This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by copyright law. For non-personal use or to order multiple copies, please contact The Epoch Times Reprints.

What is wreaking so much havoc all over the world? You’ve probably heard that the U.S. dollar is rising often precipitously, which means any currencies caught on the other side of it—frankly, all of them—are being swept into crisis. This isn’t the first time, either, because during the last eight years or so this has happened repeatedly.

Typically, however, that has predictably meant emerging market economies (EMEs) are the ones who get singed. For example, Brazil’s real in 2015 or India’s rupee in 2022—those cause little notice. But the dollar has snared several big ones, from China’s yuan (for the third time since 2014) to Europe’s euro, even Britain’s suddenly dulled sterling.

This has been utterly confusing for several reasons, beginning with all the extremely loud voices warning about the dollar’s imminent collapse. The U.S. federal government allegedly conspired with the Federal Reserve in 2020 to “monetize” the former’s debts, which many claimed had unleashed the modern equivalent to the monetary conditions in Weimar Germany during the 1920s.

It was the same indictment leveled against the same counterparties the decade before, when quantitative easing (QE) had first combined with the gargantuan “stimulus” of the American Recovery and Reinvestment Act of 2009. Only, in this case, consumer prices finally did respond. But that just raises the question: What changed this time around? Neither QE nor the government, except by amount.

Set that aside, however, for a moment. While consumer prices accelerated, the dollar’s demise did not. On the contrary, apart from the latter half of 2020, the greenback has put back upon its seemingly inexplicable upward slope.

That is the thing here—the part to focus on—and from where we start piecing reality together from out of the fog of myths, legends, and Fed-inspired nonsense. When the dollar goes up, it doesn’t go well for anyone.

For one thing, the dollar’s increase correlates very nicely—meaning, not so nice—with several easily identifiable yet equally misunderstood issues. As a beginning, foreign governments end up selling their U.S. dollar reserve assets, primarily U.S. Treasuries, whenever the exchange value moves hard against their own.

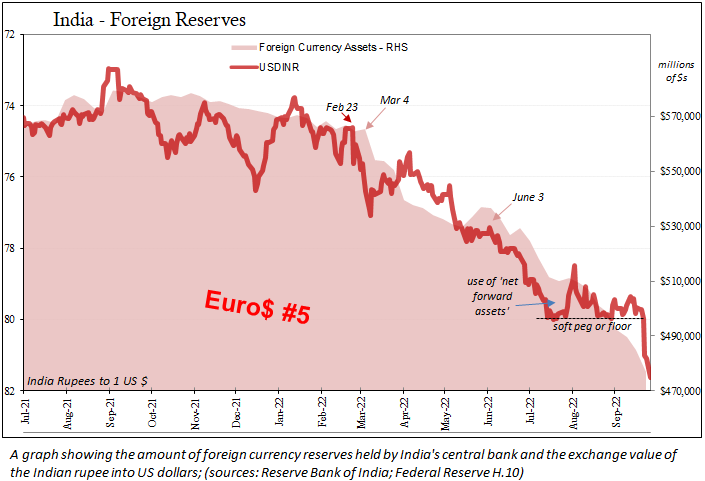

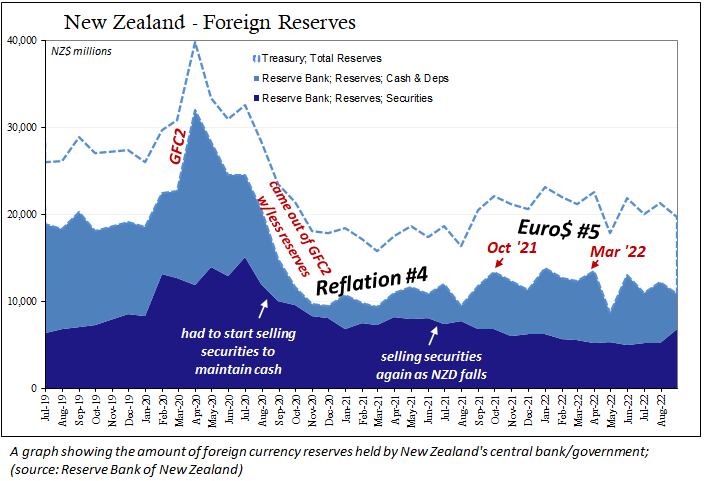

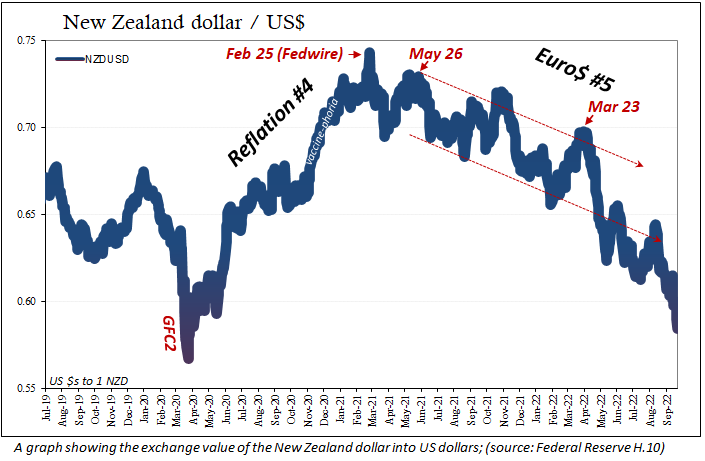

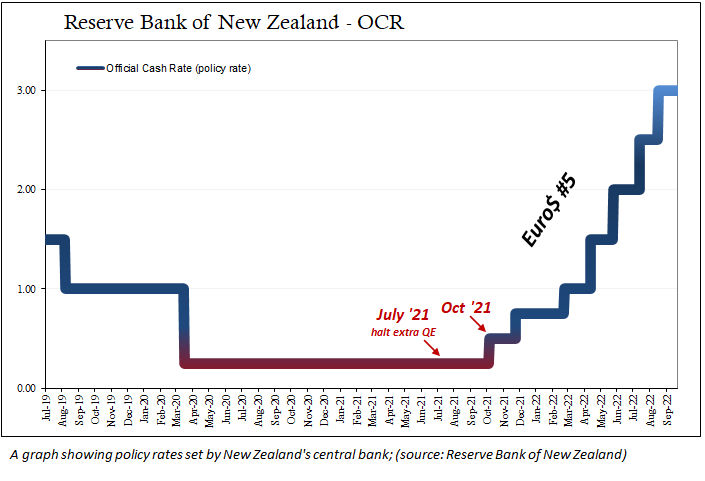

In fact, this has been the primary complaint from several of those currently being hammered. Officials from New Zealand to the Reserve Bank of India (RBI) have desperately tried to explain their plight to the rest of the world—only no one has been listening—everyone else instead has been caught up in awe of Fed rate hikes and quantitative tightening (QT).

At first glance, those do appear as if they are the world’s chief issue, including India’s. What RBI’s top policymaker Shaktikanta Das said, on Aug. 5, was, “EMEs are facing a rapid tightening of external financial conditions, capital outflows, currency depreciations, and reserve losses simultaneously.”

That is—rapid tightening of external financial conditions. Rapid.

The dollar goes up, signaling for the rest of the world “capital outflows, currency depreciations, and reserve losses”—each of those mere symptoms of that first dastardly first.

So, why not QT or rate hikes?

To begin with, the latter doesn’t matter much in this way, while the former doesn’t matter much in any way.

Take QT first—this is not (only) my judgement, by the way, it is, in fact, consistent with every bit of academic scholarship, any number of which have been produced by those doing the QT. A recent one from the Federal Reserve Bank of Atlanta, titled, “Working Paper 2022-08,” was published fortuitously right smack in the middle of our July to August to September dollar story which concluded:

“…I show that a passive roll-off of $2.2 trillion over three years is equivalent to an increase of 29 basis points in the current federal funds rate at normal times.”

Massively underwhelming, isn’t it? QT, like QE, is talked about as if it were the most powerful instrument ever invented and wielded by the enlightened class when QE as QT produces little more than a rounding error. Two-plus trillion dollars over three years does barely make a quarter-point rate hike.

Even making some conditional arguments (which are highly arguable), the study can only get it up to three-quarters of a percentage point under special circumstances. That’s it. Completely irrelevant.

So, no, QT cannot explain “rapid external tightening,” particularly given how little tightening anyone can associate with it, not to mention the fact that the current program was only recently begun and just last month ramped up.

So, then, rate hikes.

Except, no, it cannot be those, either. Again, you needn’t take my word for it. Establishment economist and current political barker Paul Krugman, in a New York Times op-ed, on Sept. 9, “Wonking Out: The Mysteries of the Almighty Dollar,” correctly (for once) observed that “... the Fed isn’t the only central bank hiking rates.” Most already were long before the Fed’s policy-making arm, the Federal Open Market Committee, voted its first rate hike back in March.

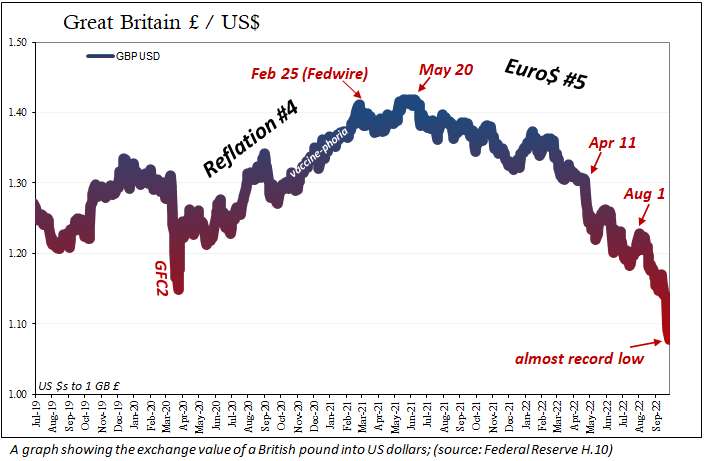

From New Zealand to, yes, the Bank of England, quite a list of overseas officials got the jump on the Fed, yet they’ve seen their currencies decimated anyway because we still need an explanation for “rapid external tightening” that cannot have been the usual suspect.

As Krugman wrote last month, there is something going on—going wrong—out there in the rest of the world, offshore, where dollars used to go freely.

Another word for offshore dollar is eurodollar.

All the warning signs related to that have been pointing in just this direction all year; even before this year, when—get this—the eurodollar futures curve had first inverted way back last December, long before Fed rate hikes, let alone any aggressive set of them, was on anyone’s mind.

What does rapid eurodollar tightening end up looking like? Let’s go back to India one more time:

“EMEs are experiencing capital outflows and reserve losses which are exacerbating risks to their growth and financial stability.”

EMEs, sure, but where have risks to growth and financial stability already become an admission over recession along with monstrous financial instability most recently?

In Britain—yes, Britain.

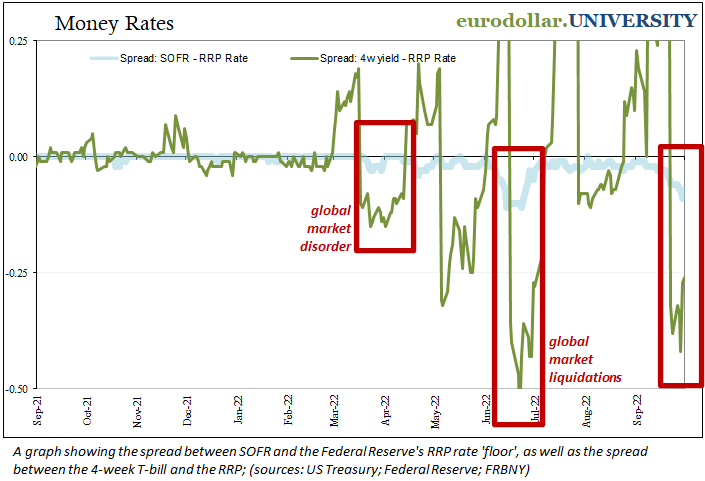

All the eurodollar signals that had forewarned what we’ve already seen—and nobody in the mainstream can explain—have taken it a step further again recently. Primary among these, as I write constantly, collateral scarcity creating, one more time, rapid external tightening.

T-bill (and repo, therefore, SOFR) rates at the end of last month, and to start this month, have become once again grotesquely alarming (meaning, low). (SOFR is the secured overnight financing rate, which replaced the London interbank offered rate, or LIBOR, in the United States.)

If this has gone so far as to reach and devastate financial London, once the very epicenter of the eurodollar system, not only do we care little about QT or the Fed’s rate hikes, we’re left both in awe of the dollar’s further potential rise and even more worried about what next it will cause.

Whether anyone can adequately explain it or not, the eurodollar is what happens, and will continue to happen, anyway.

Jeff Snider is Chief Strategist for Atlas Financial and co-host of the popular Eurodollar University podcast. Jeff is one of the foremost experts on the global monetary system, specifically the Eurodollar reserve currency system and its grossly misunderstood intricacies and inner workings, in particular repo/securities lending markets.