The latest released U.S. inflation rate showed that overall inflation eased a tiny bit from 8.3 percent to 8.2 percent, while core inflation (excluding food and energy) edged up from 6.3 percent to 6.6 percent. The divergence between overall and core inflation began in May and has persisted until now, as both have been showing flat trends. When there is no unilateral movement of the inflation rate, core and non-core rates can diverge, as we’ve seen over the past months, until they both restart another unilateral movement.

The most worrying thing is that “another unilateral movement” may not happen anytime soon. Even if inflation has peaked, it may stay flat at the existing level for a long time. U.S. core inflation has been 5.9 percent to 6.6 percent since the beginning of 2022. There has been little change in the trend regardless of commodity prices surging and then slumping during the period. This flat trend has remained for three quarters, and can hardly be regarded as transitory. Moreover, any level over 6 percent is unacceptably high.

Apart from food and energy prices slumping over the previous two quarters, demand also slowed, as was evident from a basket of macroeconomic data. When supply growth rises and demand falls, the supply curve shifts rightward and the demand curve shifts leftward, and the price (inflation) change should be downward. However, this is not what we have seen over the past three quarters. If supply and demand together cannot explain the observed price (inflation) change, then there should be some other factors at play.

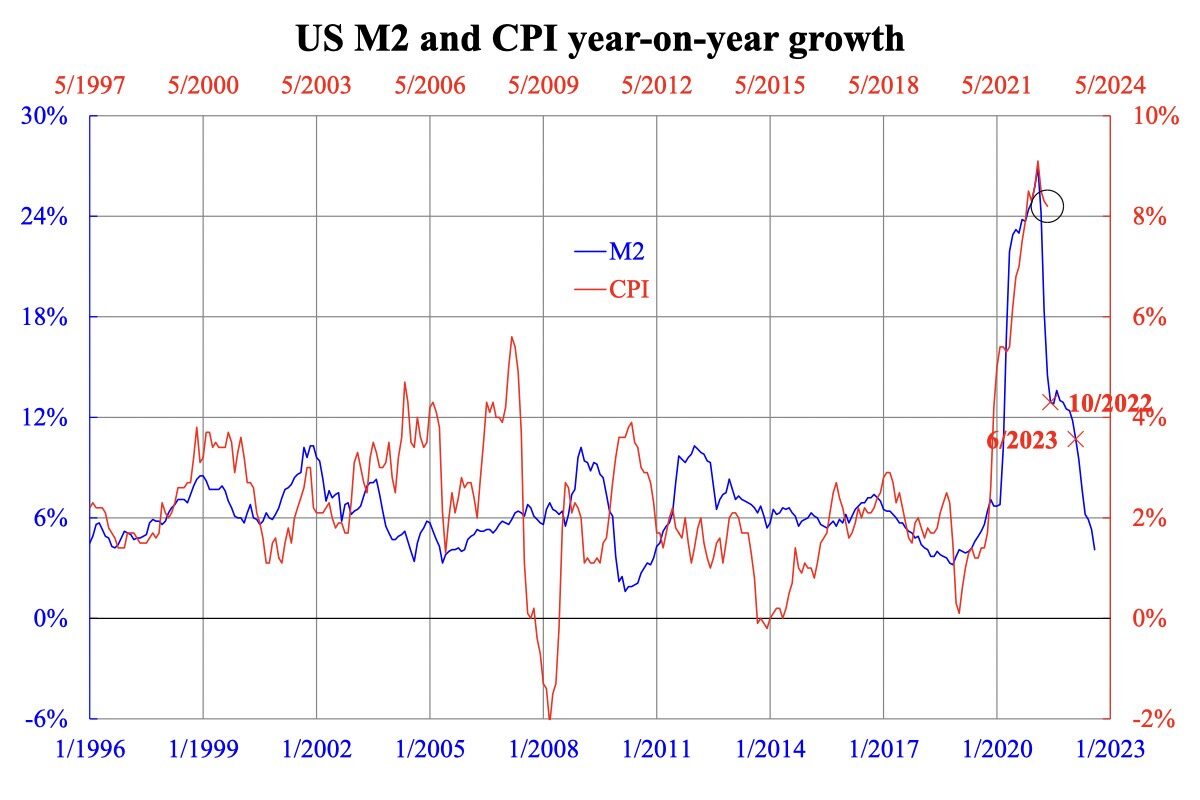

The accompanying chart shows the relationship between broad money (M2) growth and Consumer Price Index (CPI) year-over-year inflation, which has been shown before in my column and is now updated. Past experience shows that money growth causes inflation with a four to six quarters lag; now, this round of inflation lags by five quarters which is consistent with previous experience. Had money been the sole cause of inflation, we should have observed inflation speedily coming down by now, as the money growth did five quarters ago. But it is, in fact, not falling (see circled area in the chart).

Money growth primarily controls the demand side; the supply side, like energy constraint, is not controlled by money. Given that the supply constraint has eased, it should not pose an upward pressure on inflation, which is evident from the fall in non-core inflation. As core inflation remains high when demand-driven inflation should be fading out, it is logical to suspect there are factors other than demand or supply, like inflation expectations, which are out of control. In fact, there is more recent research published by the Fed concerning this area.

Unanchored inflation expectations are very troublesome and can take longer to fix. The Fed now realizes this may turn out to be the case. To avoid repeating history, this time, they might well have overdone tightening, which is regarded as one of the major risks ahead.