First Britain, now Switzerland. The United Kingdom’s massive fiscal mess has made all the news, capturing the world’s attention for its sudden descent into drama more typical of undeveloped countries. London hadn’t always been the clean money center it now projects in recent decades. The pound had experienced almost frequent problems under the previous “controlled” socialisms during the 1950s and 1960s.

Forgotten to history is the fact that Britain was actually bailed out by the International Monetary Fund (IMF) in 1976.

Why? All the familiar surface features. In one particularly damning, almost comical, government document prepared for Prime Minister James Callaghan’s cabinet, uncovered many years later, it was revealed that the government, the Bank of England, and all the queen’s horses and men couldn’t get close to saving the pound.

The document pointed to the need to lower rate of price inflation down to at least 15 percent. That target would require a major effort to get the average wage increase below 20 percent early in the next wage round. It was therefore suggested that a more reasonable target would be a wage norm of 15 percent.

Since the government ran most of the major industries, the pre-Margaret Thatcher Parliament was the country’s largest employer, too. A “wage norm of 15 percent” was pure mockery—the sort of half-baked thinking typical of academia (or of socialists) rather than real economy practice.

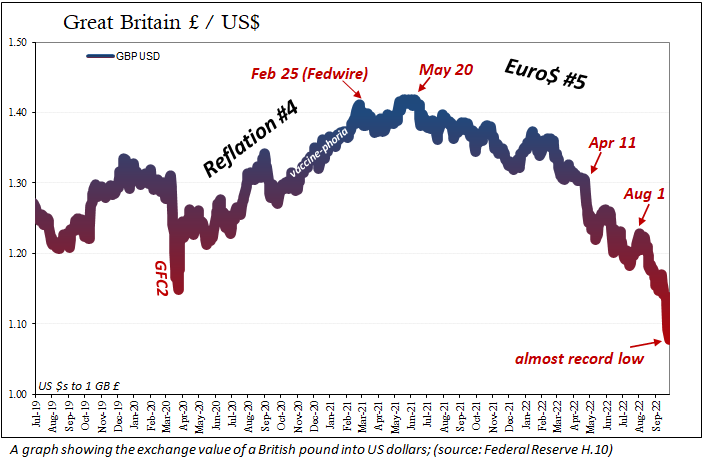

Britain was falling asunder, and the world’s money wasn’t going to stick around for the inevitable fall to get London back under common sense. If the pound could fetch only $2 by March 1976, by October it was down under $1.65.

To aid in the growing chaos, the Bank of England leaned heavily on foreign imports of cash. Except that it was not “real” cash—no one actually uses that stuff and hasn’t for over a century. Instead, swaps were used—in other words, book entries on account of these various official entities.

The Federal Reserve Bank of New York, along with the U.S. Treasury, offered a combined $2 billion to aid the Bank of England’s rescue of the sterling. An additional $3.2 billion was secured from the Group of Ten nations (minus Italy), plus Switzerland, dragging the Bank for International Settlements into the affair. Back then, $5 billion-plus was a princely sum.

These swaps, however, came with an expiration; they weren’t gifts or grants, therefore they required repayment. Those originating from America would come due in just three months, a single quarter by which the British government had to get its fiscal, employment, and inflation affairs in order. Or, more realistically, come up with some plausible roadmap no matter how painful.

You don’t need to guess how that worked out.

Instead, the swaps matured, the book entry cash repaid, the international capital flight resumed, so that before the end of 1976 the United Kingdom had to be, embarrassingly, bailed out by the IMF. As had become its standard practice, that supranational group demanded harsh concessions for its salvation, one of the largest (scaled for the time) in history.

Capital loathes instability, and nowhere more so than wherever corrective action is deemed the most unlikely. Britain was hardly alone in its 1970s’-era predicament; throughout the latter half of that decade, several countries faced monetary crises of similar or worse magnitudes.

Being lumped together with what were all otherwise emerging market nations wasn’t just a blow to British pride, it was a measure of how serious those times had become.

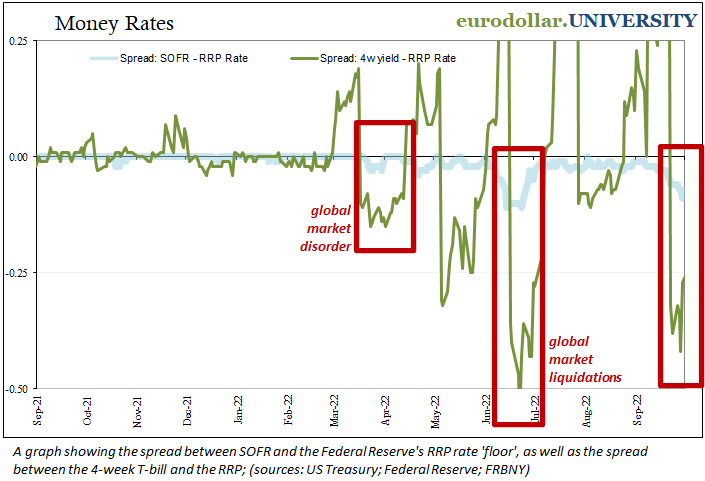

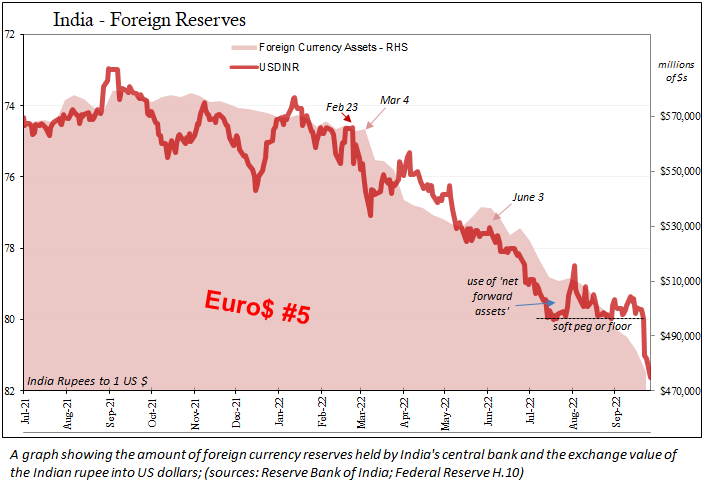

If it all sounds familiar to our own ears, it’s not the part about inflation or wage expansion but rather the monetary flight from the unstable. In fact, the evasion has become more prevalent recently than it has been since maybe 2008 (at least 2020).

I’ve written about this shortage repeatedly for those reasons; it isn’t going away. Low money rates in U.S. dollar repo market (SOFR) or for government bills, not just U.S. Treasury bills, but also Japanese government bills, are all crucial and unmistakable warnings. The surging dollar exchange value is a telltale sign that the monetary system is fragile and prone to easy flight.

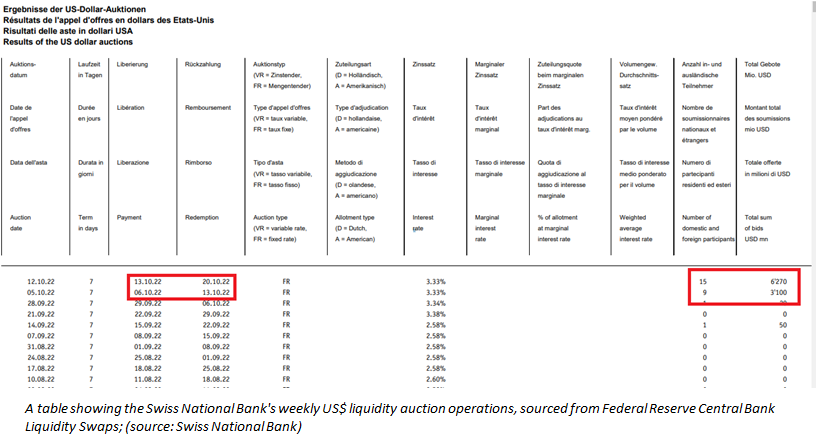

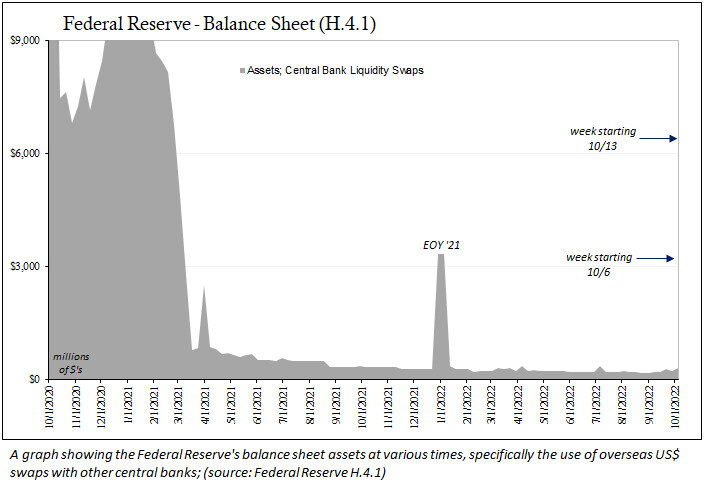

The ultimate source of this dollar funding is the Federal Reserve, employing what it calls central bank liquidity swaps. Yes, more swaps.

The question should answer itself. Two weeks in a row, we have to wonder if this is just the beginning.

Just which were those nine, now 15, banks, we don’t know, nor will anyone anytime soon. In fact, one key difference between these swaps and the discount window is anonymity. And that suggests the banks using the Swiss/U.S. dollar auctions might not be local. Perhaps they are Switzerland-based subsidiaries of foreign banks.

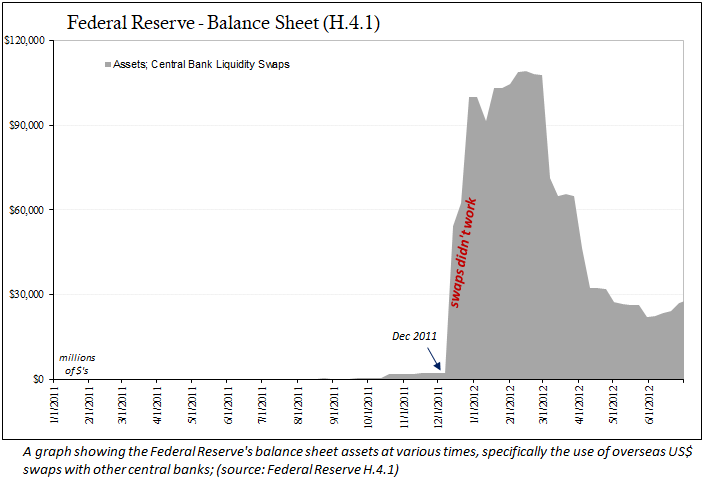

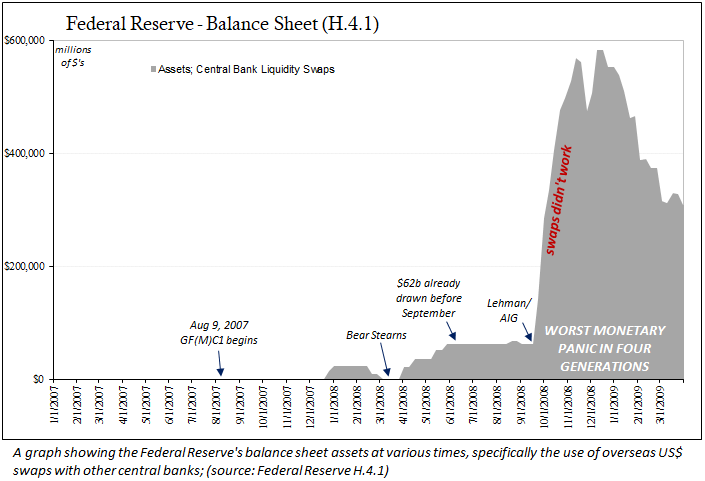

Take no solace in these swaps, either; they’re near useless (see above). Their only useful exploit is to tell us when the system is truly deteriorating, like in 2007–08, 2011–12, or 2020. The more swaps get used, the worse conditions must be getting.

We saw this coming. U.S. dollar irregularities have proliferated all year. And that is why markets are betting so heavily, so persistently, on lower rates in the months ahead, no matter how many times or how forcefully the world’s central bankers claim they’ll do no such thing.

Something is bound to break, to truly mess up the world, assuming it hasn’t already begun.