The mainstream is believing the U.S. and many other advanced economies can avoid recession. One line of reasoning is the relatively dovish tightening, where in most countries, the real interest rates are still negative, so stagflation is replacing recession. Another line is due to the tech boom, which just kick-started a new industrial revolution. This time we focus on the latter.

Recently there has been heated debate between two camps: One side believes the tech boom still has a long way to go, yet the other suspects the boom impact has been exaggerated, and that this has already been over-priced into the market, as can be seen from how the Nasdaq index has outperformed the traditional Dow Jones index.

While the performance of tech stocks reflects what the market thinks, the reality is another thing. By “reality,” it means how much real value-added this second tech boom will bring to the economy. In economics, tech is not easily measurable because it is not a standalone item but embedded in other existing equipment or tools. The standard old way to isolate tech contribution from others is by the method of elimination.

The idea is that output (GDP) is produced by inputs, primarily capital (money) and labor (man-hours). Then tech is merely the ratio of output minus input which resembles the concept of “efficiency” in physics. Tech is said to be growing when more output is produced with a given input amount. This is achievable since the two inputs are measured by money and time spent.

The change in efficiency reflects any new tech contribution. Technically, output growth is regressed on inputs’ growth, the unexplained growth component refers to the tech growth.

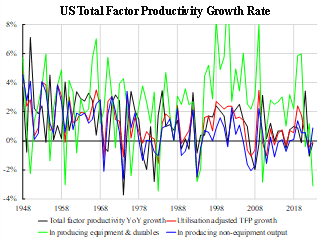

John G. Fernald of the Federal Reserve Bank of San Francisco has compiled the data with some adjustments and breakdowns. The accompanying chart shows the raw TFP adjusted for capital and labor utilization. Then the adjusted series is also split into equipment and non-equipment. Surprisingly, the measured total TFP growth does not show exceptionally high growth in the past decade or two (except 2021). In fact, the trend growth is lower than that in the late 1990s and early 2000s. All sub-series exhibit similar downtrend patterns.

One can argue that the latest AI development has yet to be reflected in TFP. However, the Internet and related tech development in the late 1990s should have been fully realized, but the trend growth in the 2010s was still lower than that in the 2000s. This poses doubts about high expectations of the recent tech tide, which is supposed to be an extension of that of the 1990s.

The GDP growth in the 19th century with the industrial revolution was not exceptionally strong compared with the 20th century. This revolution might change a lot, but probably not in growth terms.