Because everything nowadays is, it seems, little more than a game of partisan football, whatever one side does, the other reflexively denounces it before giving it a second thought. Common sense is cast aside in the almost all-out war of narratives, a fact proven repeatedly during the pandemic.

Now as that debacle finally fades from the front pages of mainstream attention, it has been replaced by a different sort of disease, another one which neither can be easily diagnosed nor treated—that is, inflation.

The Republican side rushes to pin every last added penny on their Democrat counterparts, while the latter seek out each minuscule fractional percentage-point drop as proof the former has it all wrong. An argument performed in raw numbers.

As any rational, dispassionate observer likely will tell you, numbers devoid of context are meaningless—which is their political purpose.

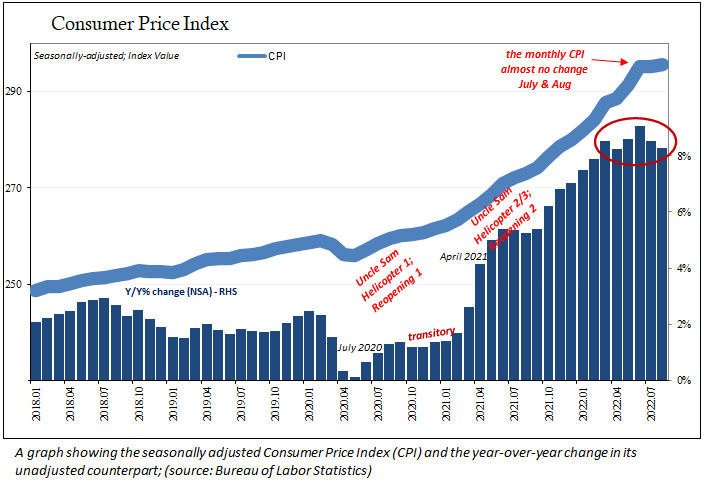

President Joe Biden quickly declared success upon release of the August 2022 CPI estimates. He was just as swiftly mocked by the other side for doing so. Biden had merely—and correctly—pointed out that, according to the latest figures from the Bureau of Labor Statistics (BLS), the headline (full consumer price bucket) estimate has been basically flat for two months in a row (July, then August).

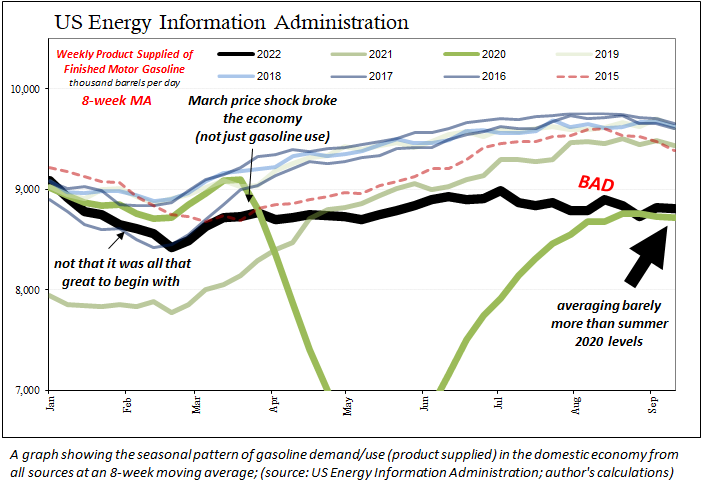

Sure, opponents conceded, while true, the annual rate still ended up being “hotter” than anyone had expected. Gasoline costs also fell during those months, the primary reason the CPI was flat in the first place; but other prices have risen to offset the less painful pump prices.

And here is where the context, and the politicking, gets turned upside down. Republicans are warning about more underlying inflation when there isn’t. Democrats are seeking credit for some real reduction in price pressures they’ll soon wish they hadn’t.

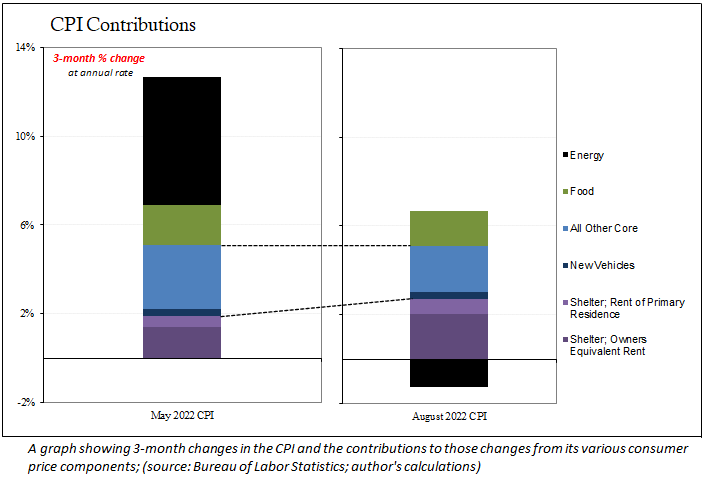

Compare the results in the CPI components in three-month intervals; first, the big surge in March through May, then what happened afterward during June to the end of August. No special training is required to appreciate just how much the situation has changed in a very short period of time.

We all know, or should, the story behind energy prices. And it is not a good one, even as prices have reversed from recent burdensome highs, which were unwisely induced by supply constraints. Since mid-June, oil has come partway back down, even though output hasn’t improved; meaning, demand has changed dramatically.

When there is weak demand and too much inventory, prices have to be adjusted downward.

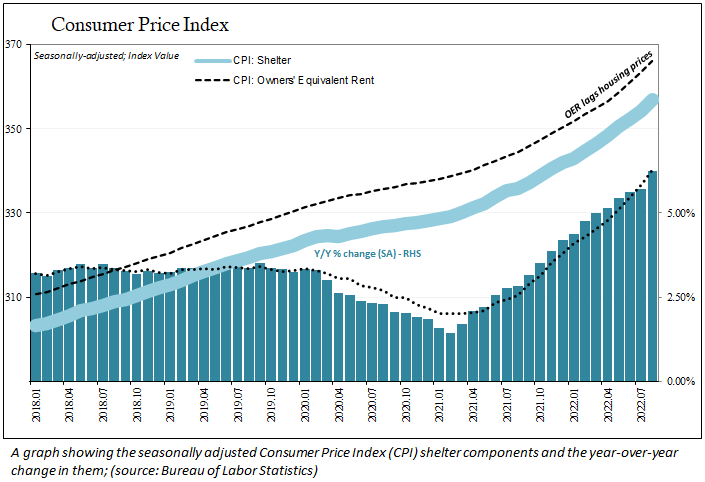

What instead contributed to the “miss” to expectations for the core CPI, in particular, was how the index accounts for rent and shelter. Nearly a quarter of the whole consumer bucket consists of something called owners’ equivalent rent (OER).

While goods prices right now are being marked down due to a slowing maybe recessionary real economy, the CPI is being “supported” by long outdated results which have no bearing on today’s situation.

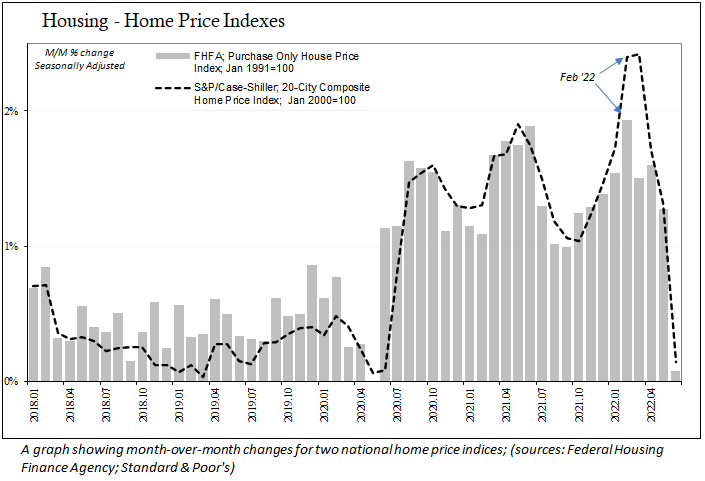

Even home prices finally stopped rising so precipitously just recently, as with crude oil, around June. The way the CPI is pieced together, though, means this part of the measure won’t slow down for quite some many months ahead, regardless of how the economy is doing.

In the end, it may not matter. The economy is in a downturn, and the most serious threat to it comes from labor, not inflation.

To that end, after having conducted a survey of 5,618 small-business employers from Aug. 13, 2022, through Sept. 6, 2022, research firm Alignable found:

“… the demand for labor has declined again, with nearly two out of every three (63 percent) putting their hiring on hold because they can’t afford to add staff, and 10 percent of that group is laying off workers.”

These numbers have become materially worse in just the past few months—the same, you’ll note, as when trends changed within the CPI.

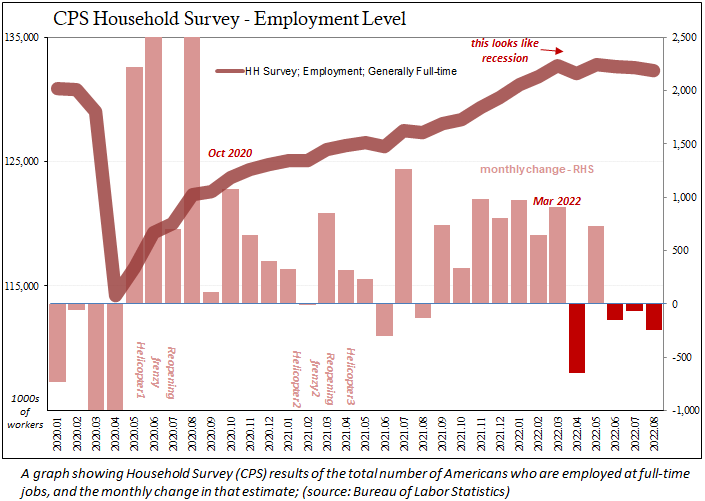

This jobs uncertainty has already shown up in major government employment data. While the BLS’s Establishment Survey has slowed, the Household Survey’s track of employment growth has largely come to a halt, consistent with what Alignable found. Worse, many employers appear to already be taking proactive cost-cutting measures, having already reduced hundreds of thousands of full-time positions to part-time.

Any lingering “inflation” Republicans claim must be getting worse is at most from last year. The very real and current improvement for consumer prices is in every likelihood the increasingly palpable onset of recession.