We have all been taught to associate low money rates with stimulus, and especially high money rates with trouble. And that can be true under certain circumstances. This theoretical world of easy interpretation doesn’t exist outside of the media or central bank econometric models.

History—even recent history—at the very least cautions for a more nuanced approach.

Take, for example, the situation in December 2007 when the Federal Reserve, under the leadership of its still-relatively new Chairman Ben Bernanke, began to figure out subprime wasn’t contained (because it wasn’t about subprime). After the clear breakdown on Aug. 9, the Federal Open Market Committee (FOMC) had simply followed its instruction manual: August (primary credit), then September (federal funds target) rate cuts, and a clear “message” for more “aid” in the form of same going forward.

Over the subsequent weeks, chaos in the monetary world only became worse. Bernanke’s group of policymakers were compelled to take steps our pre-crisis selves never imagined any Federal Reserve regime would ever take.

Instead, the TAF auction was initially (and continually) swamped by “U.S. banks” with mostly German names (U.S.-based subsidiaries of foreign mainly German parents). Add to that overseas flavor the obvious offshore nature of overseas dollar swaps, and if you had been paying any attention you would have very quickly realized how this was a global dollar panic (eurodollar) unlike what’s taught in quaint, outdated textbook theories.

The day after that, Dec. 19, EFF would drop another 18 basis points (bps), falling under 4 percent.

Wasn’t that just the TAF auctions pouring major amounts ($20 billion) of cash and liquidity into these markets?

And it wasn’t just an issue for federal funds. Repo rates such as that for GC repo (or general collateral, meaning a secured or collateralized short-term interbank funding arrangement using essentially generic U.S. Treasury securities as the collateral) would often plunge dramatically more than EFF.

The same is true in repo: if there aren’t enough interbank borrowers with acceptable collateral, cash lenders will resort to accepting much lower rates from those borrowers who can post good collateral, which most often means U.S. Treasuries, likewise explaining the same behavior found of GC repo.

No matter what the Federal Reserve would try, nothing stemmed the disaster. Right from the start of Aug. 9, 2007, all the way through to the actual end of the monetary panic in March 2009, you can plainly observe (in the chart above) how there was nothing other than absolutely obvious chaos and disorder, more often than not (the London interbank offered rate [LIBOR] was the notable exception, for reasons I won’t get into today) presented in the form of low money rates (including T-bills, for direct collateral purposes).

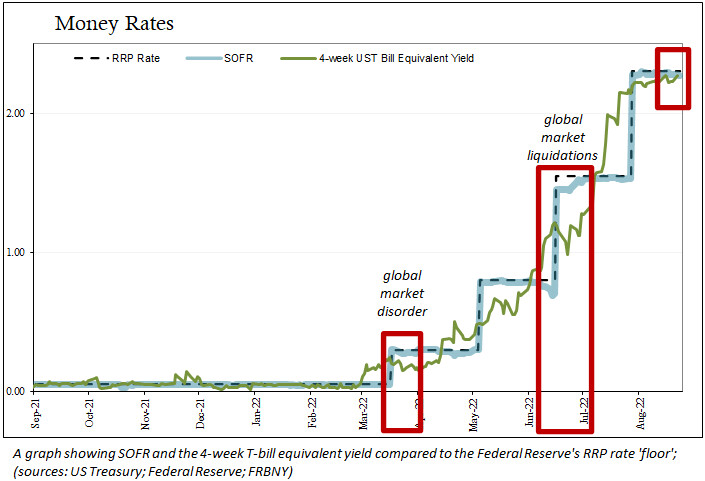

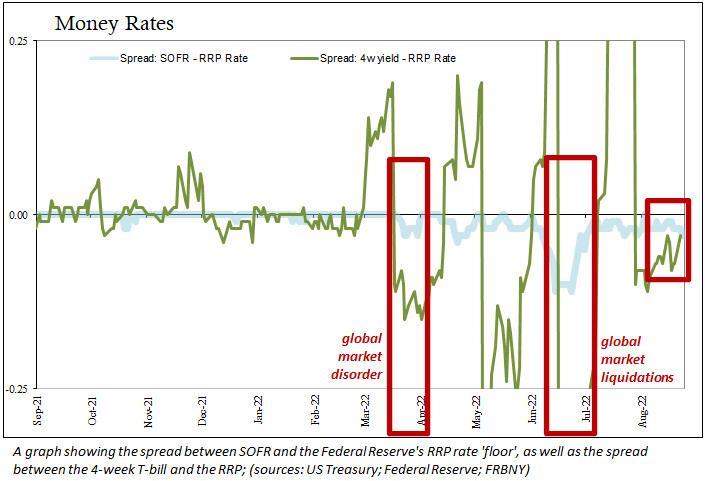

As of Aug. 24, 2022, the GC repo rate (or broad general collateral, as it’s now known) stood at 2.26 percent. Another repo-heavy interest number, the secured overnight financing rate (SOFR), which encompasses a wider volume of repo funding, was put at 2.27 percent. Yields on four-week Treasury bills were thought to tally up at 2.29 percent, having been much, much lower in recent days.

All of those are less than the Federal Reserve’s so-called “floor,” the reverse repo rate (the way the Fed claims to manage money markets has been changed since 2008, no longer picking a single target as it had for decades up to its grand failures during the crisis), which currently stands at 2.30 percent. Even EFF, on Aug. 24, was barely 2 bps above it.

In recent months SOFR, repo, and T-bills have been much further below the Fed’s “floor” than now. And when they’ve been that low, that’s also when we’ve experienced gross illiquidity and bedlam in global markets, such as occurred in mid-March and especially mid-June.

These falling money rates weren’t “stimulus,” nor did they have much to do with the Federal Reserve at all. Similar to the conditions in 2007 and 2008, they describe a very different situation from the rationale of “inflation is because too much money printing” that is widely accepted across the entire mainstream media (the same media which had prematurely congratulated Ben Bernanke for every ineffective gesture). Money markets are again behaving erratically in a way that favors no one.

And that would be bad.