It was barely a month ago when OPEC+, the group of major oil-exporting nations, had announced a small increase in production. The world economy was suffering under extreme oil price pressure. President Joe Biden traveled to Saudi Arabia, one of OPEC’s largest producing members, to personally deliver his plea for relief on behalf of pretty much everyone. All he extracted from the Saudis was a measly increase of 100,000 barrel per day (bpd).

Partisan politics aside, the reason Biden didn’t get any more than this symbolic gesture was widespread concern on the part of producers over the same economy. Fears of recession have been growing for good reason, as oil prices swing wildly, unsettling the market.

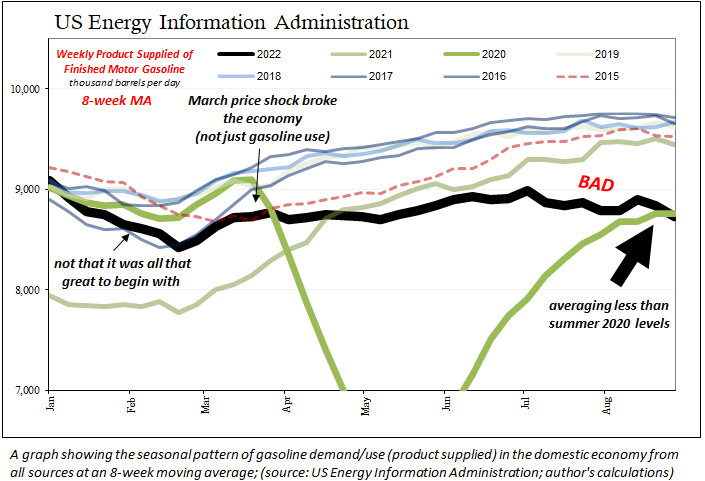

We see this very clearly, as I wrote in my last column, in the reshaping of the domestic oil futures market curve. Gasoline use (demand) domestically is thought (by the government) to be right now, on average, as dismal as it had been during the summer of 2020, when much of the country was still unwisely imprisoned by pandemic politics.

While this is relatively straightforward, recession isn’t the only factor weighing on this curve and many others.

Crude oil futures are the nexus between the real world and the monetary, the physical needs of supply balancing demand set against global liquidity. What had sent oil prices surging originally from 2020 was entirely supply related—that is, too little of it. Since around February and March 2022, the balance (or imbalance) has flipped, though not just toward demand fears.

Shouldn’t the president have visited Federal Reserve Chairman Jerome Powell instead of the Saudi crown prince?

Had Biden done so, it would’ve been just as much a waste of everyone’s time. By mainstream convention, we’re told that if something happens in markets or the economy, the Federal Reserve must be behind it. This “don’t fight the Fed” myth persists, despite decades of experience having long ago overthrown it (in fact, the myth was never really established by anything apart from unsubstantiated claims, including those for quantitative easing).

But like OPEC’s brief production increase, rate hikes are just as symbolic (and still heavily priced to be brief). Effective monetary tightening is just not something the Federal Reserve actually does. Instead, we can easily establish the real U.S. money conditions punishing the WTI curve by starting in … Italy.

Unbeknownst to most people, which includes those working at the Fed or European Central Bank (ECB), Italian governments are a huge source of useful currency for the entire global system. How do bonds become currency? As collateral in all kinds of monetary transactions, from repos to derivatives to collateral-for-collateral swaps and transformations.

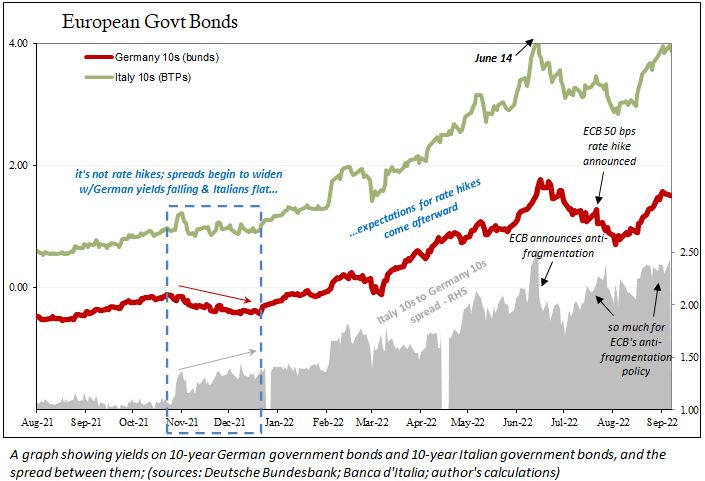

In short, since the Germans are notorious for being fiscally prudent, there just isn’t a lot of “pristine” German government bonds issued, particularly of the short-run maturities coveted by global money participants engaging in securities financing transactions. As a result, the fiscally profligate Italian government has, sadly, filled this crucial monetary void.

This, of course, introduces a potential fracture point—the same exact one which had already been the primary source of the second global monetary crisis more than a decade ago, in 2010 and 2011. Any real prospect for recession in Europe is a bad combination, with Italian bonds already trading on shaky grounds because the Italian economy never recovers from any of the previous contractions.

Growing concerns about Italy’s situation, which always features an unhealthy dose of related political instability, spill right over into volatility in Italian bonds. There is nothing collateral-takers in repos despise more than price volatility and uncertainty. We can see this pressure rising in the dangerously growing spread between Italian bonds and their German counterparts.

The ECB, aware of at least the politics surrounding Italy’s precarious position, promised more than two months ago to do something about it. Announcing a frankly ridiculous “anti-fragmentation” idea (to buy more Italian bonds while selling German bonds, theoretically narrowing the spread between them, it quickly lost favor in the marketplace because it was the usual central banking nonsense (which the financial media ate right up, the policy’s true aim).

Despite the ECB’s promise, or because it isn’t a useful solution, Italian spreads are once more blowing out.

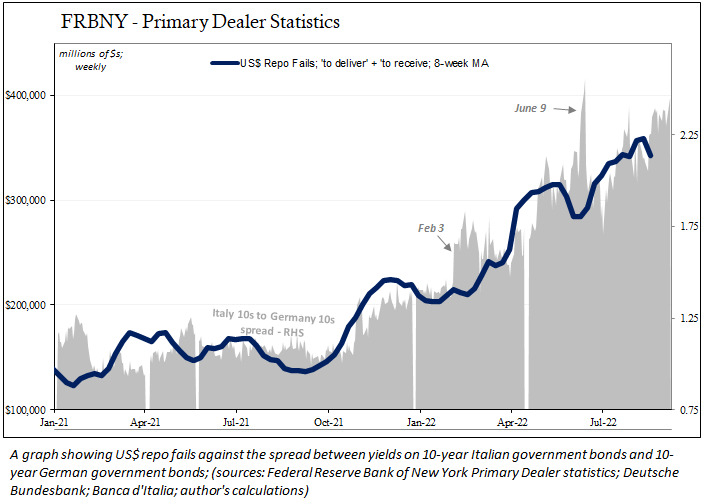

Thus, as Italian government spreads surge, this instability forces the system to scramble for other forms of more usable collateral, creating an imbalance in demand for alternatives, such as U.S. Treasuries, to the point that it leads to more and more of those repo failures.

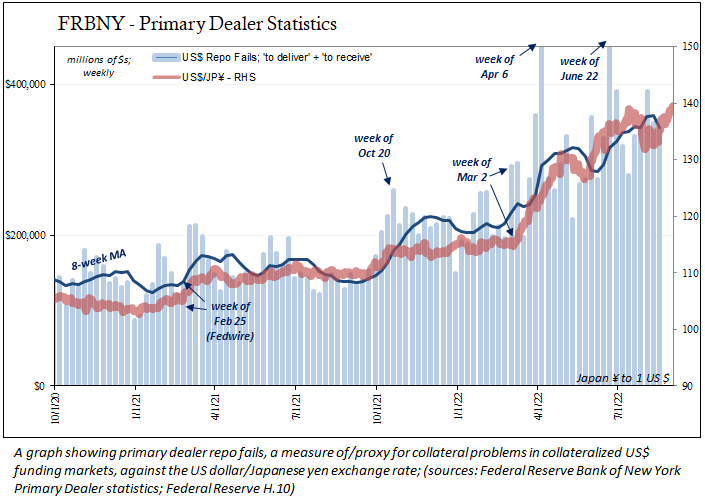

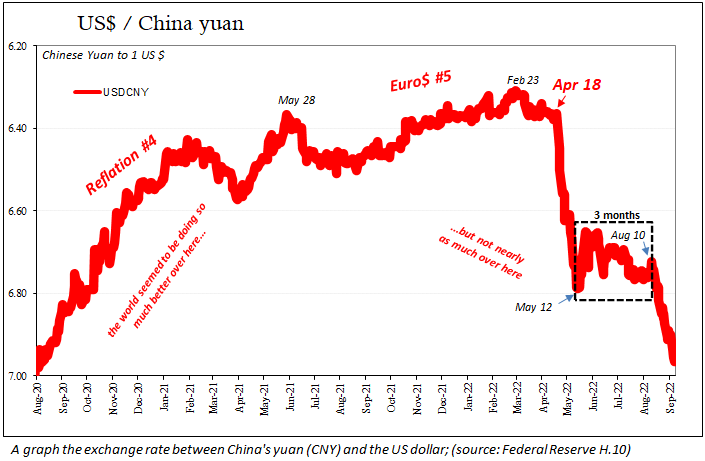

As the collateral squeeze spreads, it also leads to the more visible warning signs of dangerously tightening global money supplies—a rising U.S. dollar exchange value (also incorrectly assumed to be a result of whatever the Fed is doing). With the dollar having surged to multi-decade highs against many major currencies, this is actually a systemic monetary warning!

In that respect, OPEC+ and the Fed, the president or any politician, are all running around merely pretending to have a clue.