In February, the S&P 500 Index was at 4,500. With the corporate bond rate of 3 percent, my analysis showed the fundamental value of the S&P 500 was 4,100; stocks were 10 percent overvalued. The article cited that I and many other economists expected interest rates to go higher. As higher interest rates lower the value of stocks, the article concluded that at interest rates of 4 percent, it would reduce the value of the S&P 500 to 3,900.

My conclusion was that at 4,500, the S&P 500 was not only 10 percent overvalued but also that if there were an increase of interest rates to 4 percent it would raise the overvaluation to 15 percent. Hence, investors should have been cautious about holding stocks.

Much has changed over the past seven months. Russia invaded Ukraine, inflation soared, corporate bond rates increased to 4.5 percent, and the S&P 500 lost 500 points, to 4,000. Most stock portfolios are down more than 10 percent, close to the level anticipated by the increase in interest rates.

Of course, many things can affect stock prices. Even so, two things—earnings and interest rates—are so fundamental to valuing stocks, they deserve close attention before anyone should consider investing in stocks.

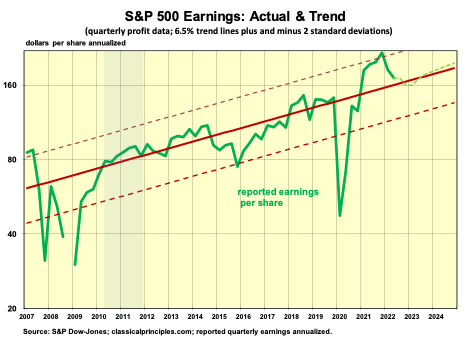

Understanding the longer-term trends in earnings and interest rates are very useful in determining the fundamental value of stocks. Looking first at the earnings trend for S&P 500 companies reveals an interesting phenomenon. Since 1947, the average yearly increase in earnings has been 6.5 percent. Actual earnings have moved frequently above and below this average, with a strong tendency to gravitate back to the trend line.

The middle trend line in the following chart shows the S&P 500 long-term earnings trend has increased by 6.5 percent annually since 1947; the green line shows annualized reported earnings for the S&P 500 companies. The important thing to note is how earnings eventually gravitate back to the trend whenever they are above or below the trend.

One solution is to observe where earnings are relative to their longer-term trend. Since this trend has survived vastly different periods of political and economic turmoil, it appears to be driven by powerful economic forces. If so, this longer-term earnings growth can often provide a reliable guide to estimating the likely direction of future earnings, particularly if earnings are well above or well below their longer-term trend.

Earlier this year, the latest earnings data showed fourth-quarter earnings were 40 percent above their longer-term trend. At that time, my conclusion was that it was more likely profits would be flat to down, placing downward pressure on stock prices, which is what happened. For the first two quarters of 2022, earnings declined by 21 percent. By the second quarter, earnings were only 6 percent above their longer-term trend. In a sense, this is good news. When earnings are close to their longer-term trend, it can be easier for companies to avoid a serious downturn.

In addition to earnings, interest rates are important in valuing stocks. Financial asset theory tells us the value of stocks depends on future earnings discounted by the appropriate interest rate. While the formula is complicated, the relationship is not. Simply, when interest rates are low, the value of corporate earnings are worth much more than when interest rates are high.

Hence, when the interest rate on bonds is 3 percent, the earnings from stocks are worth far more than when interest rates are at 4 percent or 5 percent. This relationship allows us to use interest rates to adjust the impact of earnings in determining the fundamental value of stocks.

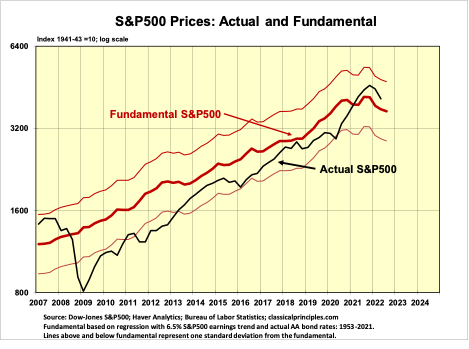

In the chart below, the fundamental value of the S&P 500 is determined by a regression analysis. The price of the S&P 500 is the dependent variable and the longer-term earnings trend and current corporate bond rates are independent variables. The fundamental value of the S&P 500 can then be generated and compared to the actual S&P 500 Index to estimate the extent to stock prices are above or below fundamental value.

The most significant recent overvaluation occurred in 2007, just prior to the financial crisis. At that point, those buying stocks paid 25 percent more than their fair value. In the aftermath of the financial crisis in 2008–09, the S&P 500 companies were selling for almost half their estimated value!

Since late 2008, the Federal Reserve has held interest rates artificially low in an effort to stimulate the economy. In doing so, the Fed artificially increased the value of corporate earnings as well as the value of stocks. Artificially low interest rates punish savers while benefiting debtors and stockholders.

Following losses during the financial crisis, investors were slow to realize the increase in the value of stocks as the economy recovered. Though stocks were often selling for 20 percent less than their value, investors were reluctant to believe it. Stock prices remained below value until the beginning of 2021. After more than a decade of rising stock prices, investors finally became comfortable paying higher prices for stocks.

With the S&P 500 Index currently in the vicinity of 4,000 and corporate bond rates at 4.5 percent, the index is 7 percent above its fundamental value of 3,700. The next move in stocks fundamental value is highly dependent on interest rates. If corporate bond rates remain at current levels, the increase in the long-term earnings trend will gradually raise the value of stocks to 4,000 by the end of 2023.

However, any increase in bond rates will lower the fundamental value of stocks. For example, if the corporate bond rate were to move from 4.5 percent to 5.5 percent, the fundamental value of stocks would decline to 3,600.

This analysis of fundamental value highlights the importance interest rates can have on the value of stocks. As the Fed proceeds with its intention to raise interest rates and take money out of the system, it is likely interest rates will go still higher, thereby reducing the fundamental value of stocks.

In spite of recent encouraging signs of an upward move in stock prices, our fundamental analysis points to potential problems for stocks in the months ahead.