It began in Australia when its central bank publicly and clearly stated its quandary. Consumer prices are rising too quickly there as elsewhere, yet more and more it appears as if those prices are leading the country, like the rest of the world, into dark recession.

What to do as a central banker?

The easiest choice would be to (try to) deal with what’s already in front of you. Consumer prices have been causing distress, whereas the contraction, as bad as it may get, remains, to many, only a possibility, even if a strengthening one.

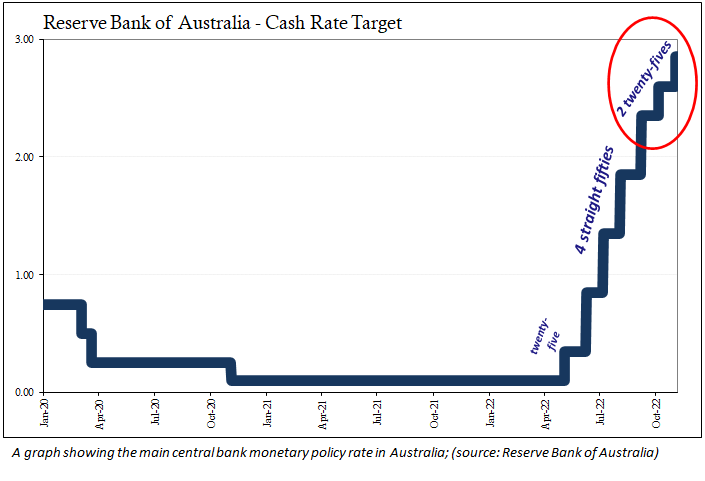

Australian authorities opted for a middle ground, as the Reserve Bank of Australia (RBA) voted to raise its benchmark cash rate by just 25 basis points (bps). This was the second in a row at a quarter-percent, following what had been four straight 50 basis-point rate hikes through the middle of the year, a tacit acknowledgement of the evolving nature of economic risks.

RBA Governor Philp Lowe’s statement from Nov. 1 began by stating, “As is the case in most countries, inflation in Australia is too high ... the highest it has been in more than three decades.”

The “outlook for the global economy,” Lowe said, “has deteriorated over recent months.”

Apparently, it was enough for the RBA to slow down its rate hikes and inject the so-called terminal rate into current discussions. Australia’s economy is heavily influenced by trade and demand from the rest of the world, and if the rest of the world has indeed become cautious, even pessimistic, this would be big trouble for the nation.

In fact, enough to alter the policy trajectory.

A few days later, in London, the Bank of England (BoE) waded into the same middle ground. Consumer prices are surging there, yet the BoE’s forecasts indicate that the United Kingdom may already be in recession and likely will remain in one for as long as two years.

In response, British policymakers raised the benchmark money rate by 75 bps anyway, the largest in decades, before then indicating there wouldn’t be many more like it—or maybe many more at all.

The BoE’s Monetary Policy Committee statement reads:

“The majority of the Committee judges that should the economy evolve broadly in line with the latest Monetary Policy Report projections, further increases in the bank rate may be required for a sustainable return of inflation to target, albeit to a peak lower than priced into financial markets.”

In the United States, the Federal Reserve had its own policy meeting, of the Federal Open Market Committee (FOMC), in between the actions of the other two central banks, and the FOMC raised its rate by another 75 bps. The Fed’s official statement conceded the same difficulties, adding the following language for the first time:

“In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

Immediately after its release, during the press conference which followed it, Fed Chairman Jay Powell appeared to walk back what everyone with common sense had easily interpreted as right in line with the Australian and British dilemmas. Consumer price risks exist, yes, but now in a far more complicated picture.

Yet that didn’t deter Powell. “We have some ways to go,” he said in reference to more rate hikes. “The question of when to moderate the pace of increases is now much less important than the question of how high to raise rates and how long to keep monetary policy restrictive.”

Rather than signal a complete change from statement to press conference, the chairman was instead practicing the Fed’s own brand of non-money monetary policy. Consumer prices are rising too fast in America, too, but the risks of recession are becoming equally a concern. Where Mr. Powell appears different from the others is in how the Fed is attempting to thread the same very fine needle.

The “Old Lady of Threadneedle Street” (as the BoE is also known) has chosen rate hikes anyway, though with more concession on contraction, as have the Australians. The FOMC wants to straddle both sides of the inflation/recession divide less equally, for as long as possible.

Why?

Psychology. Rate hikes are not, in and of themselves, restrictive of inflation or even the economy. Why would they be? Companies which perceive high nominal return opportunities aren’t going to be dissuaded by a few additional points on borrowing costs. If the profit is there, what difference the interest rate?

Furthermore, those who make the loans are only more willingly to do so, given higher interest potential. And don’t get me started on the whole “rate hikes make it more expensive to fund” hokum (an entire topic saved for another day).

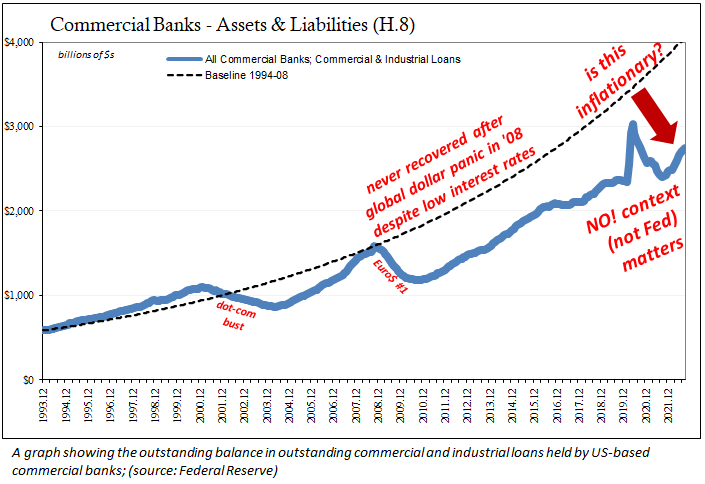

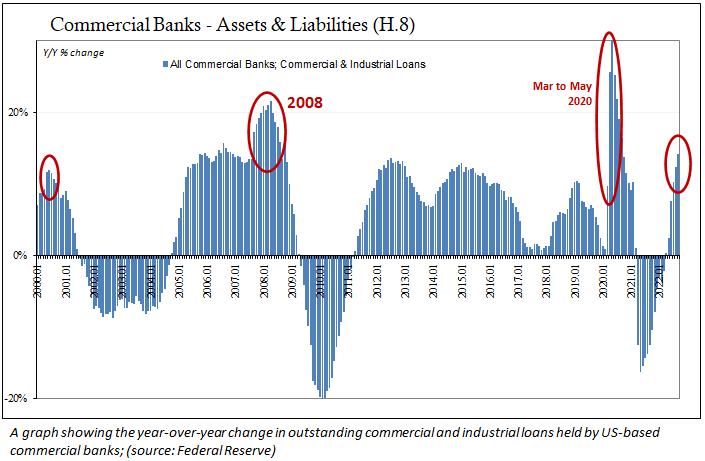

Looking at commercial and industrial credit, an important lending subset, for example, loan growth in it has been outright anemic ever since 2008. However, it has suddenly picked up considerably in recent months—the very same when the Fed is hiking rates!

This borrowing isn’t inflationary, either; rather, it is the typical business response to the same high degree of recession risk perplexing all the world’s central bankers; companies are battening down the hatches, as they did throughout 2008 (or Spring 2020) until the wheels completely fell off the banking system and economy.

He and the FOMC know it is going wrong, a lot wrong, but with the Consumer Price Index where it is, he’s going to try squeeze every last bit of rate-hike psychology from it while the nastiness of contraction is still only a “possibility.” Britain and Australia are just a little farther down the same road of possibility.

All three central banks discussed here are merely trying to find their own unique way to transition from what, for now, seems a middle ground between CPI inflation and downturns if only because recession has already forced itself into their conversations. And which soon shall eliminate any middle ground, eventually making the policy choices of our anglophone trio for them.

Some are more open to admitting it than others. And that explains the chaotic week in global central banking.