This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

In early October past year, I warned on a looming banking crisis. My warning was based of the near-collapse of the British pension funds in late September, saved only by swift actions of the Bank of England (BoE), and on our analyses on the state of the European banking system.

We had actually issued a warning of an emerging European banking crisis already in May 2020, which was then postponed by debt-moratoria and other exceptional support measures provided by authorities and gorged by banks. These measures carried the European and U.S. banking systems for nearly three years, until the failures of Silicon Valley Bank (SVB), Signature Bank, First Republic Bank and the venerable Swiss banking giant Credit Suisse, broke the uneasy calm in March/April this year.

The only err in my warning was that I assumed that Europe would be the epicenter of the banking crisis. It was based on the assumption that the already weak European banks would be hit by a deluge of corporate bankruptcies caused by fast inflation, soaring energy prices and rapid interest rate rises. Fortunately, winter turned out to be exceptionally mild in Europe, which eased the energy crisis and thus saved our economy, and banks. The Flood of corporate bankruptcies (which we warned would be coming already in December 2019) was postponed. However, the second quarter this year was the sixth consecutive quarter of increasing corporate bankruptcies in Europe; a trend unseen since Eurostat started collecting data in 2015. Europe and the European banking sector are thus heading what is likely to be a grim winter. The flood is coming.

Yet, I am most worried about the U.S. banking system. The in-depth analysis, I have conducted since late February, has revealed that the risk of a collapse of the U.S. banking system is higher than it has ever been since the Great Depression. We are currently mapping the most-safe and most-risky U.S. banks, and have actually already issued a deposits withdrawal warning concerning eight U.S. banks, with more to follow. In this article, I will walk you through the reasons, why the situation in the U.S. is so grim.

When authorities mess-up

In early October, I noted that:

Banks are also currently being hit by heavy declines in the value of government bonds, which they use as collateral. These may easily lead to cascading losses on banks, possibly with never-before-seen speed, size, and width.

As we now know, this materialized in the U.S. around six months later, but how did we get into this point?

The global regulatory arm of commercial banks is the Basel Committee on Banking Supervision (BCBS), which operates under the Bank the of International Settlements, or BIS. BIS is often referred as the “central bank of central banks”, as it provides guidance also for central banks.

In the wake of the Great Financial Crisis, the Basel Committee released its third set or rules, or internationally agreed set of measures for banks called the Basel III. The most ground-breaking, and also the most destructive, concept was the creation of Liquidity Coverage Ratio, or LCR. It was meant to ensure “that banks hold sufficient liquid assets to prevent central banks becoming the lender of first resort", as stated by the Group of Central Bank Governors and Heads of Supervision (GHOS), an oversight body of the Basel Committee on Banking Supervision. The liquidity rules of the Basel Committee set U.S. Treasuries into a category of the safest liquid assets, which meant that they were not subject to ‘haircuts’ in their value, when banks held them in their balance sheet.

While the Federal Reserve has yet to fully implement the LCR rules, it gave pre-notifications of it in October 2013, with a proposed transition period running from 1 January 2015 till 1 January 2017. Even though the LCR has not been fully implemented in the U.S., it’s likely that the proposed transition period affected how banks handled their risk management, because banks knew LCR rules would be eventually coming. Moreover, the Basel II framework, implemented in the U.S. in 2008, placed different risk-weights to bank capital with, for example, the U.S. Treasuries enjoying the lowest risk-weights. These guidelines set by the Basel Committee, and enforced by the Federal Reserve, essentially meant that Treasuries were preferred as bank capital, in addition to cash and central bank reserves.

So, because cash and coins as well as central bank reserves are in a relative short supply and in total control of the central bank, the U.S. banks gorged Treasuries. This is, e.g., what SVB did. That is, it bought the U.S. Treasuries to counterbalance the risk caused by the major inflow of deposits. The leadership of SVB, effectively, did what the authorities wanted, and the bank failed as a result.

The deposit ‘binge’

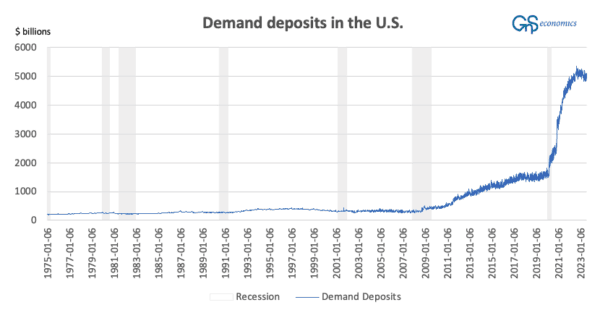

The U.S. deposit base has changed rather drastically during the past three years. This applies especially to easily withdrawable demand deposits, consisting of accounts where money can be withdrawn without advance notice.

A figure presenting the amount of demand deposits in the U.S. banking system in billions U.S. dollars, and U.S. recession periods. GnS Economics / St. Louis Fed / NBER

What was the reason for this astronomical increase in demand deposits between 2020 and 2022? The combination of Corona lockdowns, stimulus checks and massive monetary stimulus by the Federal Reserve.

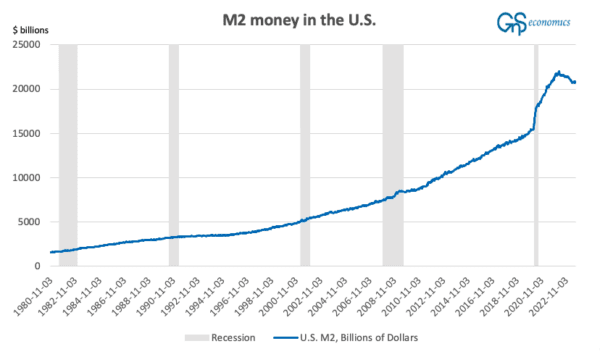

When the U.S. economy was locked down several times during 2020 and 2021, people had very little options to use their money, i.e., to consume. The stimulus checks issued by the U.S. government thus went mostly unused and accumulated into accounts of households, while banks issued vast amounts loans to corporations. In addition, the Fed enacted its biggest ever ‘money printing’ operation during the spring of 2020, which saw its balance sheet grow from around four trillion to over seven trillions USD in just four months! The amount of money in circulation in the U.S. exploded.

A figure presenting U.S. recessions and the amount of M2 money aggregate, consisting of currency in circulation, demand and other checkable deposits, saving deposits, small-denomination time deposits and balances in retail money market funds in billions U.S. dollars. GnS Economics / St. Louis Fed / NBER

The massive increase in money in circulation ignited inflation (on which arrival we warned in March 2021), when the economy finally opened. This forced the Fed to start its most aggressive rate hiking cycle ever in April 2022. In just little over a year, the Federal Funds Rate rose from 0.08% to over 5%. Naturally, the yields of U.S. Treasuries followed. The problem for banks was that the yield and the price of a bond are inversely related. The higher the yield, the lower the price of the bond, and vice versa. Here’s an excellent piece going through math of bond pricing.

Alas, the extremely rapid rise in Treasury yields were catastrophic for banks. For example, the yield of U.S. 2-year Treasure note rose to 20-fold in just two years. This meant that the value of the underlying bond crashed and banks who had acquired Treasuries with near-zero rates (with very high bond prices), suffered heavy losses. These were labelled as “unrealized losses”, because banks obtain Treasuries as held-to-maturity asset. This means that banks hold them to maturity after which the Treasury returns the principal of the bond and pays the interest. Thus, they are not “actual losses” unless the bank is forced the sell Treasuries before they mature, and this is exactly what happened.

The U.S. had been in the grips of a ‘silent’ bank run since summer of 2022, when depositors started to withdraw their deposits and place them, e.g., into retail money market funds offering a higher yield of return than bank accounts. In March, this escalated into a rout. The deposit flee had burned through buffers cash and easily liquified assets of many banks, forcing them to sell Treasuries with a considerable loss. The word got out that SVB had suffered heavy losses from such sales, and panic ensued.

It was estimated that at the end of 2022, the U.S. banks were sitting on nearly $2 trillion worth of unrealized losses. The massive amount of unrealized losses was one reason why the run on the SVB spread, and forced U.S authorities to intervene, strongly.

The panicky response of authorities

The run of SVB started on Friday 10 March, 2023, and on Sunday the 12th, U.S. authorities concluded that there was a risk of a nationwide bank run. To halt it, they devised an exceptional three-step strategy.

First, there was a joint statement from the Treasury, the Federal Deposit Insurance Corporation (FDIC) and the Fed, announcing that all depositor funds (also uninsured deposits) of the SPV and the Signature Bank were guaranteed. Secondly, the Federal Reserve provided $300 billion worth of liquidity into the system and announced that it will make “additional funds” available to all banks in a Bank Term Funding Program, or BTFP. Thirdly, in a highly exceptional move, President Biden appeared on national television to assure that deposits in the U.S. banks are safe. Such a combination of rapid and exceptional actions basically confirmed that the U.S. was on the verge of a nationwide bank run.

In Europe, banking problems emerged as the failure of the Credit Suisse. The “merger” (effectively a shotgun wedding directed by Swiss authorities) of Credit Suisse and another Swiss banking giant, UBS, calmed things down in Europe.

Yet, at the end of April, the crisis re-emerged with the failure of another U.S. regional lender, First Republic Bank. Its unfortunate fate provides important clues of where the crisis is heading.

Liquidity and loans

The BTFP became something of ‘deposit guarantee scheme’ with the amount of 1-year loans sought by U.S. banks from the Federal Reserve growing each passing week, with a declining fortunately. The program is scheduled to end by March 11, 2024, but it will almost certainly be extended to unforeseeable future.

There’s a limit concerning the amount loans banks can acquire through the BTFP. Banks need to post a collateral, a liquid asset (Treasury, etc.) in exchange for the loan, which many banks have limited quantity of. Especially smaller banks tend to follow the traditional model of banking, where the inflow of deposits is counterbalanced in their balance sheet by issuing loans.

For example, the First Republic Bank could acquire only $13 billion from the BTFP, because it held mostly loans as assets, while SVB had acquired Treasuries to balance the inflow of deposits. Alas, both strategies led to failures of the banks, which by itself sends a dire warning on the state of the U.S. regional banking system. Essentially, both the traditional model of banking (issuing loans against deposits) and the one pushed by authorities (acquiring Treasuries) have become ‘death traps’ for banks.

Moreover, while the overall liquidity in the U.S. banking system grew between the first and second quarters of this year, its dispersion (standard deviation) also increased. This means that there were more U.S. banks with smaller liquidity buffers and thus in a higher risk of failing at the end of Q2 than at the end of Q1. The historical comparison of the current situation of U.S. banks also sends a warning of a risk of an outright collapse of the banking sector.

Into the collapse?

In May 1984 Continental Illinois National Bank and Trust, a seventh-largest U.S. commercial bank at the time, failed due to bad loans it had acquired from a (failed) Penn Square Bank and a resulting run of 30% of its deposits. Based on the data at the end of Q2, close to 2800 banks (out of the 4642 retail deposit taking banks at the FDIC database), would fail if they would face a similar run on their deposits that toppled Continental Illinois. To note, run on SVB was 87%, Silvergate 52% and Signature Bank 29% of their deposits.

Small regional banks in the U.S. are currently holding a vast majority, close to $2000 billion, of real estate loans. In regional banks such loans have grown by 35% since the beginning of 2020, and by whopping 147% since bottoming during the last week of 2011. As we know, many U.S. cities are in the grips of a ‘Retail apocalypse’, which is likely to get much worse when recession arrives (which is unlikely to be far). As shown by the failure of First Republic, banks cannot liquidate these loans (except under highly restrictive conditions of the discount window of the Fed).

And, the issue is pressing. For example, the loan portfolio of First Republic Bank consisted 80% of real estate loans. It took losses from its loan portfolio, and had a very limited liquidity buffer to counter the deposit outflow, and failed. There are hundreds of U.S. banks with a higher share of real estate loans in their loan portfolio than what First Republic had. Moreover, thousands of U.S. banks could not cope with the deposit run faced by Continental Illinois.

The loan losses accumulating in the balance sheets of banks can (are likely to) trigger another round of more severe bank runs, leading swathe of U.S. bank failing. In the worst case, we are marching towards a complete implosion of the U.S. banking system.

Raise some cash.

Author wishes to thank Dr. Peter Nyberg for comments. Remaining errors are my own.

Tuomas Malinen is CEO and chief economist at GnS Economics, a Helsinki-based macroeconomic consultancy, and an associate professor of economics. He studied economic growth and economic crises for 10 years. In his newsletter (MTMalinen.Substack.com), Malinen deals with forecasting and how to prepare for the recession and approaching crisis.