This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

The National Debt Clock, a billboard-size digital display showing the increasing U.S. debt, is seen on the corner of Sixth Avenue and West 44th Street, in New York City, on Aug. 1, 2011. Andrew Burton/Getty Images

There have been three major sovereign debt crisis episodes during the past 200 years. The first one occurred after the Napoleonic wars between 1827 and 1860. The second one occurred during and after the Great Depression and World War II, and the third one during the era of commodity-price and banking crises from around 1987 till around 2000. Now, we are approaching a fourth one.

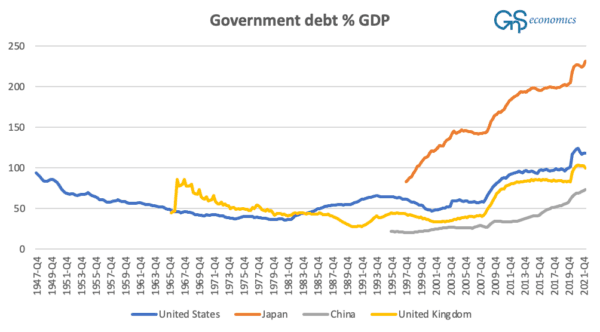

The figure below presents the level of central government debt as a share of gross domestic product (GDP) in the world’s leading economies. It paints a startling picture.

A figure presenting the central government debt as a share of GDP in China, Japan, United Kingdom, and the United States from fourth quarter 1947 till first quarter 2022. GnS Economics/World Bank

Japan is, of course, in its own league, but what is striking, yet unsurprising, is that sovereign debt has basically exploded in all countries since the global financial crisis of 2007–09. This phenomenon was recognized in the March 2017 issue of the Q-Review series, where the authors wrote:

“The crisis of 2007–2008 reversed the trend of financial globalization, which has undermined global growth. The pull-back in financial globalization has been masked by central bank-induced liquidity and continuous stimulus from governments which have created an artificial recovery and pushed different asset valuations to unsustainable levels. This implies that we live in a ‘central bankers’ bubble.’”

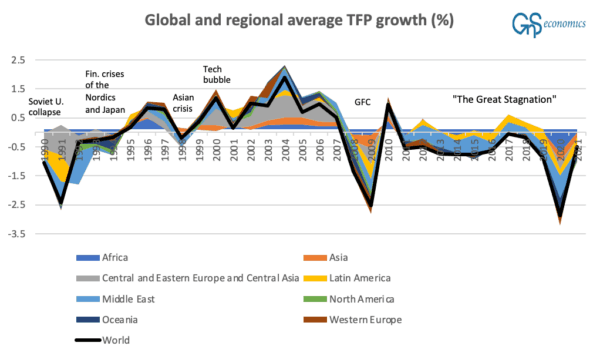

To be more precise, the issue explains that central banks have pushed bond yields to historical lows, which has made it possible for governments to take extraordinary amounts of debt. This also coincides with another worrying global phenomenon—the collapse of global productivity growth—which I already detailed earlier.

A figure presenting the growth of total factor productivity (TFP) in the regions of the world from 1990 to 2021. GnS Economics /The Conference Board

Stagnating global productivity growth is extremely worrying because it implies that firms are unable to increase their productivity, which means that they will be unprofitable as well. And when their indebtedness grows, yet profitability stagnates or falls, their ability to service debt will also diminish over time.

This, quite straightforwardly, implies that the ability to increase profitability and service debt, at the national level, has also diminished for several years, while governments have been racking up debt at record speed. Our economies quite simply have been on an utterly unsustainable path for over a decade, and now ‘chickens are coming home to roost’ with rapidly rising interest rates.

The first “victim” of this was the United Kingdom, where the reckless fiscal policies, especially during the coronavirus crisis, pushed the country to a brink of debt and financial crisis saved only, at the nick of time, by the Bank of England. The crisis also forced the newly appointed Prime Minister Liz Truss to resign, making her the shortest-serving prime minister in British history, with just 45 days in power.

But there surely will be more to follow.

Debt or fiscal crises emerge when an over-indebted nation loses the trust of investors to its debt-servicing capacity. There are numerous examples of such episodes in history. During the above-mentioned periods, close to half of the countries of the world were in some state of default on their external (foreign) debt obligations.

Solving fiscal crises is also not easy or pleasant.

Fiscal (or debt) crises consist of periods of severe deficits in public financing and/or of periods in which the government fails to meet domestic or foreign obligations. Gerling et al. (2017) identify a fiscal crisis by four criteria: credit event (a default of foreign currency-denominated debt); exceptional official financing (e.g., from the International Monetary Fund); implicit domestic default (e.g., monetization ordomestic arrears by the government); and loss of market access.

If a government defaults on its foreign or domestic debt obligations (i.e., interest payments and/or principal payment of its bonds), it eases the debt burden of a country, but tends to lead to capital market exclusions as investors will not be willing to lend to the country, for a while at least. Exclusion from income sources outside its tax revenue leaves the government with just two options: it either has to “live by its means,” meaning that it has to cut expenditures so that they can be covered with diminished revenues, or it can resort to monetization of budget deficits through a central bank. So, in practice, governments need to choose between self-imposed austerity or a runaway inflation after the default.

Since the beginning of the 1950s, countries have also been able to apply for assistance from the International Monetary Fund (IMF) during economic hardship. IMF programs come with austerity measures, which have been conditional on the acceptance of the program since practically from the beginning. These measures include removal of price controls from state economic enterprises and removal of subsidies. During the onset of the program, there is almost always an agreement on the ceiling of the fiscal deficits and domestic credit. In addition, public and private debts are often rescheduled and the nominal exchange rate regime changed (i.e., removal of any currency pegs).

Now that central banks have raised, and most likely will keep raising, interest rates to combat soaring inflation, the debt-service costs of governments will continue to soar. Thus, it’s just a matter of time before more governments of even the advanced economies will lose the trust of investors, like Britain did.

As pointed above, at that point our governments (and central banks) have only two options left: to “tighten the belt” considerably or to monetize “everything.” Alas, we (the world) are either on the brink of the greatest austerity period in history or the possibility of global hyperinflation.

Today’s choices could not be more dire, but fiscal irresponsibility, which we have allowed, breeds suffering in one form or another. It seems that we need to learn that lesson, yet again.

Tuomas Malinen is CEO and chief economist at GnS Economics, a Helsinki-based macroeconomic consultancy, and an associate professor of economics. He studied economic growth and economic crises for 10 years. In his newsletter (MTMalinen.Substack.com), Malinen deals with forecasting and how to prepare for the recession and approaching crisis.