The world economy has been on a perilous road for over a decade. The Global Financial Crisis (GFC) that hit the world in full force in September 2008 led central bankers and the government to issue extraordinary measures to stop the financial sector from melting down.

Governments, for example, issued blank guarantees to bank debt and deposits, and recapitalized banks, while the Federal Reserve set up liquidity-swap operations with other central banks to guarantee the availability of dollars.

However, the most drastic innovation was the asset purchase programs of central banks, dubbed quantitative easing (QE). The Bank of Japan ran a first-ever QE program from March 2001 till March 2006. The program was deemed unsuccessful and canceled, but that didn’t stop central banks from enacting such programs during the GFC.

During the first round of QE, launched on Nov. 25, 2008, the Federal Reserve bought bonds issued by government-sponsored enterprises and mortgage-backed securities. In March 2009, the program was extended to include the U.S. Treasury debt. Seemingly, the aim of the Treasury purchases was to stimulate investments by lowering long-term rates, and to support consumption by boosting the asset prices (bonds and stocks). While the theory and reasoning for the QE came later than the actual onset of the program, it seems that the Fed also wanted to artificially raise the prices of assets to create a wealth effect. The Fed thus assumed that by making people feel richer, they would spend more, which would grow the economy.

When a central bank buys assets through QE, it operates only through so-called Primary Dealer banks which, however, are not often banks, but broker-dealers. The central bank buys the assets, usually Treasurys, with newly created central bank reserves, which are “excess reserves” to a bank. So the central bank doesn’t buy the assets with money, but with reserves, that is, deposits at the central bank.

If the seller is a bank, it ends up holding the excess reserves (in exchange for the assets). However, if the seller of the asset is a non-bank, for example, a corporation, hedge fund, pension fund, or another trader, the reserves end up going to the central bank account of the bank of the non-bank. These will be balanced with new deposits, which are owed to the non-bank. That is, assets are bought from non-banks with deposits.

So QE programs force both excess reserves as well as new deposits into the banking system. These may have very different effects in the economy, as excess reserves flow only between financial institutions (banks), while new deposits are money entering the economy. From whom did central banks buy the assets: banks or non-banks?

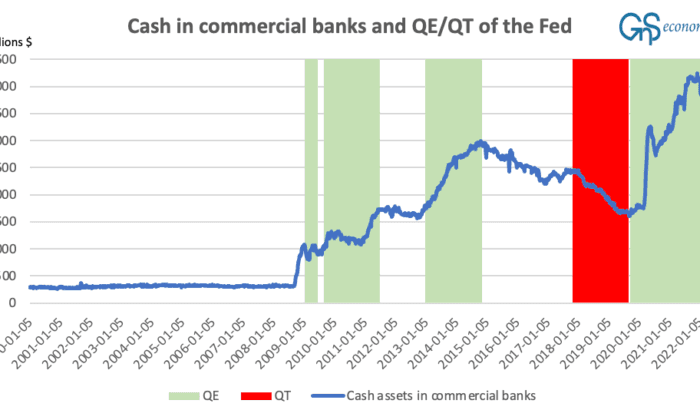

Seth Carpenter, Selva Demiralp, Jane Ihrig, and Elizabeth Klee found in their paper, “Analyzing Federal Reserve asset purchases: From whom does the Fed buy?” that, during QE1 and QE2 which ran between November 2008 and December 2012, the Fed bought Treasuries mostly from households, including hedge funds and pension funds. Essentially what happened during Q1 and Q2 was that the Fed pushed vast amounts of cash assets into commercial banks. When the Fed has shrunk its balance sheet by selling the assets, in a program called quantitative tightening (QT), the opposite has happened. More on QT later.

Where have the excess cash and bank deposits of households and investors gone, then?

According to research, “On the international spillovers of U.S. quantitative easing,” by Marcel Fratzscher, Marco Lo Duca, and Roland Straub, published in 2016, the first round of quantitative easing by the Fed led to flows toward U.S. assets, especially equities. The second and third rounds of QE led to capital flows outside the United States. Essentially this means that the cash, pushed into banks by QE programs, was used to speculate in the financial markets both in the United States and abroad.

How did the excess reserves forced into the balance sheet of commercial banks change their behavior?

John Kandrac and Bernd Schlusche found in their research—“Quantitative easing and bank risk-taking: evidence from lending”—that excess reserves led to higher total loan growth and increased risk-taking. That is, the QE program altered the net interest margins (between deposits and loans), the liquidity profile, and the duration of the assets held by the commercial banks. These changes induced the banks to increase lending and move their portfolio toward riskier lending activities.

- They led to massive speculation in the financial markets, and

- They led to increased risk-taking in the banking sector.

What makes the situation even more problematic is that central banks can’t really wind them down without bringing the financial markets and the economy down with them. The Fed tried this through the asset selling or QT programs in 2018 and 2019, which led to the near-collapse of asset and credit markets, and the near-implosion of the repurchase agreement, or repo market. Now, the Fed is poised to try again, and we really can’t expect any other result.

Moreover, QE programs of the European Central Bank (ECB) have been the main reason why the heavily indebted eurozone countries can borrow at very low rates. Or would lend to the government of Italy for 10 years with a yield of little over two percent? QT of the ECB would thus lead to the collapse of the sovereign bond markets in the eurozone, and to the unraveling of the European common currency.

Alas, central bankers have painted themselves into a corner with no way out. Now, due to hastening inflation, they’re forced to try, which most likely won’t go down well with the financial markets and the economy.

Brace.