To note, while Trump had a rather notable track-record in propelling the U.S. economy into a renewed growth during his tenure, his aggressive policies postponed the recession that should have arrived to the United States in 2020, at the latest. An economy needs to enter a recession periodically (cyclically) to root out excess leverage, over-indebtedness, and unprofitable companies. An economy is meant to develop through (business) cycles. All attempts to remove the cyclicality will make the economy fragile and thus subject to larger business-cycle fluctuations and crises.

The artificial recession, that is, the shutdown of the U.S. economy during the spring of 2020, was probably necessary, for a short while at least, but the stimulus checks and the bailout of the financial markets by the Federal Reserve can be seen as grave mistakes. The former crushed the labor force participation rate and created artificial demand for “stuff from China,” which led to the backlog in U.S. ports and in global freight, thereby setting the stage for the shock of inflation. However, the exceptionality of the situation in the spring of 2020 demanded extraordinary measures and thus the actions taken by President Trump were understandable.

However, the latter—i.e., the bailout of financial markets by the Fed—was something I thought I would never witness. That is, I thought I would never see the central bank of the United States effectively socialize losses in the capital markets. It was stuff straight out of a communist’s playbook.

“On the 16th, the New York Fed announced that it will add $500 billion in overnight loans to the repo market. On the 17th, the Fed announced that it would use $1 trillion to mop up corporate paper from issuers. On the 18th, the European Central Bank announced that it would buy 750 billion euros’ worth of bonds and securities. On the 19th, the Fed announced that it would create a lending facility for money market mutual funds. On Mar. 25, 2020, interest rates of short-term corporate debt surged to 2.43 percent above the federal funds rate, the overnight lending rate of the Fed, which led the central bank to issue a program targeted at the corporate markets.”

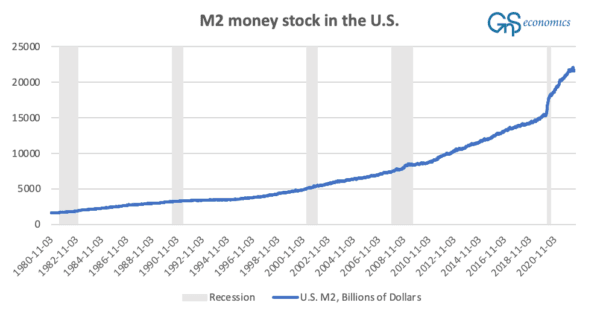

The Fed effectively backstopped (socialized) the losses of investors and companies in the capital markets, and created a massive and wholly artificial increase in the money in circulation in the United States. Thus, the combined effect of lockdowns, stimulus checks, and the Fed bailout created the prerequisites for the inflation shock. However, much graver failures were required for the inflation crisis to emerge in full, and made they were.

“So, inflation has been running higher than shown in the official figures, but the real problems are likely to emerge when economies reopen and conditions move toward a ‘new normal,’ which is now occurring in the United States. Airlines, hotels, restaurants, etc., now have diminished capacity, which means that they may be unable to meet suddenly increased demand.”

At this point, all artificial increase in demand, like distributing “free” money to the populace, just aggravated the inflation shock, and this is exactly what President Biden did. Alas, we can argue that the Biden administration made the shock much worse than it would have been if people would have simply returned to work and not used their free money to buy things and services in limited supply. To top it all off, the push by Biden to increase the minimum wage, which eased the labor shortage a bit, further increased the costs of corporations, fueling the inflation shock.

Moreover, the stubborn policies of the Biden administration and the European leaders regarding sanctions against Russia have created an extremely precarious situation, wherein the whole energy sector of Europe, and thus the European economy, could face a collapse during the coming winter. Moreover, I don’t think there’s a single example in the history of economic sanctions successfully working against any country under an authoritarian rule, and definitely not against Russia.

It is truly baffling how European leaders have been so gullible that they have effectively relinquished their energy independence to Russia, which, let’s be honest, has been an opportunistic aggressor basically throughout her existence. We Finns know that you should never relinquish anything to Russia if you want a functional and mutually beneficial relationship with that eastern neighbor.

So, when the “chickens” of this manipulated economic cycle come home to “roost,” remember to blame the right culprits for it. They can be found in the White House and the Eccles Building in Washington, D.C.