about bonds than consumer prices. The central bank mandate for stable inflation didn’t come about until much later, during the Great Inflation of the 1970s (contrary to popular perception, the vast majority of the Fed’s history is littered with incompetence and grand failures). At this time, the institution’s primary role was to ensure smooth sales for the government’s debts.

Up to 1946, this directive from Treasury was more symbolic than anything. Before then, the Fed didn’t need to enter the debt market because that market was more than willing to absorb massive UST issuance, first from the New Deal, then to finance WWII. Banks repeatedly demonstrated their unshakable preference for safe and liquid assets (at the expense of lending, therefore economic growth).

With the CPI nearing 20 percent rates, however, officials at the Federal Open Market Committee (FOMC) began to wonder just how long the domestic banking system would continue to purchase Treasurys at the low yields the Treasury Department commanded.

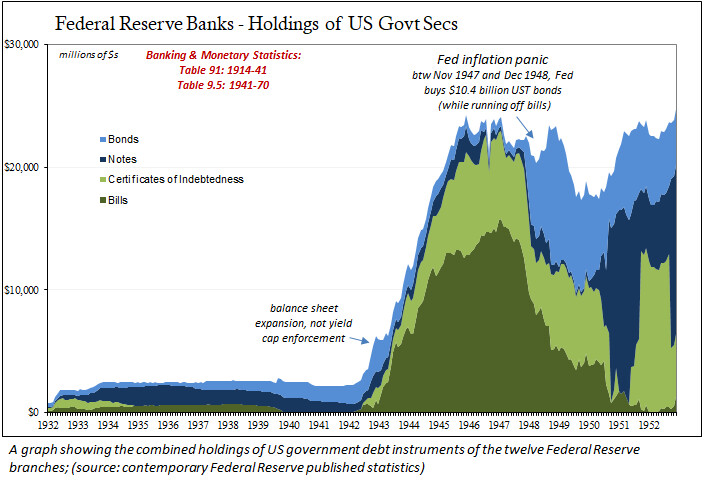

Even though consumer price gains had slowed considerably from a peak rate of 19.7 percent in March 1947 to “just” 10.6 percent that October, the Fed began to buy longer-term Treasury bonds anyway (while at the same time rolling off its large hoard of Treasury bills). From then until November 1948, bond purchases totaled a whopping (for the time) $10.5 billion.

Accounting for the bill runoffs (about $8.4 billion) and several sundry other balance sheet items, all combined had led to the sudden (out of thin air) creation of roughly $1.75 billion in fresh bank reserves.

This hadn’t initially seemed much of a problem. The rate of general consumer price increases continued to decline, reaching a low of 6.8 percent by March 1948.

Then, seemingly out of nowhere, the deceleration reversed. By July, the CPI was rising at just about double digits all over again. In the midst of creating these bank reserves at the Treasury’s demand, policymakers were doubly concerned that what had been a supply-driven shock in economics might unravel into full-blown inflation.

During August of that year, Thomas McCabe, the Fed’s Chairman, traveled up the street to Capitol Hill to inform Congress it needed to reauthorize the use of reserve requirements—the very same that had been misused only a decade before, plunging the economy back into depression in 1937—lest they risk ending up in the monetary territory of Weimar Germany (only slight hyperbole on my part).

“In view of the pressure of current demands, the continued shortages of many goods, the limited capacity for increased output, and the available accumulations of liquid assets, further credit expansion will add to the pressure for rising prices.”

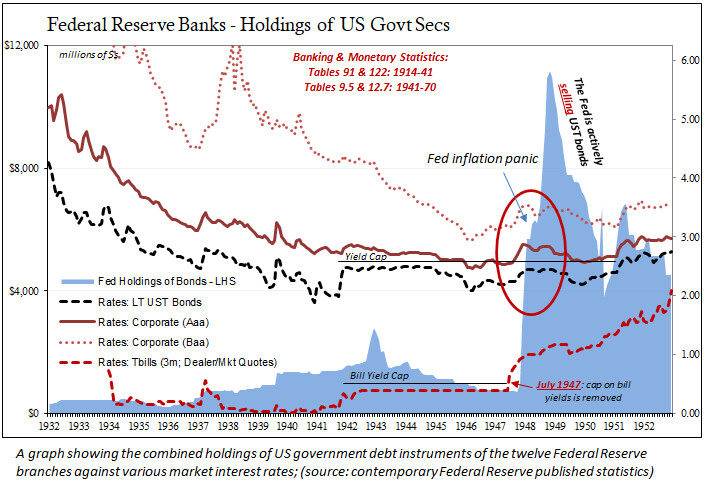

What most on the FOMC really wanted was to be set free from their perceived requirement to buy bonds to keep yields down (this part is highly contestable, see below; there is more than sufficient evidence to show yields were never in danger of rising and that the Fed’s buying program was a mistake of its own making fearing inflation the market did not). But if Treasury insisted, locking up the reserves created by the purchases with higher reserve requirements seemed the next best thing.

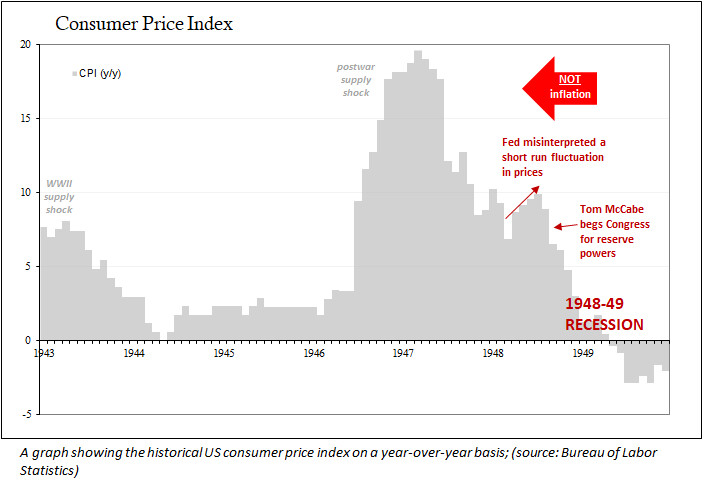

It was, if you haven’t guessed, all for naught. Prior to McCabe pleading in Congress for its approval, consumer prices were on their way back down once again. Before the Fed even began to use those powers, the CPI had receded to 6.5 percent by September 1948, then 1.2 percent by January 1949.

Not because of anything the Fed did or would do; bank reserves weren’t an issue (never are).

Policymakers had fretted over the wrong set of risks. When testifying that eventful August, McCabe had said, “We are convinced that, so long as the present situation lasts, it is important to restrict further credit expansion and to promote a psychology of restraint on the part of both borrowers and lenders.” In other words, without powerful Fed action “promoting a psychology of restraint” the United States was doomed to unending inflationary hell.

But that’s not how inflation works, something the 1948 Fed found out the hard way.

Nothing ever goes in a straight line, however much we might wish for such simplicity and ease. Consumer prices had accelerated, then slowed only to quicken again. Officials merely followed their own biases in selecting which of those to focus on.

As it turned out, the re-acceleration was the last shock to the domestic economic system, one too many to have withstood. What had seemed— to these policymakers, anyway—an increasingly likely path into uncontrolled inflation had really been a final gasp before deflationary recession.

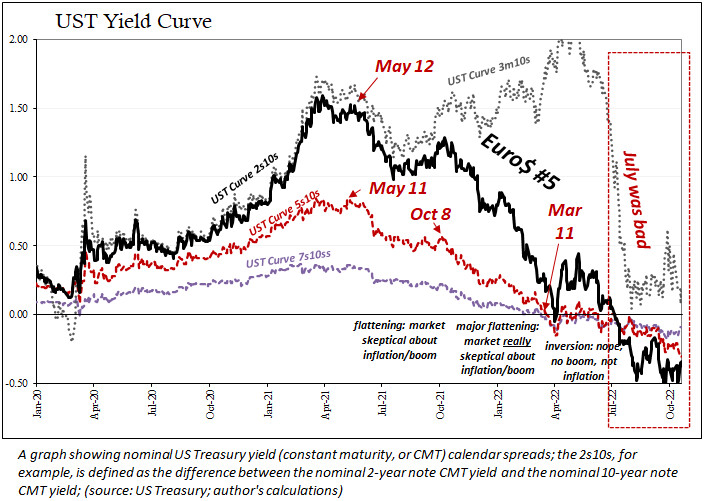

Whether the current Chairman of the Federal Reserve, Jerome Powell, is aware of these specifics is unknown. More than likely, he is not because today he sounds nearly exactly like his long-ago predecessor, McCabe. The rate hikes of 2022 are about the same psychology expressed nearly three-quarters of a century ago. Even the re-acceleration of the CPI.

Though so much has changed from then to now, economic principles have not. Nor has the market’s determination, regardless of what policymakers believe.