The Bank of Japan (BoJ) has adjusted the yield curve control (YCC) by allowing the cap of the 10-year sovereign bond yield to reach 1 percent instead of the previous 0.5 percent. Since both the short-term policy rate and the long-term ten-year target yield remain unchanged at -0.1 percent and 0 percent, respectively, this clearly is not a tightening action, but it does allow for higher volatility at the long end of the yield curve. Although the volatility of funding cost (ten-year yield) would theoretically retard investment, the actual effect of such a second-moment effect is less than the first-moment effect; a direct hike.

Whether a direct rate hike would slow down investment is not clear from the data. In principle, though, a tightening through rate hikes would slow down bank lending growth, which is the primary source of funding investment. If such a relationship cannot be seen clearly from the data, it would be challenging to continue arguing about the effectiveness of interest rate policy.

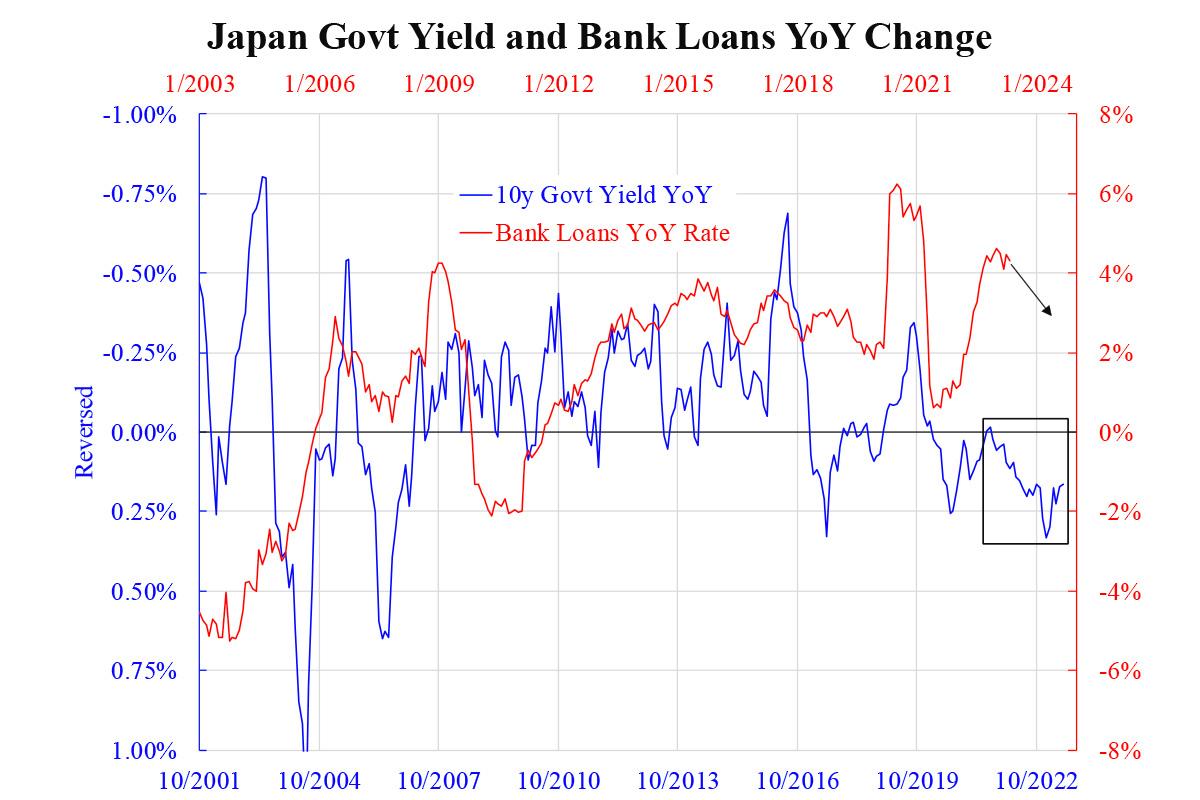

The attached chart shows the relationship between ten-year sovereign yield year-over-year (YoY) change and bank loans’ YoY growth rate. Empirical evidence from countries like the U.S. indicates that monetary policy takes at least one year (and up to two) to become effective. This assumes that there is a five-quarter lag from yield change to loan growth. And, because higher yield change should result in lower loan growth, the left vertical axis is depicted upside-down. Loan data begins from 2001, so the chart is already showing the maximum period.

The conclusion is clear and two-fold. Firstly, the yield cut in the early 2000s was ineffective and loan contraction remained severe without showing much response to policy. This was a typical debt trap scenario where almost none of the policy tools worked. Secondly, the yield rise after the mid-2010s was also ineffective in bringing down bank loan growth, even when accounting for the five-quarter lag effect. The two series might still exhibit the same direction when the lag is discounted, but the levels are far from being matched, so the slowdown in loan growth will not be materially obvious.

The BoJ might be happy with this position after enduring decades of deflation and underinvestment. However, the current inflation (3 percent to 4 percent) could be too high for many, given that the real GDP year-on-year trend growth is relatively low (1–2 percent). Such investment boosting price (CPI) more than quantity (GDP) is an unintended and unwanted consequence.

As the rest of the world is no longer subject to a supply shock, the appropriate way to tackle inflation is by impeding demand. This is also true for Japan, with its wage-price spiral and recovering internal demand being observed over recent years.

Like the rest of the world, the BoJ is probably betting on inflation coming down, albeit slowly. A transition from the current 3 percent to 4 percent, to the 2 percent target seems achievable. This explains why they did not change any of the rate targets. Nevertheless, inflation elsewhere is slowing down too slowly. The BoJ might be more apprehensive than it had been when evaluating whether such a 2 percent target is achievable in the near future, thus resulting in its latest YCC adjustment.