Gold’s Historical Performance

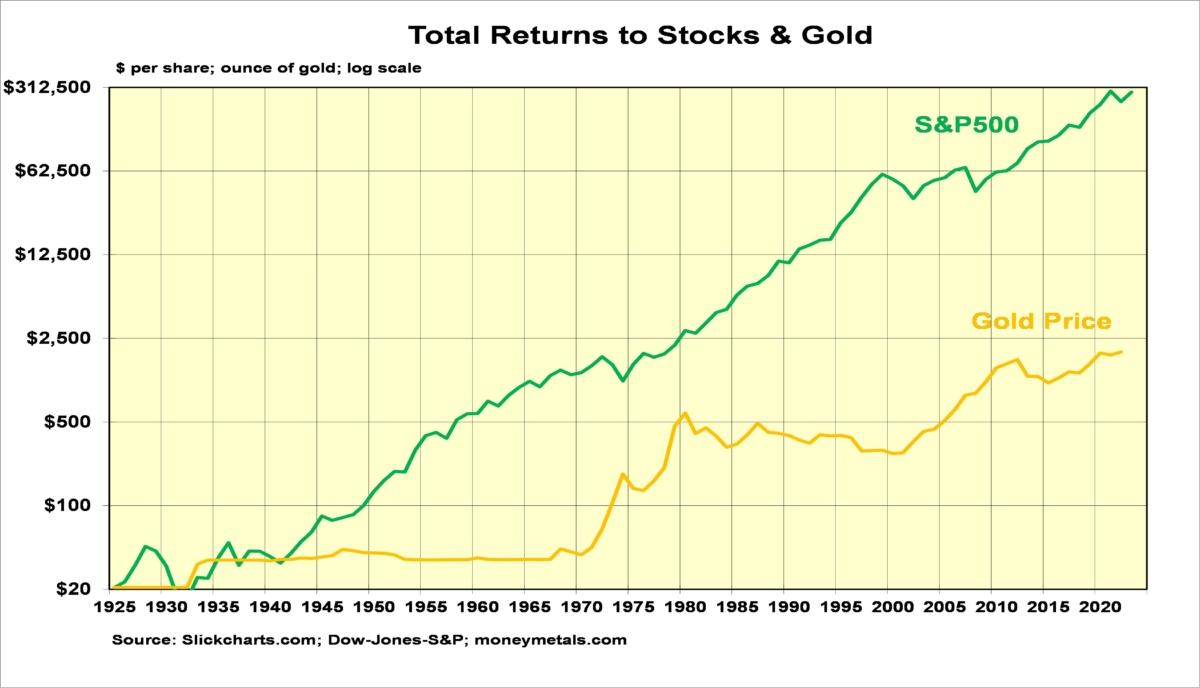

The long-term history of gold shows it can be an effective hedge against inflation. However, returns to gold tend to be unimpressive compared stocks. The following chart shows the comparison between an ounce of gold purchased in 1925 and an investment in the S&P 500 Index.Over this period, gold held its value against inflation. The average gain for gold was 4.8 percent a year while inflation averaged 2.9 percent. However, at the end of 2022, gold purchased at $20.67 in 1925 was worth just under $2,000. The total return to the S&P 500 made it worth almost $300,000. From a longer-term perspective, stocks are a far better investment than gold.

When Was Gold a Good Investment?

To assess if gold is an attractive investment today, it helps to look at the three times during the past century when gold was a good investment.The first was during the first half of the 1930s. Beginning in 1929, a shift away from free-market classical principles led to a collapse in both the stock market and the economy. If a person bought gold at the end of 1929 and sold it at the end of 1934, the ounce of gold would have been worth $14.33 more, a 69 percent return.

Unfortunately, in 1934 the United States outlawed the holding of gold for monetary purposes. Under penalty of 10 years in prison, citizens had to sell their gold holdings to the Treasury at the government’s fixed price of $20.67. Even so, gold kept its value from 1929 to 1934, while stocks lost 41 percent of their value.

The second period where gold was a good investment was from 1970 to 1980. After raising the gold price to $35 in 1934, the U.S. government fixed its price at that level until 1971. Over these years, inflation raised the market price well above the governments fixed price. The United States ended its attempt to fix gold prices in 1971 in response to foreigners rushing to exchange dollars for gold. Once gold was permitted to respond to market pressures, its price went from $38.90 at the end of 1970 to a daily peak of $850 in 1980.

Those who bought gold in 1970 and sold it at the end of 1980 had a total return of 1,429 percent. Over the same decade, the return to stocks was 125 percent, which was mostly wiped out by a 117 percent increase in inflation.

After 1980, the gold market settled down. In the 20 years from 1980 to 2000, gold fell from $595 to $273. This set the stage for the third period when gold was a good investment. From 2004 to 2011, gold prices soared from $400 to a daily peak of $1,922 in 2011.

Is Gold Currently an Attractive Investment?

There are two things currently to consider when deciding to buy gold. The first is U.S. economic policies. It is notable that each of the three historical periods of soaring gold prices occurred when U.S. politicians moved policies away from free-market classical principles. Since 2020, politicians have repeated this mistake with massive increases in federal spending, debt, and regulations.However, historically it has taken more than a seriously weakened economy to send gold prices soaring. Prior to each period where gold has been a good or great investment, gold prices were undervalued. In order to assess if gold is currently a good buy, it is important to attempt to estimate gold’s intrinsic or fundamental value. What is an ounce of gold worth?

Some economists will tell you an item is worth whatever people are currently willing to pay for it. While true, this is a useless answer.

All commodities have some intrinsic value; and all commodities tend to move in the same direction over time. Unique factors affecting supply and demand often send the price of a particular commodity either above or below those of all other commodities.

When unique factors send the price of a commodity above or below other commodities, it sets into motion powerful forces to bring the price back in line with all other commodities. When a commodity’s price moves higher than other commodities, resources shift to produce more of the higher-priced commodity. Also, demand for the higher-priced commodity tends to fall as the relatively higher price discourages consumption and attracts lower-priced substitutes. Over time, the combination of these forces tends to bring the price of higher-priced commodities back in line with the prices of other commodities. These forces tend to move in the opposite direction when a commodity’s price moves lower than other commodities.

To find a commodity’s intrinsic value, it is important to relate its price to other commodities during periods when markets are free to adjust. Our approach uses the period from in 1982 to 2022 to calculate the average relationship between gold prices and the Commodity Research Bureau (CRB) Index for raw industrial commodities.

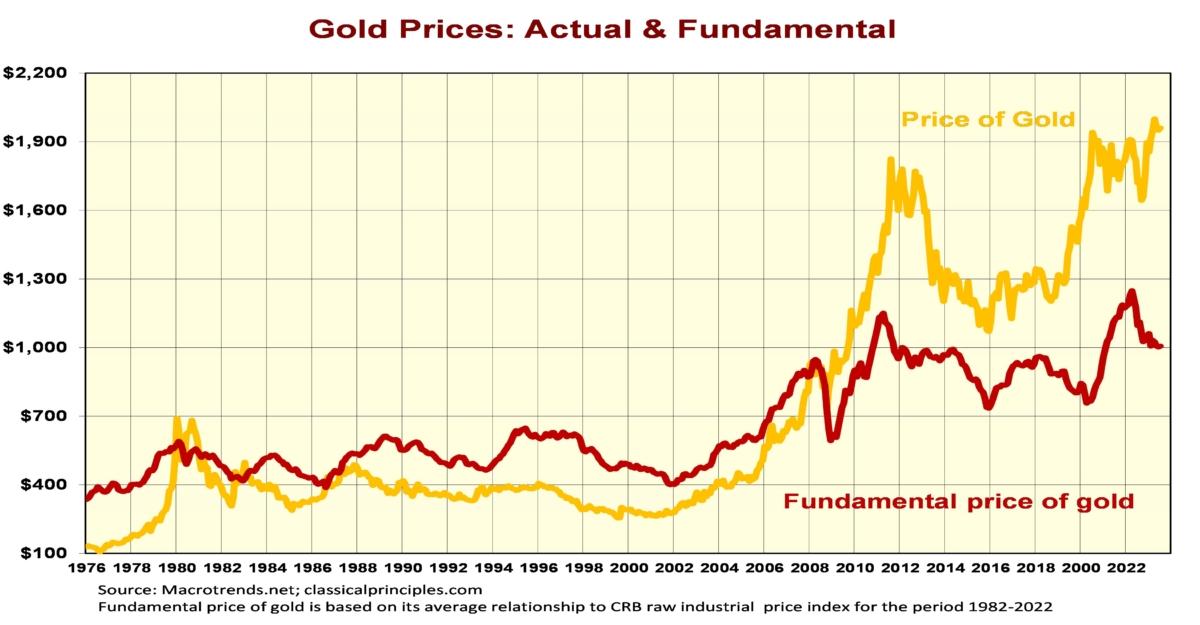

The following chart shows the price of gold as well as its intrinsic or fundamental price. This is the price of gold based on what it would have been had gold prices simply matched the movement in the prices of other commodities. From 1980 to 2005, gold prices increased at a slower pace than other commodities. Hence, the analysis shows and extend period when gold prices were selling for less than its intrinsic value.

Markets adjusted to gold’s relatively low prices by discouraging its production and increasing its demand. Eventually, this created a shortage which sent gold prices soaring from $400 to a peak of $1,900 by 2011. Gold prices moved back toward its intrinsic value by the middle of the decade and have since soared back to the $2,000 vicinity.

At $2,000, gold prices are double our estimate of its intrinsic value. At this level, traditional supply and demand forces should tend to encourage more production of gold while reducing its demand. The result should be downward pressure on gold prices in the years ahead.

In order for gold prices to increase from their current relatively high level some factor unique to gold would have to occur. One such factor, which may have contributed to the rise in gold back to the $2,000 vicinity, could be the increase in gold purchases by central banks. Factors unique to gold always have the potential to shift prices away from more fundamental factors.

While such unique factors are always possible, it is seldom prudent to invest in any asset that is grossly overvalued. It is often more prudent to wait for longer-term supply and demand forces to correct for such disparities.

The bottom line is that gold appears grossly overvalued compared to other commodities. Without some unique force driving the gold price still higher relative to other commodities, gold will experience significant downward price pressure in the years ahead.