After driving inflation to double-digits, the Federal Reserve has been adamant about monetary restraint to restore price stability. Can the Fed succeed? If so, at what cost?

Further, what needs to be watched to conclude the Fed is achieving its objective? What must occur to conclude the Fed has succeeded?

The Best Measure of Inflation?

Evidence the Fed is succeeding will come from various measures of consumer inflation. Monthly measures are preferable because they provide the earliest indication of a significant change.The two alternative monthly measures of consumer inflation are the Consumer Price Index (CPI) and the so-called consumer price deflator. Each of these includes both the prices for all items as well as core inflation, which excludes volatile food and energy prices.

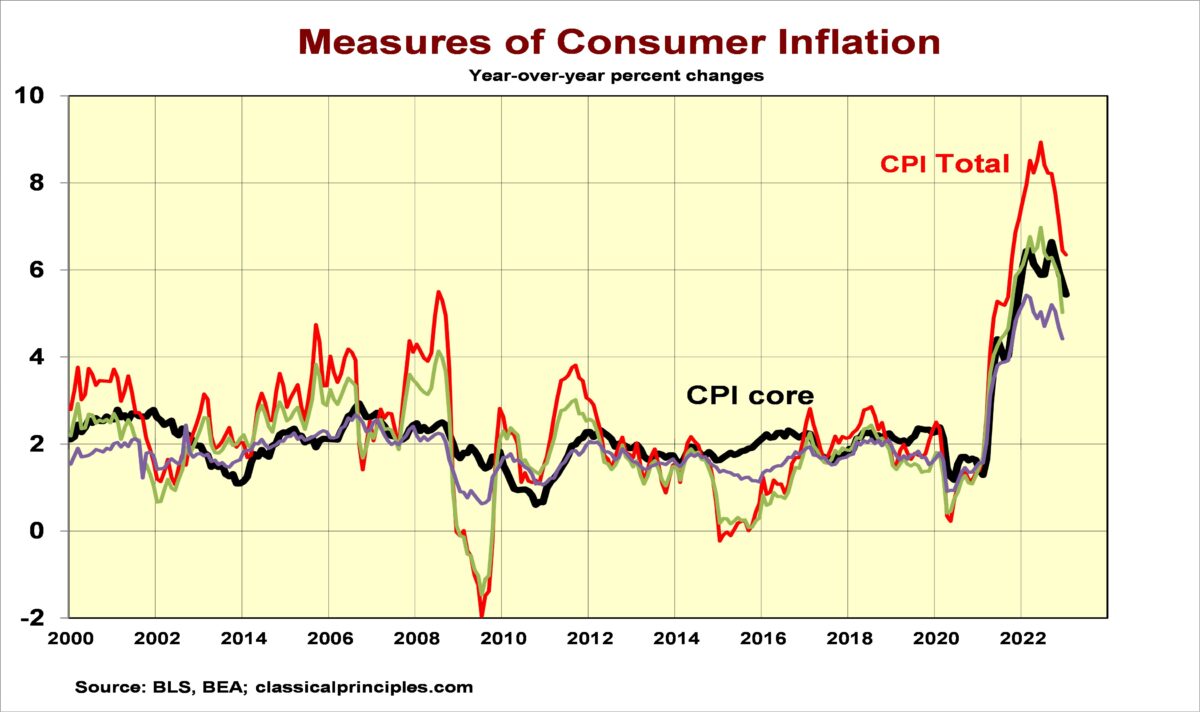

The following chart shows year-over-year changes in both total and core inflation for both measures. Interestingly, the most popular of all these measures is the total CPI. It includes all items. This is the measure tied to many contracts, including Social Security payments. It is also the most volatile and least stable of all these measures.

The bold, black line shows the core CPI, which clearly is the most stable with the fewest false signals. The alternative consumer deflators do not appear to add significant information beyond the more conventional CPI.

(Source: Bureau of Labor Statistics / Bureau of Economic Analysis)

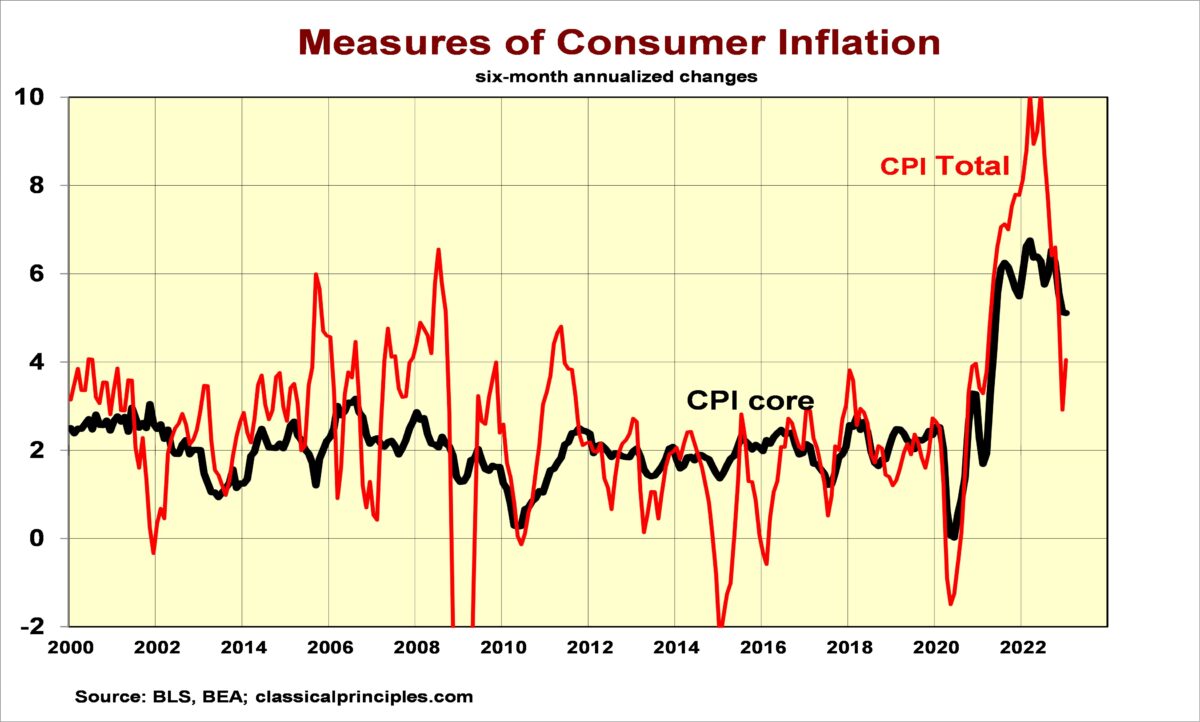

Another consideration in assessing inflation is the best time period for identifying an emerging trend. While conventional reporting focuses on the year-over-year change, observing changes over a six-month period can provide an early sign of any change.

The next chart shows the annualized change in both the total CPI and core CPI measure over six months. Changes in the total CPI are so volatile as to appear meaningless.

(Source: Bureau of Labor Statistics / Bureau of Economic Analysis)

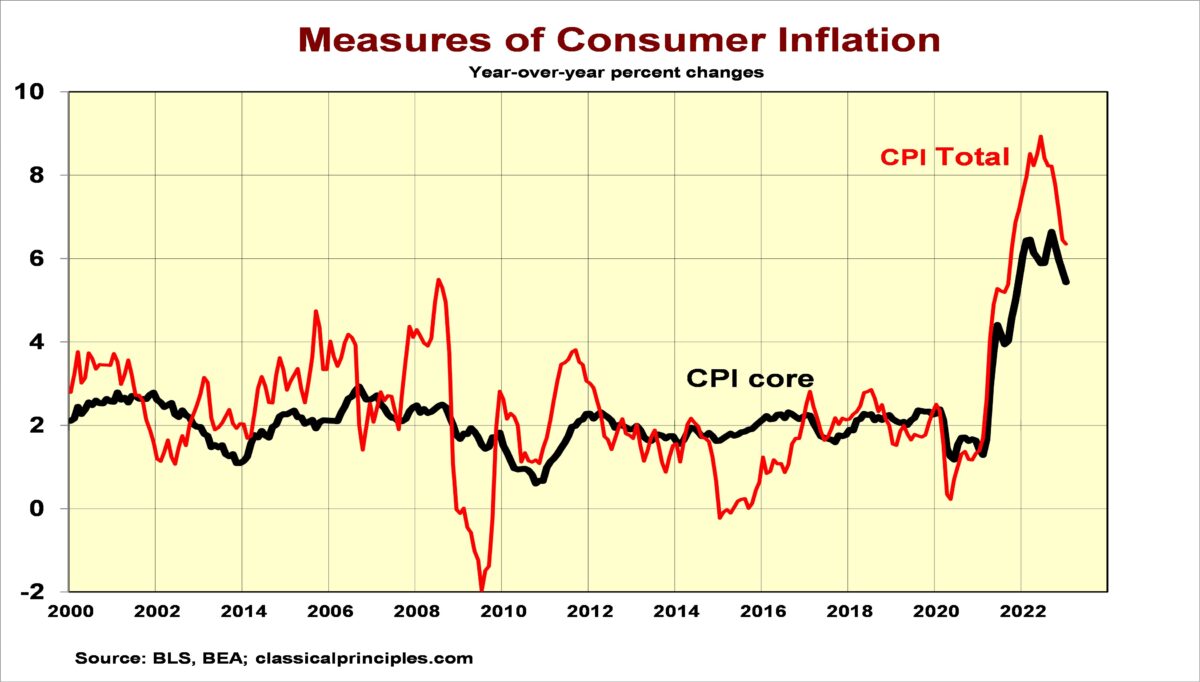

The next, and final chart, shows the core CPI over both one year and over six months. The six-month change is slightly more volatile than the yearly change. This is most apparent during periods of major changes business, such as the lockdown during COVID and surge from the recovery from the lockdown. For most periods when the economy is moving in a more stable direction, the six-month change is reasonably close to the one-year change in identifying underlying inflation.

Can the Fed Contain Inflation by Year-End?

Yes, but …. The Fed has the ability to contain inflation by year-end, but doing so will involve several things. The Fed can increase its chances of success by providing a clearer guide to success. Our inflation analysis indicates that the Fed should define success as a one-year period where the core CPI measure is in the vicinity of 2 percent.Once the Fed has defined success, it should announce its intent to conduct monetary policy in a manner to confine the growth in current dollar spending (GDP) to no more than 4 percent. This means retaining a restrictive policy until current dollar spending is clearly trending toward growth rate of 4 percent or less, after allowing for normal lags between policy and its effect.

Data for January suggest current dollar spending is growing at an annual rate of 6–7 percent. Core inflation appears to be in the range of 3–4 percent. If current dollar spending were to remain this high, it will be impossible for the Fed to succeed.

My analysis shows the Fed’s policy restraint began in July 2022. Since monetary policy works with a six- to nine-month lag, current dollar spending should slow sometime between January and July of this year. If the Fed maintains its restraint, current dollar spending should slow to a pace of 4–5 percent by year-end, possibly sooner.

While history suggests inflation can take two to three years to slow, most of this history involved a gradual buildup in inflation. Since the current inflation came on quickly, it is not ingrained in the system. This means it should come down faster, perhaps in 12–18 months.

One final factor determining the Fed’s chances of success will be what happens to the nation’s productivity. If productivity continues to decline, as it has over the past year, growth will be feeble or nonexistent. Under such conditions, inflation is certain to exceed the upper limits of the Fed’s target. At that point, the Fed would have to consider its legal mandates. The Federal Reserve Act mandates that the Federal Reserve conduct monetary policy “so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

The Fed has only indirect control over the economy’s productivity. Over the past year, Congress and the Biden administration have enacted legislation that has seriously weakened the nation’s productivity. Unless the new Congress can mitigate the damage, or productivity somehow improves, the Fed’s chances of achieving it 2 percent target will be gone with the wind.