An absurd yet apt metaphor for this year’s predicament. It is widely believed that U.S. real GDP change in the second quarter of 2022 will tally up less than zero, just as it had during the first quarter. Should this happen (the estimate won’t be released until after this article is written), does that mean the recession did?

To answer the question with a better one, who cares?

While the White House and its various proxies are busy angering pretty much everyone across the political spectrum by trying to focus attention on recession by overtly and aggressively attempting to litigate its definition on social media, how bad the first half of the year might turn out to have been is no longer all that relevant.

To start with, Treasury Secretary Janet Yellen is, actually, correct in stating there is no “technical definition” of recession. Some guy a long time ago came up with the notion that two straight quarters of negative GDP might be a useful rule of thumb for laypeople who lack the full range of information to otherwise decide for themselves. From there, it has taken on the proportions of a cliché.

Therefore, it can’t be recession because … they want this to happen.

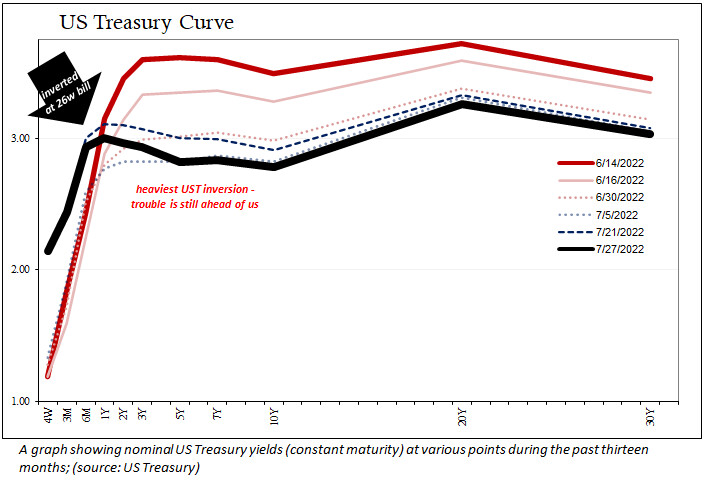

And that weight is tremendous. What we see from them we haven’t seen since 2007; in some cases, late 2007 after the first Global Financial Crisis had already begun.

The level of inversion in the yield curve like the eurodollar futures curve isn’t a product of any January to June “technical recession.” It sure can’t be some minor slowdown, the result Yellen or President Joe Biden’s administration is merely grasping for; Goldilocks showing up, shifting from a “too hot” economy while avoiding one that becomes “too cold” ending up just right and just right in time before the November midterms.

Our real problems remain in front of us.

By “us,” I don’t just mean Americans. This is a global downturn of uncertain proportions, but whose outline is more and more looking like some of the worst cases. Record low consumer and business sentiment in Germany and Europe. China using Zero-COVID to cover up Zero-Recovery and the increasingly authoritarian response to dissatisfaction with it.

On and on it goes.

For Americans, well, Walmart’s most recent more serious warning (press release update for second quarter and fiscal year) sums up their situation only too well:

“The increasing levels of food and fuel inflation are affecting how customers spend, and while we’ve made good progress clearing hardline categories, apparel in Walmart U.S. is requiring more markdown dollars. We’re now anticipating more pressure on general merchandise in the back half …”

This is a polite way of saying the same thing curves are pricing; they aren’t worried about what already took place.

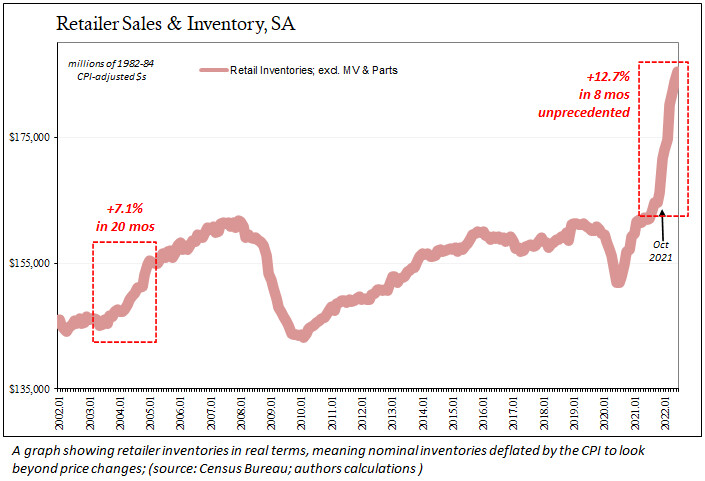

For retailers like Walmart or Target, they made the same mistake as Yellen. Each had confused high CPIs for robust recovery. Retailers went plain bonkers ordering goods entirely out of character and way beyond historical precedence. Blaming the supply chain bottlenecks, the real problem was economic forecasting.

These companies all reasoned they’d be perfectly fine in 2022 even if they had overdone it on goods during 2021. After all, mainstream econometric models all said that the good times were going to last well beyond the foreseeable future.

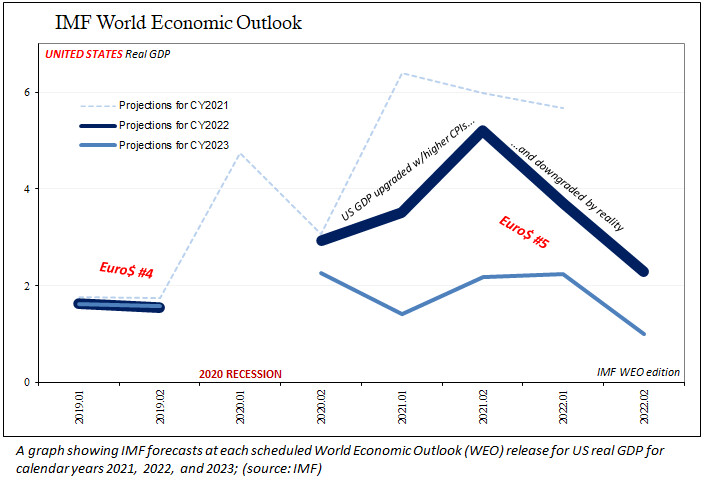

The IMF, for example, last summer thought U.S. real GDP growth for this calendar year would be better than 5 percent—and this was right around the time when Walmart and the others stepped up the order booking. No problem handling excess inventory if consumer spending was in for clear sailing.

A year later, the IMF now regrets to inform everyone its models were way, way too optimistic. Rather than 5 percent or better, now maybe 2 percent. While no small miss, the error can only have been a lot bigger.

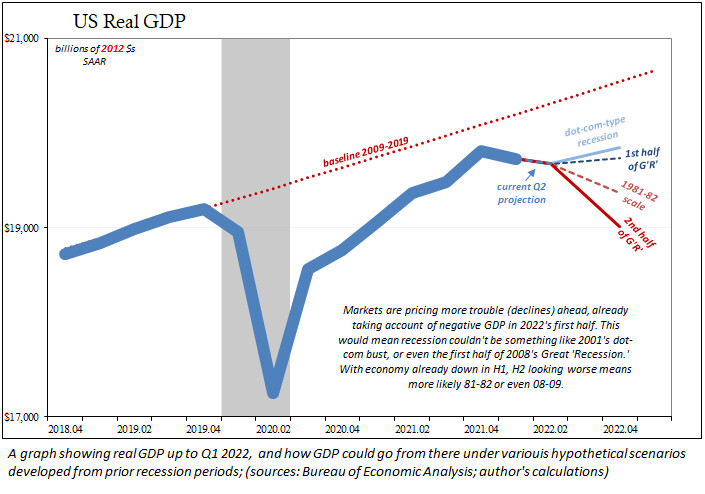

You might already be doing the simple arithmetic in your head, wondering just how the United States (like other places around the world) can even manage 2 percent when the entire first half of the year is almost certain to have been negative. The second half could only be something like the dot-com recession, meaning shallow decline and then much better from there.

Technical recession? Who cares, we’ve got much bigger problems.

Walmart and its peers are now reaching a panic because they know, and have already started to see, how all this actual economic math unrelated to Economists’ useless modeling truly must add up going forward from here.

The FOMC, for its part, remains steadfast as to the inflation story; a second straight 75-bps rate hike just to make a political point, to reinforce a narrative about cooling off from nuclear white-hot. It’s just no one is really buying it any longer. Not markets, nor, per the world’s largest retailer, consumers.