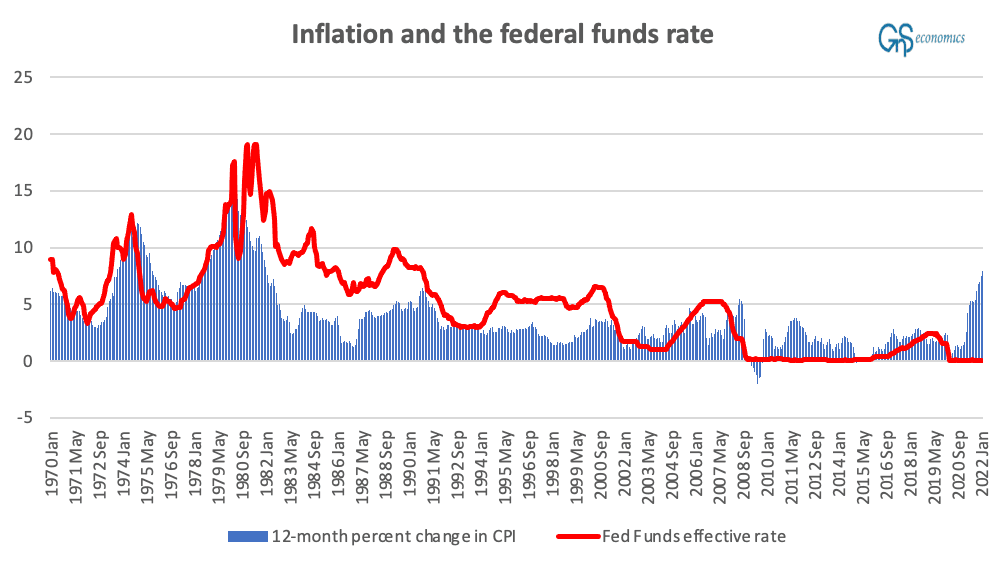

In February, the United States recorded the fastest inflation print, 7.9 percent, since January 1982. In January 1982, the federal funds rate was 13.2 percent (on average). On March 16, the Federal Reserve raised the federal funds rate to a range of 0.25–0.50 percent. It’s a joke, really.

Like I wrote in my previous article, the most pressing economic issue relating to the war in Ukraine is its likely effect on inflation. While we are also likely to face some serious banking issues down the line, the approaching inflation shock is probably going to be so massive that it can act as a trigger for much wider economic calamity.

That’s why it’s rather perplexing to watch some economic commentators arguing that central banks should dismiss ravaging inflation, because it’s due to a “spike in energy prices.” A spike in energy prices is definitely happening, but how about wheat (up around 50 percent since start of the invasion), nickel (up around 150 percent) or potassium chloride (up over 50 percent)? The shock to the inflation gauges come not just from energy prices, but from a wide variety of commodities and metals. Henning Gloystein, an analyst at Eurasia Group, stated in a Bloomberg interview on March 3 that “We’ve never seen such steep and sudden commodity price spikes across so many assets.”

Like I also wrote previously, war and sanctions will most likely have far-reaching consequences on the world economy. This shock is just the beginning, but it really could not have come at a worst time.

To shed some light on the issue, it’s probably beneficial to clarify the dynamics of inflation and repercussions of fast inflation with the help of a historical example from the 1970s.

The United States became dependent on the oil imported from the Middle East after her oil production peaked in 1970. In 1973, as a result of the Yom Kippur War fought between Israel and a coalition of Arab States led by Egypt and Syria, the Organization of Arab Petroleum Exporting Countries proclaimed an oil embargo against western countries supporting Israel. In six months, the global price of oil rose by nearly 300 percent, but oil prices in the United States rose even more. The economies were rather heavily oil-dependent at that time, which exaggerated the effect of the oil price shock.

During 1973, wages in the United States were growing at a stable rate of around 6 percent, but during the second quarter of 1974, wage growth accelerated to 9.6 percent and kept on accelerating. As a result, inflation reached 12 percent in 1974, the Fed raised interest rates, and the economy fell into a recession.

By late 1976, the inflation had dropped to little over five percent. Then, in 1979, the Islamic Iranian Revolution began, causing widespread instability in the Middle East and stirring a panicky reaction from the markets. The price of oil doubled in 12 months. In 1980, the Iran-Iraq war commenced, which led to further declines in oil production, more instability, and even higher prices.

By late 1970s, the public had learned to expect fast inflation, which pushed wages higher. As a result, the annual inflation rate in the United States rose to over 14 percent in early 1980s. The President of the Federal Reserve, Paul Volcker, lifted the interest rates from around 11 percent in 1979 to 20 percent in June 1981. This led to a recession, but it also killed inflation, which fell below 3 percent in summer 1983.

What is notable is that the war in the Middle East in the 1970s affected mostly just oil prices. This time around, the repercussions of the war and sanctions are much more widespread, from the real economy to finance. That’s why the situation is actually more worrisome.

Most importantly, the example of the 1970s shows two things: First, it takes around six to nine months for the inflation shock to manifest in wages if the shock persists. This has already happened in the United States. Secondly, in the current economic system, raising of interest rates by the central bank are the only way to rapidly and effectively control inflation. This has not happened anywhere yet.

What we need to understand, thoroughly, are the dynamics of inflation. Inflation shock can originate either from the demand or supply side. That is, inflation shock can come from either too much demand of some commodities with respect to the level of current production or the supply (production) of commodities may suddenly diminish, while demand remains high.

It the end, it doesn’t matter what the source of the shock is, because if the shock persists, wages start to rise. And, when that happens, inflation starts to feed itself. As wages rise nationwide, corporations transfer increased wage costs to prices. As prices rise, it lowers the purchasing power of wages, which leads to demands for higher salaries, restarting the cycle. As a result, fast inflation becomes self-sustaining.

However, when faced by a strong enough supply-side inflation shock, the economy can enter to a deleterious state called stagflation. In it the economy falls into a recession while inflation runs rampant. Thus, the economy will experience a combination of high unemployment and fast inflation. This is a recipe for serious societal unrest, which is what occurred in many countries in the 1970s.

What we are now facing is a threat of stagflation. It is almost certain that the world economy is about to face a serious or even a never-before-seen inflation shock. In addition, growth forecasts have been in decline, and the highly-indebted world economy is unlikely to be able to cope with rising interest rates.

Even if Russia and Ukraine would settle a truce quickly, the conflict is already so deep and global that de-escalation will almost surely take some time. This implies that, while we would be likely to see markets rally with news of a ceasefire, the inflation shock is likely to persist and likely to worsen. This would leave central banks with very few options but to raise rates and eventually run-off assets from their balance sheets. Last time they tried this, in 2018 and 2019, the financial system almost imploded, and now there’s more debt, everywhere.

Considering this, the inflation shock could be all that is needed to push it into a period of overlapping economic crises—a possibility we have been warning about for over a year.