According to the economist Thomas Sowell, “The first lesson in economics is scarcity. There isn’t enough to satisfy everyone. The first lesson in politics is to ignore the first lesson in economics.”

For decades, many complained about the rising national debt. Yet, Congress continues to vote for spending that far exceeds tax receipts. Over the last four years, this pattern has become as bad as ever.

How bad is it?

In 2019, amid a booming economy, federal spending exceeded tax receipts by almost $1 trillion. This brought the nation’s publicly held debt to $16.8 trillion. As bad as these numbers were, during the past four years the United States added another $9 trillion in national debt. This year government will add another $1.5 trillion, or more:

Of the $9 trillion in deficits since 2019, $3.9 trillion was paid for by the Federal Reserve buying the debt. This sent soaring the money supply, spending, and inflation. This portion of the debt was paid in the form of higher prices for everyone.

The remaining $5 trillion, along with the compounding effects of interest payments, was paid for in the form of reduced private investment as Treasury purchases crowded out private sources of debt.

By the end of 2023, the $9 trillion additional debt will bring the nation’s publicly held debt to over $26 trillion. I estimate another deficit of $1.6 trillion, along with interest costs of 5 percent will increase the nation’s debt to $28 trillion by the end of the current fiscal year.

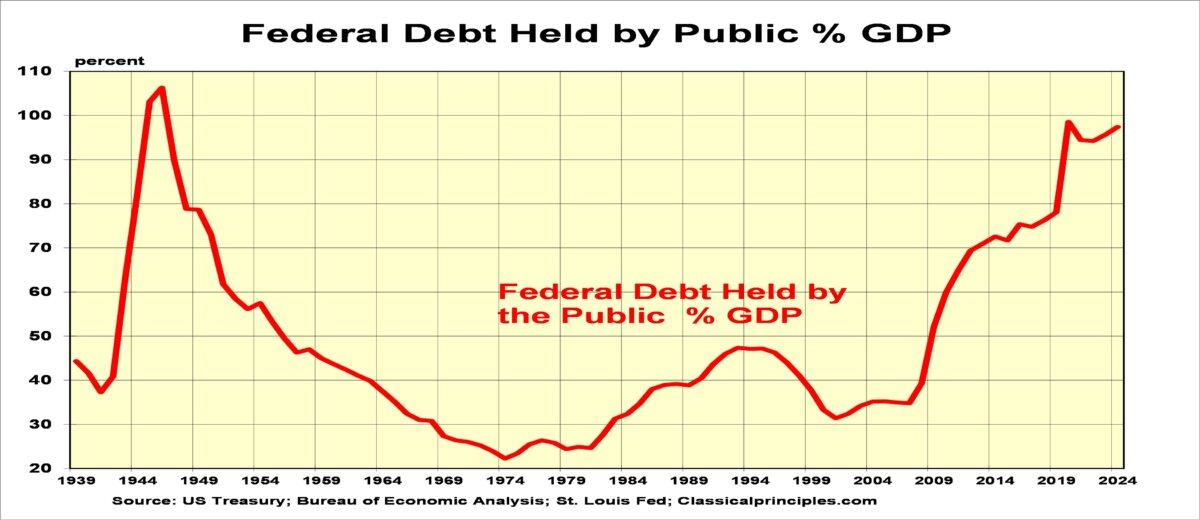

The appropriate way to view the nation’s debt is to look at it relative to the nation’s output. The following chart puts these numbers into perspective. It shows how the debt reached over a 100 percent of a year’s output during World War II, and then declined sharply amid constraints on federal spending.

Implications of Debt Equaling Close to a Year’s Output

Debt is neither good nor bad. Its impact depends on the details of how and why the debt was incurred. World War II debt was associated with funding a war to secure freedom. Once the war ended, the victory secured decades of freedom and growth. The war debt was paid down during the 1950s and 1960s. The paydown came not from budget surpluses but rather from slower growth in federal spending, which provided more resources for a rapidly growing private economy.The debt buildup during President Ronald Reagan’s time in office was a similar case. A combination of tax cuts and military spending had a twofold effect. The tax cuts spurred growth in the private economy while the buildup in U.S. military spending led to the collapse of the Soviet Union’s economy and the dissolution of the Soviet Union. The result was more than a decade of world peace.

Increasing federal debt for clearly defined programs that enhance peace and productivity can be worthwhile. Since 2008, most of the increase in the nation’s deficits and debt has been driven by poorly designed programs which increased federal spending and placed barriers to growth and prosperity.

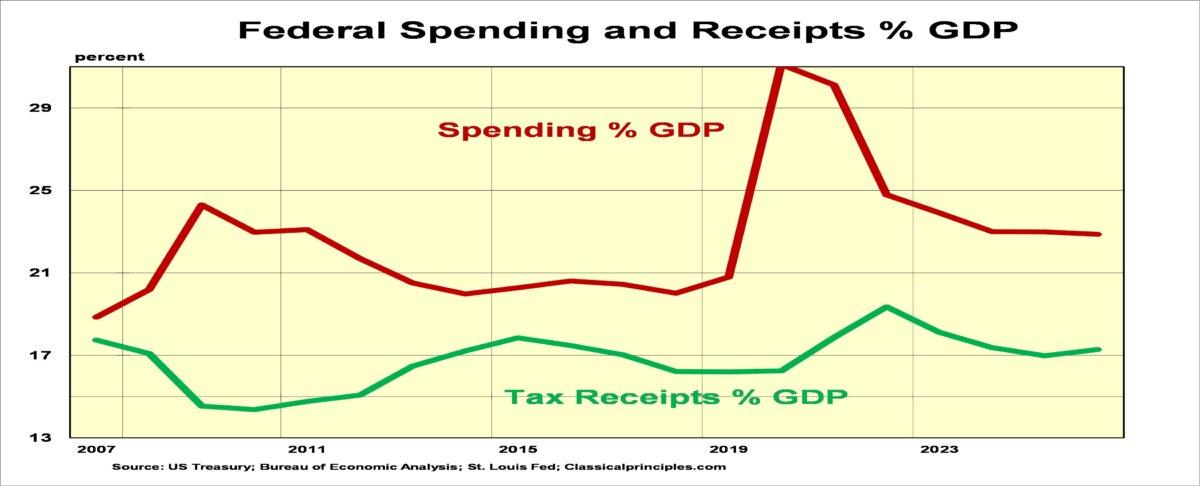

From 1952 to 2007, federal spending averaged 19 percent of GDP while tax receipts averaged 17 percent. Since 2007, federal spending has averaged 22.5 percent of GDP and tax receipts remained at 17 percent.

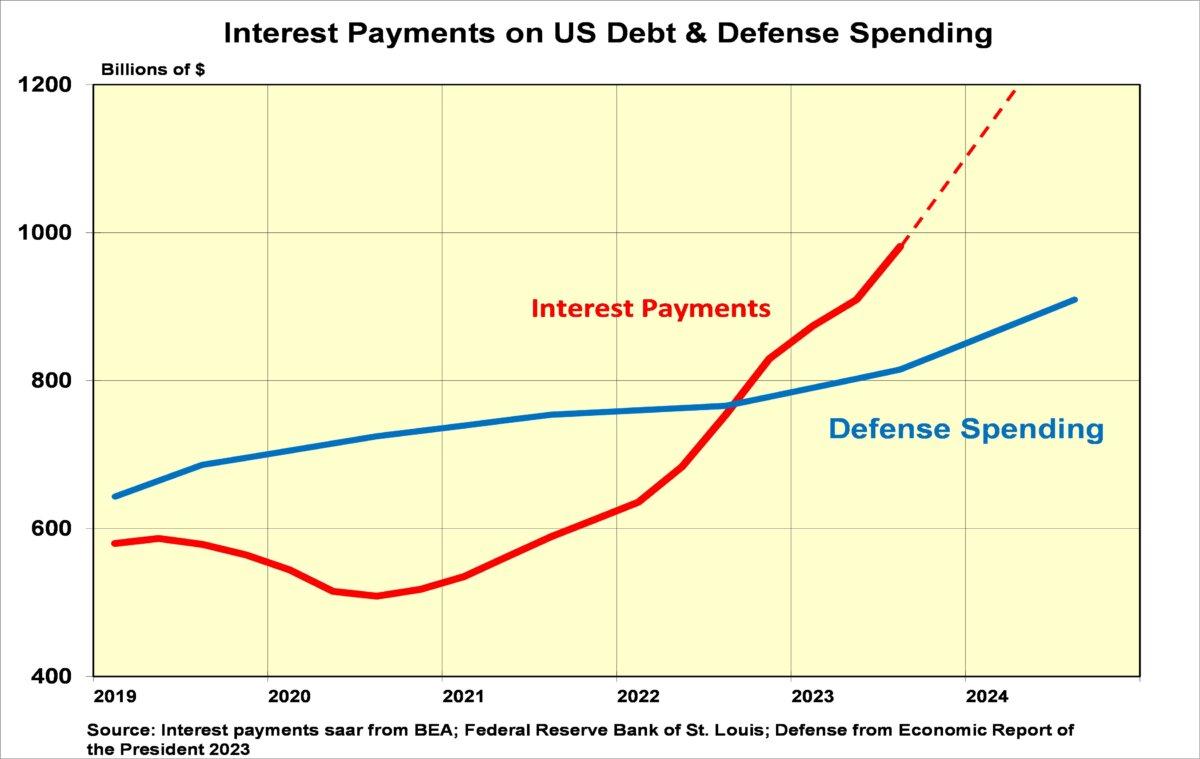

The massive buildup in red ink over the past four years has depleted funds for future government programs. As debt spirals out of control, interest payments have become a progressively larger portion of spending. As the following chart shows, interest costs on the debt exceeded the entire defense budget late last year. This year, the combination of another $1.6 trillion deficit and higher interest on the debt will makes interest payments the third largest component of federal spending, behind Social Security and Medicare.

Economic Implications and Solutions

A legacy of irresponsible bipartisan policies has placed our government’s finances in a similar position to those who have maxed out their credit cards. What seem to be obvious solutions—a massive tax increase and cuts in Social Security—also would be destructive. History indicates that tax increases undermine the economy and actually reduce tax receipts and increase deficits.When the tax cuts of 2018 took effect, federal tax receipts were 16.2 percent of GDP. By 2022, lower tax rates increased tax receipts to 19.4 percent of the economy. This past year, amid tax increases from the so-called Inflation Reduction Act, tax receipts fell to 18 percent of GDP. The Congressional Budget Office (CBO) consistently forecasts higher taxes increase tax receipts. History clearly shows the CBO has been consistently wrong.

Since tax increases make deficits and debt worse, the only solution is to contain federal spending. Cutting promised benefits, such as Social Security, is simply a recognition of bankruptcy by failing to make good on promised commitments to workers. We can do better.

As in the 1950s, any workable solution must enable the economy to grow faster than the growth in federal spending.

Given the magnitude of our current budget problems, policymakers should consider “thinking out of the box” for creative solutions. Congress could apply a cost/benefit analysis to all federal functions and eliminate those where costs exceed benefits.

Another solution could involve reform on our country’s inefficient healthcare system, which spends twice as much as countries with far more efficient approaches. The potential for saving trillions of dollars in healthcare costs would significantly reduce federal healthcare expenses, the largest budget item after interest expense.

Still other creative solutions would deal with our convoluted tax collection system. Currently, the system intrudes on privacy and inhibits saving and investment. Replacing the nation’s income tax with a single flat tax on all spending, such as the Fair Tax Act of 2023, would enhance privacy, contain federal spending, and promote saving and investment. Still another solution would privatize Social Security through the type of an Own America Account, as proposed by Jeff Yass and Stephen Moore.

Current federal deficits and debt are serious problems, but there are solutions. Federal spending can be contained. Solutions involve making use of America’s greatest strength—the private, free-market economy and proper incentives to make the cost of government more transparent. These incentives are what once made our economy strong and successful. They remain the keys to reducing federal spending and promoting liberty and prosperity for all.