The U.S. personal consumption expenditure (PCE) based inflation released last week eased a bit from 6.6 percent in March to 6.3 percent in April. Thanks to the higher base in April 2021 than March 2021, larger denominator makes year-over-year growth lower. Analysts claim that inflation had peaked. But this number is subject to base effect and the influence of noncore volatile items, i.e. food and energy. Examining the core PCE month-over-month inflation which excludes volatile items and without base effect, the April number is essentially the same as the March one, standing at 0.3 percent.

Annualising this gives a year-over-year inflation of 3 to 4 percent. This looks low but may only be “transitory” in Fed’s term. Like stock prices, goods prices do not rise along a strictly linear path, occasional low growth cannot confirm a peak. In fact, the core PCE month-over-month inflation is still on the past two years’ linear uptrend. As we have argued previously, the source of recent global high inflation (ex-China and Hong Kong) is mainly due to ridiculous monetary easing. So long as such excess is not largely withdrawn, inflation will not be low.

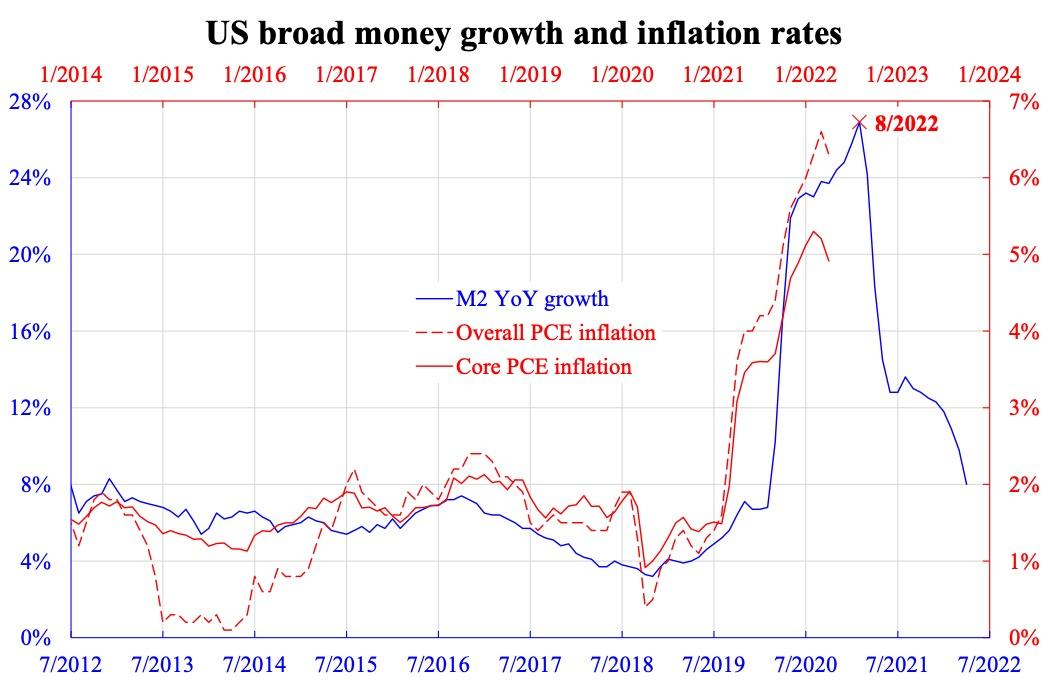

The accompanying chart tries to infer the timing of inflation peak ahead from broad money growth. From Irving Fisher’s quantity theory of money (equation of exchange), it seems obvious that two of the four variables—money and price level grow exceptionally faster than the remaining two—money velocity and transaction. It follows that money growth should largely predict price growth (i.e.inflation). Since the former refers to the money available for transactions, broad money should be used instead of the narrowest monetary base.

The chart shows both, with inflation in both overall and core indexes.

Some accuse inflation to be primarily commodity-driven due mainly to the Ukraine-Russian war. This is wrong. Firstly, inflation already edged up since central banks’ monetary easing; the war started when inflation was already very high. Secondly, core inflation excluding most commodities also rose in the same manner. If money growth predicts inflation, then the past decade’s relationship suggests the former leads the latter by about one and a half years, which implies that inflation would peak in the next quarter.

Even if the August number will be the highest, we would not see it until September with release lag, and will not be able to confirm the peak at least till October when a lower number is seen. If as Jay Powell the Fed Chair said, rate hike would still continue until inflation comes down meaningfully, then the hike cycle will extend to at least next year, from this chart’s prediction. Moreover, if it is perceived that the worsening inflation would last until October, there may not be room for the Fed to step back from 50 basis points to 25 in the September or even November meetings.

Even the 75 basis points hike might not be on the table. The upward revision of hikes in autumn meetings might pose another round of threats to the market. The current respite may not last for too long.