In the grand scheme, a half-million dollars may not seem like a lot. For a business that runs on relatively thin margins, though, any surprise cost increase can end up making a tremendous difference. So it was for Long John Silver’s circa April 2021. The “Great Ketchup Shortage” had just cost the restaurant chain that five hundred thousand.

Stephanie Mattingly, the company’s chief marketing officer, told The Wall Street Journal how, “Everyone out there is grabbing for ketchup.” As a result, the business did what you’d expect: they passed along the condiment surcharge to their customers.

The head of Heinz Ketchup would later dispel the notion that the tomato condiment was ever in short supply. CEO Miguel Patricio noted to Time Magazine last June how there’d always been enough, it just wasn’t packaged for how Americans were consuming it right then.

“It’s not that we don’t have ketchup. We have ketchup, but in different packages. The strain on demand started when people stopped going to restaurants and they were ordering takeout and home delivery. There would be a lot of packets in the takeout orders. So we have bottles; we don’t have enough pouches.”

This supply shock manifested across industries. Think about what happened to our work life during 2020: many of us, for example, went from commuting to an office to then working from ill-equipped homes. Employers and employees were forced to spend like crazy on computers and telecommunications gear to make it possible in a relatively short period of time.

Sadly, schools, too.

But producers and assemblers couldn’t easily respond to this drastic change in demand. Like Heinz, operating under financial, physical, as well as government restrictions had left the entire global supply chain more inelastic than it had been since maybe World War II.

Demand for goods like computers skyrocketed, especially when so much of it was being paid for—indirectly, anyway—by Uncle Sam. Sure, they were called loans in the beginning, yet everyone knew the grift would turn such “loans” into grants.

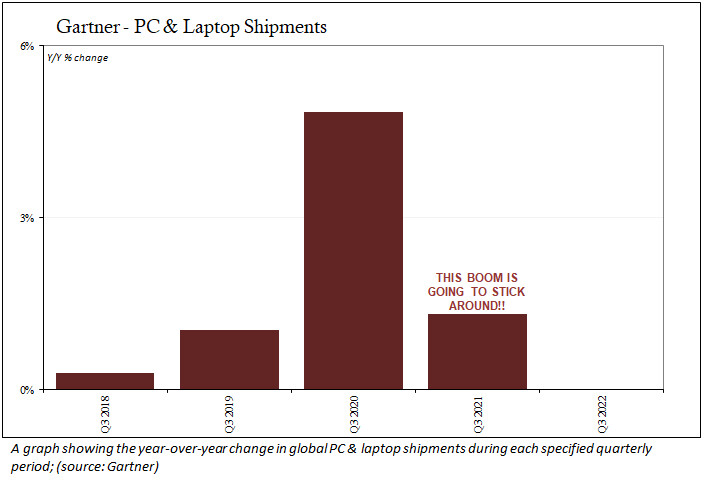

According to the industry source Gartner, shipments of personal computers (PCs) and laptops surged for these non-economic reasons. In the third quarters of 2018 and 2019, total shipments had risen a paltry 0.3 percent and 1.0 percent year over year, respectively. Then the shutdowns and major recession hits in 2020—which suddenly transformed into boom times for the sector.

Redistribution of money and activity for the most unproductive of reasons and all financed by even more harmful non-economic considerations undertaken by the worst participant in every commercial system (i.e., government, in case you were wondering). Freebees, as it turns out, aren’t ever some undiscovered secret to long-term wealth.

The piper would eventually have to be paid and by those actually doing the dancing.

This wouldn’t happen in 2021. For one reason, the federal government introduced more “inflation” first from former President Donald Trump and then President Joe Biden (this sort of insanity tends to be equally bipartisan). Back to Gartner: they figured that as good as 2020 had been for computer manufacturers, 2021 was even better.

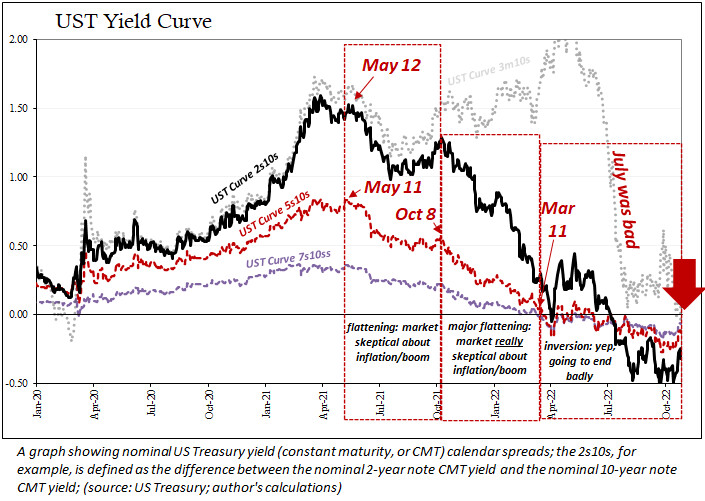

Markets, however, were never so fooled. The U.S. Treasury yield curve, one among a long list of prices and indications, began its flattening odyssey right in the thick of this frenzy. Going back to May 2021, long-run yields started to converge with those for shorter-term instruments.

This is the very same increasingly probable disaster of initially flattened, then modestly inverted, and now totally upside-down curves.

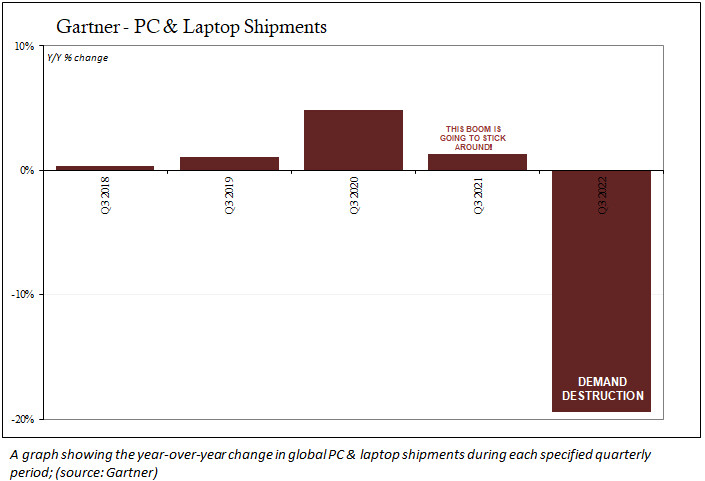

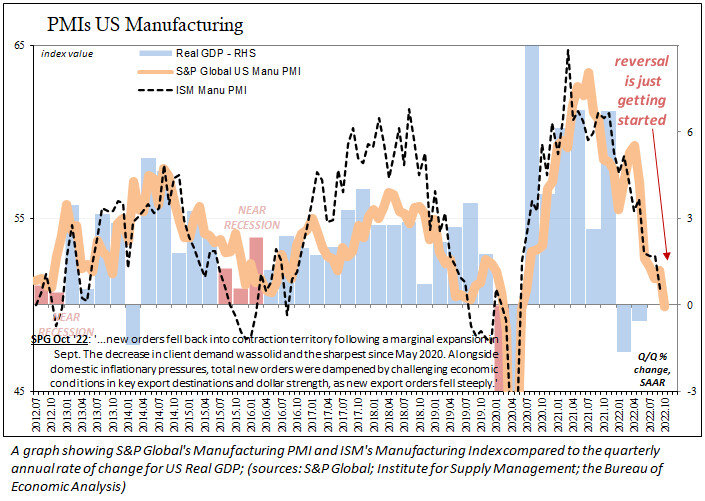

What’s happening in the computer space at large is much worse than just a swing back in the direction of the pre-COVID economy. The most frightening part is that it is just today getting started; everything this year up to now has been no more than a prelude to a gloomier future.

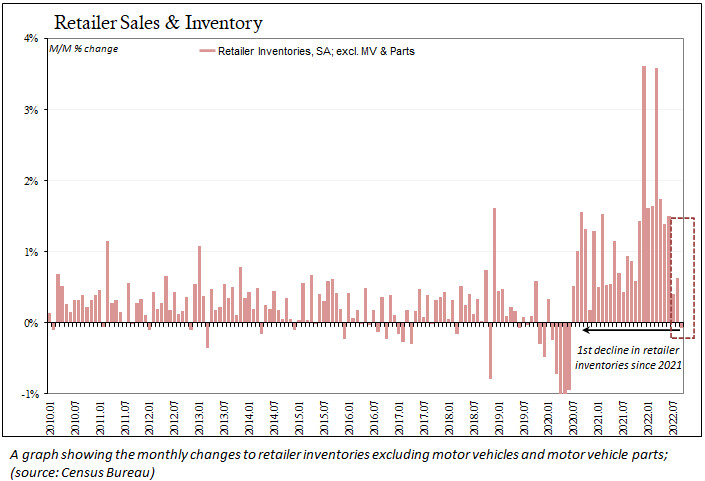

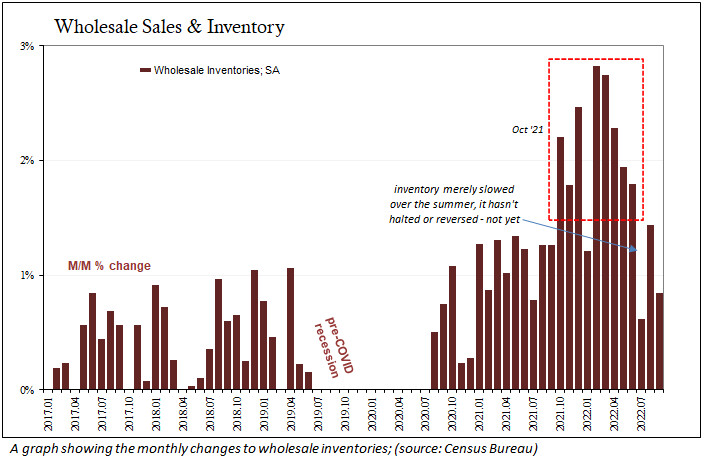

The Census Bureau reported that retail inventories (excluding motor vehicles) shrank in September by the tiniest amount, down 0.06 percent compared to August. It was notable for being the first monthly drop since early in 2021—therefore, the beginning of piper payback.

Now comes the time to really pay—yet where is Uncle Sam? He’s over at the Federal Reserve pleading with Chairman Jay Powell to do something about last year.