In a matter of months, the future hasn’t just dimmed, it has gone black. Think back to the end of last year, or even the first few months of this year. The U.S. economy’s “technical recession” was a complete surprise. Even though gasoline and food prices had been pushed higher along with those for far too many goods, everyone from policymakers to politicians to corporate managers was still highly optimistic.

You were far more likely to hear about the overheating economy in need of slowing than the dangers of a slowdown quickly turning into a nightmare.

We know how positive businesses were being because of how they had behaved. Forget what was being said; look at what these leaders did with their companies. Even though (to some degree because) containers and container ships remained piled up, logjammed coming from China trying to land and unload on the U.S. West Coast, retailers, wholesalers, everybody kept ordering to the max.

Container prices had peaked in September 2021, according to Freightos; the average at that time was nearly $11,000 per standard metal box. With only slight improvements in transportation and supply logistics, those charges had softened just a little from that top—still just about $ 10,000 per in mid-March 2022—reflecting the corporate desire to keep up the flow of goods.

During that happy-go-lucky period, inventories had begun to scale up to historic heights. The economy was white-hot and set to stay that way. It was widely believed the biggest risk to the good times was not getting enough stuff on shelves (remember #emptyshelves?).

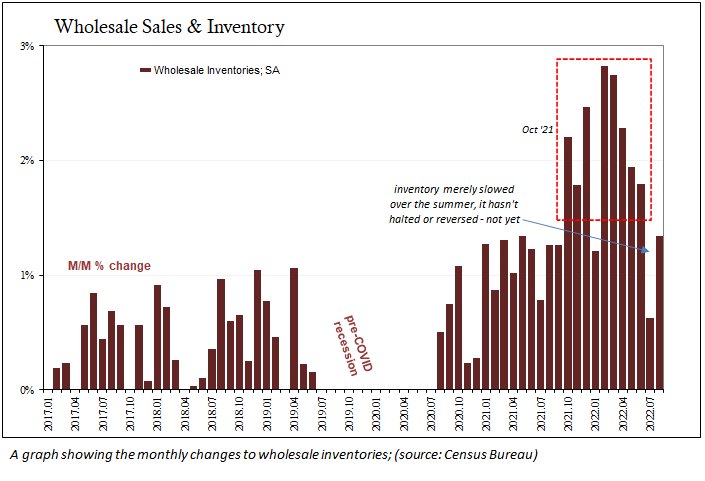

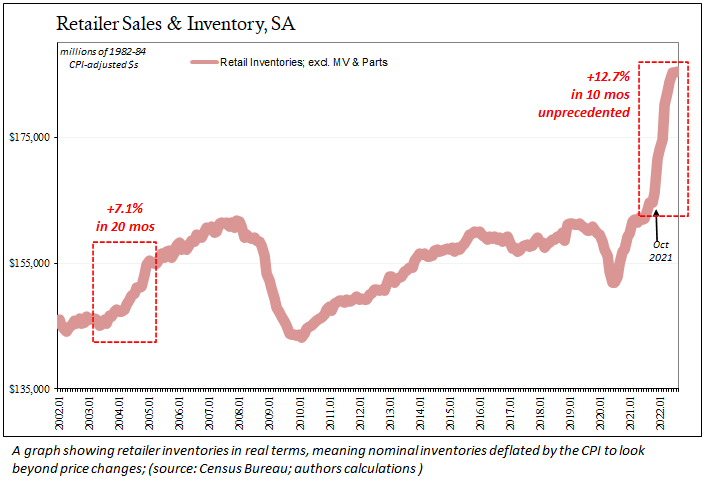

Using the Census Bureau’s estimates, and then adjusting them by the BLS’s CPI (or core CPI, where appropriate), retailer inventories exploded by nearly 13 percent in only the 10 months between October 2021 and the end of August 2022 (the latest advance data). Again, that’s in constant 1982-84 dollars.

The closest any other time has come to such volume was a 7 percent increase over the 20 months between mid-2003 and the end of 2004 when the “recovery” from the dot-com recession finally kicked in.

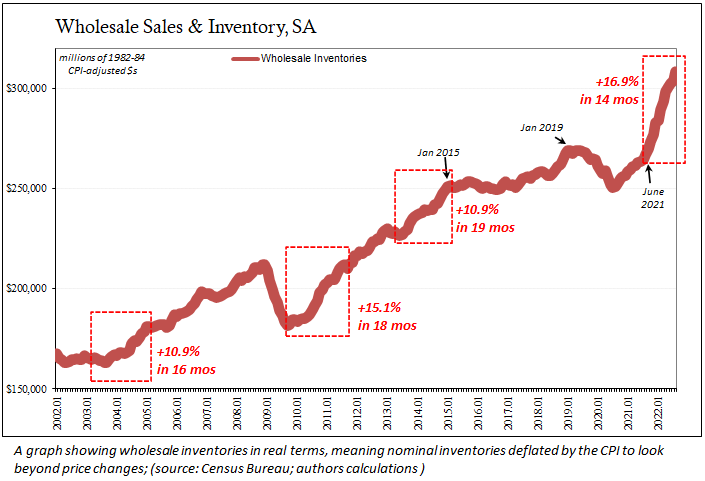

Wholesalers were in on it, too. Adjusting for prices, wholesale inventories surged 17 percent over the last 14 months dating back to July 2021. You have to go back to the period immediately following the end of 2009’s Great Recession for anything similar, and even then it was a 15 percent increase stretched out over a year and a half.

Around May and June, however, corporate managers began to figure out that America’s “technical recession” in the first of the year was more serious than at first thought. The initial contraction in GDP, believe it or not, had been dismissed on the accounting techniques used to calculate inventory contributions!

But real economic weakness persisted for what should have been obvious reasons. Consumers were already stretched even from last year, then as gas prices surged, food prices spiked, spending habits predictably shifted into frugality. Corporate America had mistaken one-time goods gluttony boosted by artificial means (the feds, not the Fed) for something permanent it clearly never had been.

Economic reversals, however, are a rather slow and uneven process. It’s not as if businesses flip a switch, turning from get-all-the-goods to shut-it-down all at once. Instead, the ordering was at first fine-tuned, the inventory once rising at a sustained historic pace modestly decelerated. Unbridled positivity had only transformed into cautious optimism.

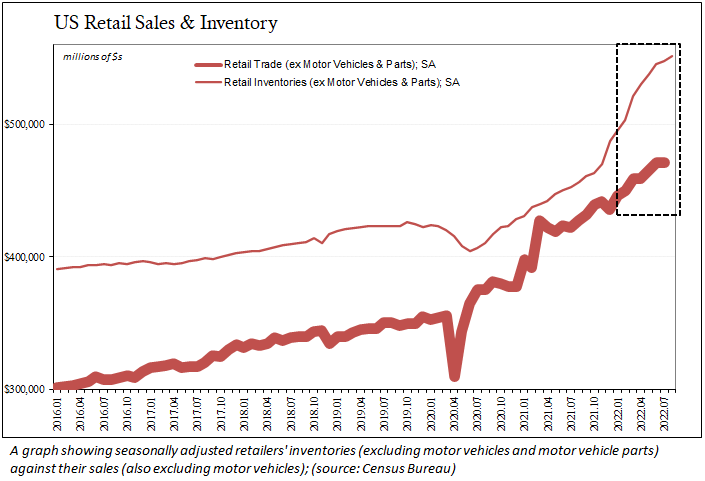

The more recent inventory estimates show this continued to be the overall perception right up until the end of this past summer. Again, adjusting for prices, inventories in August were no worse than flat compared to July or June. No huge cutbacks for either retailers or wholesalers, not yet.

“I hesitate to call it a blood bath, but it’s going to be ugly in terms of the amount of discounting and markdowns.”

That was Richard Hayne, the CEO of Urban Outfitters. His comment was no outlier, as Nordstrom’s Chief Financial Officer Anne Bramman admitted earlier in September. After slashing her company’s forecasts for revenue and more so profits, because of way too much inventory, Bramman added that discounting to get rid of unsold stock was “a lot deeper” and, worse, might “take a couple quarters” to sort out.

Average container prices overall are down to almost $4,000 per unit, nearly two-thirds below the peak. Those from China to the U.S. West Coast, where it once cost almost $20,000 because of how much of what Americans buy goes from the one to the other, you can now get a container for $3,441 (or thereabouts). This current average is now less than during the summer of 2020.

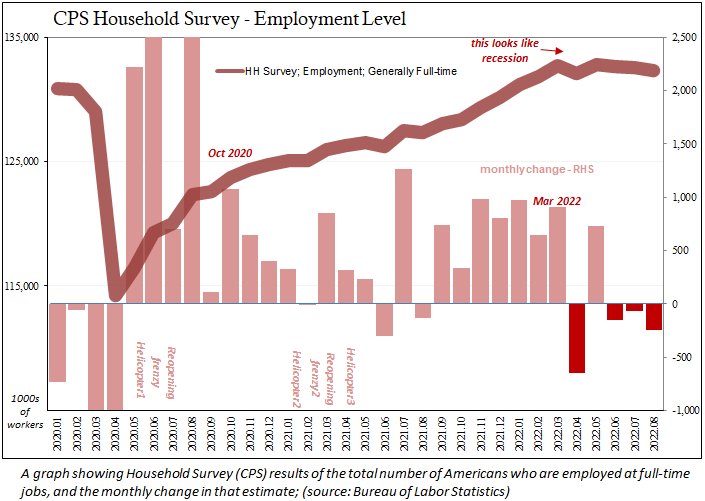

But the most distressing yet predictable development has been the downturn only now infecting the employment situation. While unemployment remains low, it is at best a lagging indicator; at worst, as it had been before, completely misrepresenting the health of the labor market and economy. Some government data shows companies are and have been cutting back hours, converting full-time jobs to part-time.

That’s just to start, with warnings like this one coming from Julia Pollack, chief economist for ZipRecruiter:

“We’ve not seen the normal September uptick in companies posting for temporary help. Companies are hanging back and waiting to see what conditions hold.”

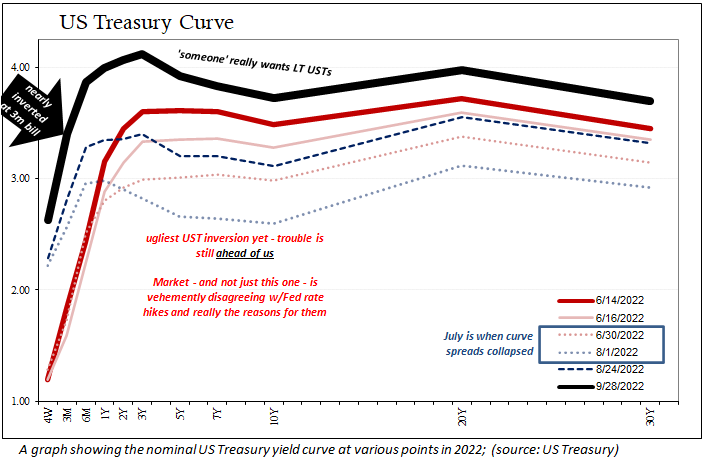

I’ve been writing here in these pages about how markets had cautioned beginning last year that the economy was never truly robust. They had forecast growing trouble right from start, long before Russia/Ukraine and the final, devastating surge in oil. At mid-year, curves sunk to 2007-levels of inversion, therefore predicting what we’re only beginning to hear about from the previously uber-confident.

In other words, that soon-to-be-forgotten technical recession really hadn’t been anything to be concerned about, though for completely different reasons. Rather than represent the previous “worst case” of a white-hot economy slowing to merely awesome, it had instead been the opening phase to a much worse and more prolonged slide whose worst days remain ahead.